Being the new year and all, I thought it would be appropriate to put together a checklist for those that want to improve their financial situation in 2018 and beyond. The reality is that if you don’t take action now, you likely won’t take action later.

Remember that building wealth in order to achieve financial freedom is the direct result of simple disciplined steps made consistently over time.

Notice that these are not “goals,” but rather a list to follow of 12 EASY ACTION STEPS you can take to ensure your financial house is built on a solid foundation. I’m making it super easy; you can take just one action step a month through the end of the year and complete the whole list.

And guess what? Nothing on the list will take you more than an hour to complete. That is 4% of your day or just 0.14% of your month. You can spare that kind of time, right?

For the super ambitious you can probably knock out all 12 steps in about 4 hours OR LESS. Use the “New Year Resolutions” momentum!

Let’s move on to the list.

12 Financial Steps You Must Make in 2018

1. Track Your Net Worth (and while you’re at it, be sure to track your income and expenses, too)

You have to track the things you want to improve. There is a famous saying in business philosophy that I believe is just as relevant in our personal lives and that is:

“What gets measured, gets managed.” – Peter Drucker

There is so much POWER and TRUTH to this quote. Tracking allows you to establish a baseline from which to improve (we all have to start from somewhere). This is super important because you need to know where you are, and where you’ve been, to figure out the path to where you want to go.

“The simple act of paying attention to something will cause you to make connections you never did before, and you’ll improve in those areas – almost without any extra effort.” – Sebastian Marshall

Building wealth is a numbers game and you have to keep score. Do you want to be a millionaire? Of course you do! I personally want to be a millionaire several times over. And guess what I’m doing that you should be doing?

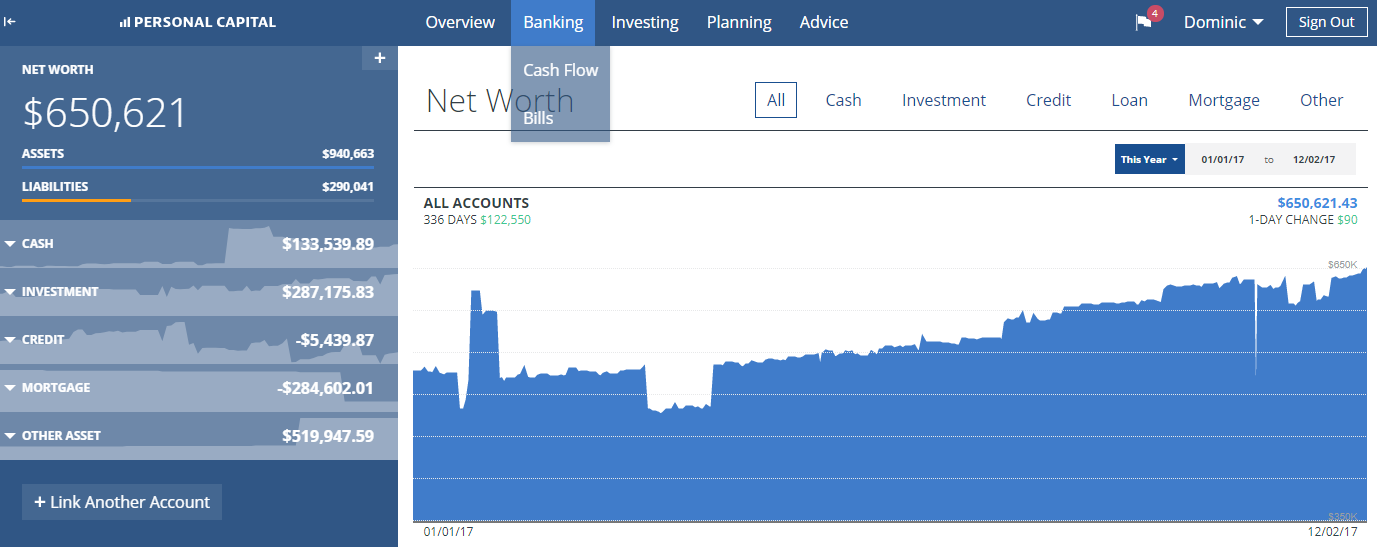

TRACKING! (you can see my history here)

Yes, you need to track all of your financial accounts. You need to track your income. You need to track your spending. You need to track your assets. You need to track your liabilities. You need to track your investments. Track, track, track.

It may sound laborious, I know. But it’s the only way.

I have good news for you. Tracking has become a lot easier with advancements in technology. And the best tool that I’ve found to automate my tracking is Personal Capital (it’s FREE). Below is a screenshot from my personal account, where I have aggregated over 20+ financial accounts.

Personal Capital allows you to aggregate your entire financial life into one easy to manage financial dashboard. All you need to do to see all your accounts in one place is log into Personal Capital and voila! But it doesn’t stop there. PC will even automatically classify all your income and expenses for you. You get a FREE and fully AUTOMATED tracking system.

2. Increase Your 401K Contribution & Work Towards Maxing Them Out

Are you leaving money on the table? At the very least you should be contributing enough to get the full match that your employer offers. If your employer provides a match of up to 6% of your income, you should be contributing at least 6%. So, if you are reading this and your contributions are set at 3% of your pay, leave right now and go increase that to 6% (seriously, do it NOW). Even if your company only matches 50% of every dollar you contribute, that is a 50% guaranteed return, something you will not find in any investment that exists on earth (or the universe).

Some of you reading this might be thinking, come on GYFG, I am already doing this. Give me something more challenging than this.

To that, I say, good on you, but there is still much work to be done. If you’re already taking advantage of the full match that your employer offers, then you need to level up and work towards maxing out that 401K. The contribution limit is $18,500/year (in 2018). I encourage every reader of this blog to aim towards maxing our their 401K as soon as humanly possible. The earlier you do this, the easier it becomes.

I often recommend to recent college graduates that they do this as soon as starting their first job. If you are a recent grad, the reality is that you’re likely earning way more money than you were while going to school. Maintain that student lifestyle a bit longer, develop this habit early, and get some real traction in place. It is something that your net worth will thank you for later.

Look, the average starting salary based on 2015 statistics, is $50,651, so maxing out your 401K would mean contributing 36% of your income, leaving you with $32,651 before taxes. You’re probably only going to pay about 15% in taxes (if you live in CA; less in other states across the USA). That still leaves you with $27,753 in living expenses or about $2,300/month.

You can do it!

3. Open a Brokerage Account (IRA or After-Tax Account)

Depending on where you are in life, you may be maxing out your 401K already, and you may have some additional funds that you’re ready to invest elsewhere. Look, I’m not even telling you to fund the account right away. In this step, you’re just opening up a brokerage account (baby steps).

I recommend TD Ameritrade, which is the brokerage I personally use (and have been using for 10+ years). Let me tell you why I love them so much:

- They have what I believe to be the BEST retail investing platform (in the world). It’s so easy to use.

- They have over 100 ETFs that you can invest in for $0 Commission (yep, that is FREE 99).

- Oh, and 32 of those ETFs that are commission free are part of the Vanguard family (yep, those funds with the lowest fees that all the PF bloggers rave about online).

- There is a ton of FREE education provided.

So, go open up an account now. (I recommend downloading the desktop Think or Swim platform)

Bonus Points: Set-up a monthly auto deposit. I currently have $1,000/month sent to my after-tax TD Ameritrade account.

4. Apply For A Cash Rewards Credit Card

Are you leaving FREE money on the table? Why not get paid for the spending that you’re already going to do anyway? In late 2016, I signed up for the Chase Sapphire Reserve, which earned me almost $7,000 in cash back in 2017. If you include the other credit cards I churned, this earned me close to $10,000 in 2017 (not too shabby if you ask me).

This is a substantial increase from the $6,000 earned in 2016 from new credit card bonuses and cashing in points for cash. Why not get paid for the money you were going to spend regardless? And they say there is no such thing as a free lunch.

WARNING: Only do this if you can afford to NEVER carry a balance. If you can’t pay off the balance every month, a credit card is not for you, regardless of the reward.

Think you don’t have any room in your budget to invest? Earning credit card cash-back rewards on expenditures you were going to make anyway could offer up a significant amount of possible investing dollars. Think again!

Do I have your attention now?

5. Automate Everything

We covered this one a little bit in number #2 above since your 401K contributions typically come out of your pay automatically every pay period. But there are plenty of other things you can automate in your financial life.

- Automate your credit cards, by setting them to auto-pay (i.e. set your payment to “pay the statement in full” every month).

- Automate your monthly mortgage payment.

- Automate all of your recurring monthly payments, using the bill pay feature offered by your bank.

- Automate transfers to investment accounts (like the one you opened up in #3 above…hint, hint 😉 ).

- Automate, Automate, Automate!!! Make one decision now instead of multiple decisions every month.

6. Ask For A Raise

There have been studies done that show that people that ask for more money make more money!

You might be thinking, “but I just got a 3% raise, how can I go and ask for more money?” If you’re reading this blog, you’re likely an overachiever, which in my opinion means you have likely provided more than enough value over the course of the last year to demand a raise that is substantially higher than 3%, which is virtually only a cost of living adjustment (2.2% for 2018, according to Social Security Trustees).

And if you truly feel uncomfortable about this, ask yourself if you are in fact adding value to the company you work for above and beyond what is expected, and what others are doing. If you cannot answer “yes” confidently, find a way to do so.

Be prepared to walk your employer through why you have earned the raise you are asking for and show up armed with specific examples of the value you have added to the organization. For example, a few years back I found $500,000 that the company I was working for at the time was double charged for over a three year period. It wasn’t on anyone’s radar, the business had no clue, and getting the money was a huge windfall that was greatly appreciated.

This made it easy to ask and justify a 10% raise after only five months with the company, which at that time in my career was only $10,000. It’s a pretty easy sell when you say I just made you enough money to pay for this new raise for the next 50 years.

Don’t settle for 3% raises!

7. Buy & Read “The Slight Edge”

This book, more than any other, has made a HUGE impact in my life. I have probably given away at least 25 physical copies of this book, and have recommended it over 100 times in person (thousands if you count this blog).

Do yourself a favor and buy a copy for yourself here

If we get at least 50 comments on this post, I will choose one person at random to send a FREE copy. This is my way of encouraging you not just to read and scroll, but to participate in the conversation.

8. Buy Discounted Gift Cards

Do you like paying less than face value for the money you were already going to spend? Of course you do!

If you’re already going to spend money at a particular place (restaurant, retail store, grocery store, etc.), why not get a discount? About two years ago, we found Raise, an online marketplace for purchasing discounted gift cards. As you may know from reading our monthly financial reports, we spend a lot of money on eating out, so we regularly buy discounted gift cards to the restaurants we either frequent regularly or ones we know we will soon.

We tend to find gift cards marked down by 10-20% to the places where we were already going to spend money anyway. In 2017 we picked up $7,000 worth of Lowe’s gift cards for about $6,300 for a home improvement project (we laid wood tile throughout the entire first floor of our home). That’s a savings of $700, or 10%.

It’s likely you have places you frequent often, so why not get a discount on all your future purchases there by purchasing discounted gift cards? There are thousands of vendors to choose from. Check out Raise to save some money.

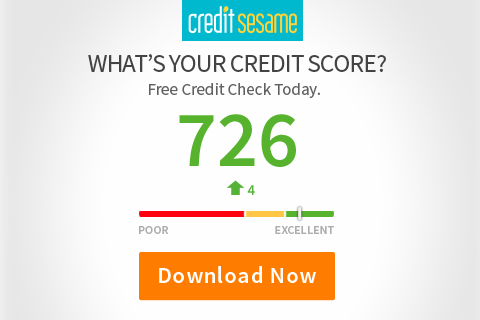

9. Check & Monitor Your Credit Score

Your credit score plays an important role when it comes to obtaining the financing you need throughout your financial life. Almost all of us will need a mortgage at some point and  time. You also need a solid credit score to get approved for credit cards (the only way to get those lucrative signup bonuses and cash back programs mentioned in #4 above).

time. You also need a solid credit score to get approved for credit cards (the only way to get those lucrative signup bonuses and cash back programs mentioned in #4 above).

These days you can check and monitor your credit score for free.

I recommend you check out Credit Sesame, which comes with the following FREE benefits:

- Free Credit Score and Monitoring

- Free Identity Theft Protection – you’re protected with up to $50,000 for FREE.

- Stay Informed with Real-time Monitoring & Alerts (Remember #5 above? Automate, Automate, Automate)

- Get Powerful Insights Into Your Finances

- Manage Your Credit and Loans in One Place

- See How Your Finances Measure Up Over Time

- Opportunities To Save Money

It only takes 90 seconds to sign up for a FREE account. How can you pass up the free $50,000 identity theft protection alone for that minimal time outlay???

10-12. You Choose

10-12. You Choose

Maybe you have already been noodling some ideas of your own. If you need a little more inspiration, here are a few more ideas that I have:

(1) Look into refinancing your mortgage to take advantage of a lower rate.

(2) Pay off those pesky student loans. Automate a higher payment with a pay off date goal set.

(3) Pay off your credit cards (in full and then never carrying a balance ever again).

(4) Put together a plan to eliminate all the debt in your life.

(5) Create an Emergency Fund and working towards saving six months worth of living expenses.

(6) Set up a Trust that includes a will.

(7) If you’re ready to have your money work for you, you can also consider setting up an account with PeerStreet (I’m earning about $500/month in interest income every month).

(8) Or consider diversifying your risk by investing in a non-correlated asset like life settlements.

(9) Choose a meaningful place to donate, and automate that. We sponsor a little boy in Africa for $100/month, which to us is a very small amount, but it pays for his schooling and room and board.

The possibilities are endless and likely unique to your own financial goals and current financial situation. Check off the above #1-9 basics first though. Boring and automatic is not bad, but rather creates a solid foundation from which to try some more creative and aggressive ideas later.

I wish you a very prosperous and fulfilling 2018!

– Gen Y Finance Guy

38 Responses

Hey Dom – I picked up Slight Edge last week per your suggestion! I’m going to read it soon and apply the things in the book in my daily life.

Would you suggest this path: max 401k then open brokerage account? Currently, I get the 4% company match. Right now, I’m sitting on a decent sized cash position and wondering what next. Would you suggest IRA or brokerage?

Erik – The Slight Edge is going to be a game changer. I am actually in the middle of reading it for the 7th time myself.

I would personally prioritize maxing out all the pre-tax accounts before opening up an after-tax brokerage account (so max out 401K, then IRA, then after-tax brokerage).

Great list Dom. I think this list applies whether you’re just getting started or have been at the game for awhile. Just yesterday we made the changes online to max out my fiancé’s 401(k) and 457(b). Now that we’re getting married this year, we’ve got to take advantage of all the tax-protected space we can. It will force us to change how we handle finances but obviously the short term pain is worth it. Like you recommended in #2 above, sometimes you just need to flip the switch to max out the accounts. Pretty soon you’ll adjust and won’t even remember what it was before you were contributing the maximum amount.

Josh – I am jealous you get another set of pre-tax accounts to contribute too 🙁

Nice Move!!!

Solid list! 7/10 done already, I’m glad our 2017 goals aligned so well! Side hustle as my “move of choice” is up next.

I have friends who use the gift card discount idea. They use their money back credit card at a local grocery chain with a membership card. End up getting a discount on the card, points back, and free gas! I haven’t had a big purchase at one store in a while, but the tactic is on my radar.

Right on Chris!

I’m surprised how many people haven’t even considered #1. They have NO IDEA what their net worth is. I can’t imagine. To me that seems scary.

I hear you Brad.

It’s hard to know what to do to improve if you don’t even know what the starting point is.

Ah, I haven’t heard of “The Slight Edge;” I’ll have to check it out at my library. 🙂 These are all fantastic ideas to get your finances in order!

I honestly didn’t start tracking my net worth until this month. Since we’re in quite a lot of debt, I never thought it made sense to track our net worth since it’s always zero lol. But I did download Personal Capital to see what all the fuss was about, and I’m actually really enjoying tracking my net worth! Yes, it’s in the red, but it’s even more motivation to pay down our student debts to get in the black.

Mrs. Picky Pincher – You have to go check out “The Slight Edge” and read it as soon as possible…it will change your life.

Glad you are tracking your net worth, soon enough you will be in the black 🙂

There are definitely a couple on this list I need to do. I like to think I’m pretty on top of this stuff, but continuous little improvements can go a long way.

Thanks for sharing them all in one place!

It’s the simple disciplines made consistently over time that eventually lead to exponential results.

Great set of rules.

Tracking net worth helps me to see the results of my actions. It also helps to know the number when you have to take a decision.

Two items I need to work on: further automation and asking a raise. I plan to achieve both in 2017!

Go after it Ambertree!

Great post! I just published on a post on actual investments for 2017. I think this posts complements well. Great rules. Keep up!

Awesome!

Great post. I have found very low priced gift cards on ebay as well.

Amy – what kind of discounts are you finding on Ebay?

Dang 🙂 I should have waited for a shot at winning “The Slight Edge” 🙂 I ordered it a week ago upon your recommendation.

Great list. I swear by n°5 and n°6

Just think…you will have the advantage of time on your side by getting earlier than anyone that might win it.

I get more than the match on my 401k, then I Roth and my plan is later in the year savings account excess will go to brokerage. I want to make sure savings is good before I up my 401k again.

My credit cards are paid off monthly.

I’m skeptical of automating too much. I had a cable bill autopay, put it on hold, and then it kicked in again despite having a new account. I’m ok with the bill paying, but paying the credit card gives me a chance to review the charges.

My company did layoffs in the fall, and they are doing retention bonuses, so I’m going to see if the raises shake out.

I’m treating yoga teaching as my way to a raise. So I think my #10 is setting up my llc. Then comes the sep Ira vs solo 401k decision to put at least some of it away.

If I don’t win the book, I will get it out of the library. 🙂

Thanks for the inspiration!

” I encourage every reader of this blog to aim towards maxing our their 401K as soon as humanly possible. The earlier you do this, the easier it becomes. ” This is so true. I maxed out over a decade ago and you learn to live without the money. When I look at my 401K balance, I know it is well worth it. I buy Lowe’s and restaurant gift cards from Raise as well. Love the extra savings.

Loving the infographic there Dom! I like a good list post when used sparingly and as you mention you don’t have too many or hardly any of them..

The #1 thing I’d focus on is your #1 point about tracking aspects of your financial life.. That is vital to success combined with the slight edge principle :)!

Thanks Buddy!

#1 is in first position for a reason 🙂

Cheers

I have never heard of The Slight Edge but based on your recommendation I’m going to pick it up. Especially if you’re in the middle of reading it for a 7th time. Thanks for sharing!!!

Mustard Seed Money – You will not regret picking up a copy of The Slight Edge. I would love to hear what you thought after reading it.

Hey Great list Dom! I’ve only scored a low 6/10 but that’s still nice. Unfortunately still not maxing my 401(k) but 2017 should be the first year! I’ve never read the Slight Edge, but you keep talking about it so I might give it a try 🙂

It is a game changing book Finance For Geek!

Thanks for the automate tip, never though of using it to fund my brokerage account.

I will check Raise out, never heard about it before. Thx

Thanks for the discounted gift card idea. We have a couple of small projects lined up for this summer. And savings on the materials will definitely help 🙂

I hope you save a boatload of money!!!

Great points. I’ll need to pick up a copy of The Slight Edge. Always looking for a good read. Thanks for the recommendation.

You’re going to love The Slight Edge!

Cool! Never heard of The Slight Edge. But since you recommended it, I’m going to check it out!

Thanks for the tips. I have done each of them but number 7. I’m lucky to be able to max out all of my retirement accounts. Financial Freedom can be within our reach with some tips like this and living responsibly.