It’s time to shake things up with this month’s financial update. There hasn’t been much change to the format or content for 33 straight months, and I feel like the time has finally come to inject fresh life into this report and content.

Mission Statement: To Humanize Finance, Build Wealth, and Reach Financial Freedom.

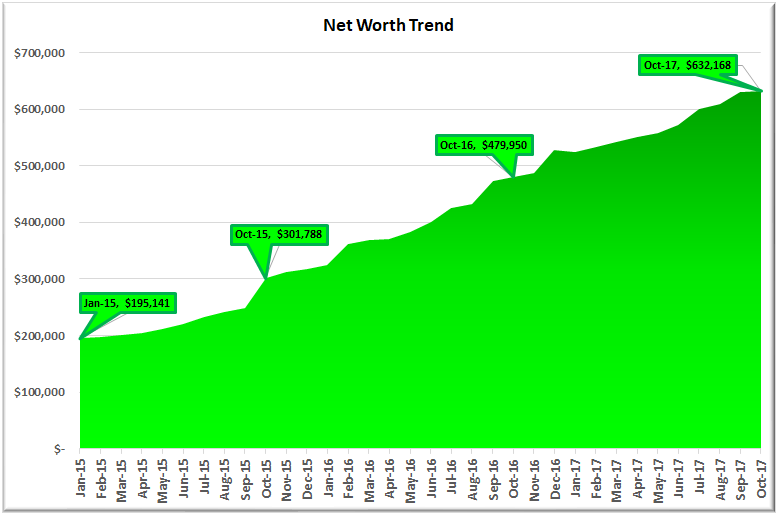

For those of you that are new around this corner of the internet, these monthly reports are about full transparency. They are just as much for me as they are for you. It’s a hard decision to make all of your financial details public, but it’s also a very motivating one. The process I go through every month to produce these reports has been enlightening and life-changing. I published my first “income and net worth report” for January of 2015 when our net worth was only $195,141 and our gross income was on pace to hit $178,000 that year.

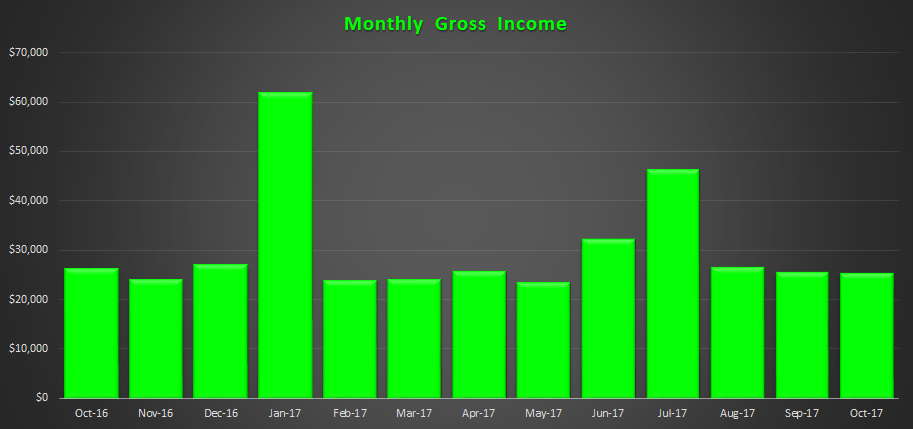

Fast forward three years, our net worth is on pace to finish the year at ~$655,000 with a gross income of $370,000.

- That’s a 3.4X increase in net worth due to a compound annual growth rate of 50% for the past three years.

- At the same time income has increased 2.1X, which translates to a compound annual growth rate of 28%.

I honestly don’t think the GYFG household would have experienced these kinds of results without the existence of this blog and the accountability it brings. Knowing that I will need to share our results with my readers every month keeps me very focused and intentional with all things related to our financial well being. For that, I THANK YOU for taking the time to read and interact with me on this blog.

That said, my sincere hope is that my policy of full transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom if they are willing to do things differently than the pack. If you’re after average results, then you’ve landed on the wrong site. There’s nothing wrong with average, but the kind of results I preach are EXTRAORDINARY. Yes, the “get rich slow” method is proven, but the alternative is to “get rich fast.” Look, I have no interest in living like a starving college student until I am old and brittle, only then to have the means to do the things my body is no longer physically capable to do. And I don’t want that for you either!

Here at GYFG, we approach the pursuit of FINANCIAL FREEDOM with an abundance mindset, so you won’t hear me telling you to cut out those $5 lattes.

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years of slaving away for The Man before you have the option to retire. I personally think that 10-20 years is all you need, and the folks that are more aggressive can probably reach financial freedom in 10 years or less. A high income paired with a high savings rate is a good recipe for the 10-year track.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (because not that many people giving financial advice do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities (and BS). Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

As always, you can find all my previous reports on the Financial Stats page.

Net Worth

Well, October ended up being all sizzle and not much steak after last months increase of almost $21,000 to net worth. For the month, net worth was up just shy of $2,000 or 0.3%. Significantly less then I had anticipated, but like everything, there is a story.

October Net Worth $632,168 (up +19.8% for 2017 YTD)

- Previous month: $630,223

- Difference: +$1,945

As I alluded to above, I had anticipated a gain of $10,000 in October, but for the reasons below this didn’t come to fruition:

(1) We ended up gifting $3,000 to my in-laws after we closed the sale of our investment condo. They originally helped us get the condo and although they were not expecting anything from us as a result of the sale, it was nice to be able to surprise them with dinner out and a fat envelope of cash. It was ironic that we decided to start our night in a 1930s style speakeasy, especially in light of slipping a fat envelope across the bar to our in-laws 🙂

(2) One of our stock positions (AT&T) fell significantly in October, leaving us with a paper loss of $3,000.

(3) We had an additional $2,000 worth of bills for repair work done on the condo that I was not aware of (mostly because my wife was handling all of this while I made three trips to NY within a five week period). The sale is now complete, so all expenses related to the condo are now behind us.

Net Worth Break Down:

– This month I decided to do away with the P2P category that now has a balance of around $3,300 and combined it into the cash category. I have been withdrawing ~$300/month as it becomes available. These accounts should be completely wound down in another 10 months.

– Last month Cash only made up 11% of the total pie, but this month has jumped to 27% due to the sale of the investment condo closing. In the end, we netted about $93,000 from the transaction.

– Due to the above, the Real Estate category dropped from 51% to 36%. Keep in mind that this category includes the equity in our primary residence, our investment in the Rich Uncles commercial REIT ($10,000), and our hard money loans through the PeerStreet ($80,000) platform.

– As a reminder for newer readers, the Business category represents the ownership I have in the private company that I work for. Earlier this year I wrote my largest check ever ($105,000) to take advantage of what I think will end up being a great financial opportunity.

– The Stocks category really represents the cumulative value of our retirement accounts that are invested in stocks. However, it is not all of our retirement money as the majority of our PeerStreet investments are made through a self-directed IRA (worth about $73,000).

– We have not added to our Gold position in some time. I’m really starting to question whether gold really has a place in our overall portfolio mix or not. I probably won’t liquidate what we have, but it is unlikely that we will be adding to this position in the near future.

– That leaves the Cars category. I include cars because the endgame is to keep cars as a percentage of the overall net worth pie as small as possible. By including them, it keeps me conscious of the opportunity cost of sinking too much capital into the machines that are only meant to get us from point A to point B. The combined value for our cars is currently being held at $17,000 and will get re-valued at the end of the year. I suspect the value will drop by at least $3,000.

Gross Income

As you can see from the chart below, our income has been rather flat the past three months. This is a trend that I expect to continue through November, but then in December, we will see a nice spike due to a three-period pay cycle for me. The only x-factor that could break the trend earlier would be the commission piece of Mrs. GYFG’s compensation.

It’s almost hard to believe the monthly incomes we realized in January and July of this year. The reason those two months are so lumpy has to do with the way my bonus is paid out. In January I was paid the remaining 70% of my total bonus potential from 2016 and then in July, I was paid 30% of my 2017 bonus potential (with the remaining amount payable in Jan/Feb of 2018).

Going into 2017 I had very ambitious income goals, which I have come to accept we will not achieve with only 2 months left in the year. In my ambition-fueled delusional state, I actually thought we had a chance at hitting $440,000 in 2017, but now realize that number will be closer to $370,000. You know what they say, shoot for the moon, and if you miss you will still be among the stars.

One of the other metrics that I like to track is our trailing twelve months (TTM) gross income. We won’t have a chance at setting a new record until January or February of 2018, but it is going to be close. At most I think we could beat it by $10,000 but that is not a guarantee.

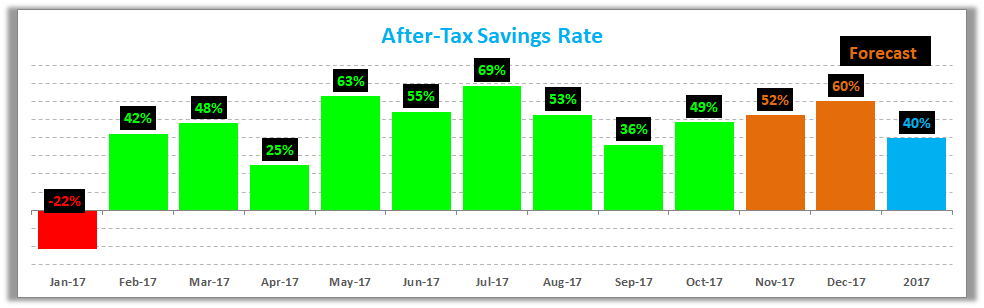

Savings Rate

Below is how we did vs. our goal of saving 50% of our after tax income.

We are currently on track to miss our goal of saving 50% due primarily to the decision I made to carry the $33,000 we paid to put my brother through rehab as an expense. However, if you back that out, our “adjusted” savings rate is actually on track to hit 52%. Unfortunately, the “it doesn’t count bucket” doesn’t exist. As I mentioned above, this is technically a loan, but since we are not sure if/when we will be paid back, we are not carrying it in our net worth figure as an asset. That said, I have come to the decision that it probably doesn’t belong in our expenses either.

Speaking of savings rate, have you checked out my post where I mathematically prove the importance of your savings rate as a higher priority than the compound return? If you’re trying to build wealth quickly, then you have to read this post.

Mortgage Early Payoff Goal

You can read about our strategy to pay off our mortgage in 7 years (and 3 months). After several refinances we currently have a 3/1 ARM at 2.25% and we currently owe $294,864. Our primary residence is currently sitting at 22.2% of our net worth, still higher than we would like, which is why we have not made any additional mortgage payments this year. We would like to see this closer to 20% in the short term and far less in the longer term (like less than 10% over the next 10 years). That said, due to the sale of the condo, we have decided to divert about $24,000 to pay down additional principal in order to stay on track for our 7-year goal (in November or December).

Our primary residence is currently sitting at 22.2% of our net worth, still higher than we would like, which is why we have not made any additional mortgage payments this year. We would like to see this closer to 20% in the short term and far less in the longer term (like less than 10% over the next 10 years). That said, due to the sale of the condo, we have decided to divert about $24,000 to pay down additional principal in order to stay on track for our 7-year goal (in November or December).

This will move our goal progress to 24.1%!

Closing Thoughts

For those of you have been reading these reports for a while, you will notice that I have excluded detailing our expenses. This is not because we are no longer tracking expenses, but I don’t think I need to share them every month. I am thinking I will have a quarterly version of this report that will detail out expenses YoY and against our budget as a special quarterly section.

We have a few more moves to make before the year ends, and those include:

(1) Investing $30,000 in Three Life Settlement policies. This is what I wrote about last week and the check was actually just cashed yesterday, so keep on the lookout for more details in the near future.

(2) A part of our BIG MONEY moves for 2017 was to pay down $28,800 in principal on our mortgage in order to stay on track with Year 3 of our 7-year goal of having the mortgage completely paid off. $6,700 will have been paid down through regular amortization from our monthly payments, which leaves about $22,100 remaining for us to pay down before the end of the year.

(3) Then there are the automated investments that will keep doing their thing through the end of the year. The 401K will be maxed out. The HSA account will be maxed out. We continue to invest an additional $500/month to Rich Uncles. We also started sending $1,000/month to an after-tax brokerage account, but we have yet to put the money to work yet.

That about sums it up!

I am looking forward to chatting with you all in the comments below. How was your month? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

Cheers!

– Gen Y Finance Guy

18 Responses

Nice Update.

it is cool to see you put you reflections down in writing because it will allow you to come back to them years from now to analyze the decisions and see which ones you like the best. [maybe another blog post somewhere down the line 😉 ]

Curious, It appears you have a healthy appetite for risk with big bets on individual companies like your employer and other stock positions.

-Do you have a plan if those positions do not pan out at planned? whats is the plan to unlock the money if needed?

-Also it would be good to compare your rate of return on your individual positions vs indexing (which we seem to get beat over the head with) Might prove enlightening at a later date to see how you have done vs the market.

Onward and upward.

Thanks, Jason!

You have no idea how much I have learned about myself through this blog. I only wished I started writing sooner. Recently I have started venturing back to posts I wrote over 3 years ago and after I get past how horrible my writing was in the beginning it is interesting to see how I have evolved in many things, but also held firm in others.

Re: Your Questions

First, I like to preface this with a Quote from Warren Buffet on concentration:

“Keep all your eggs in one basket, but watch that basket closely.”

(1) There is no plan as to what to do if some of the big bets I have made don’t pan out. They are illiquid investments, so there’s not much you can plan. I have made some big bets, but as JayCeezy pointed out, we are in the sweet spot for taking this kind of risk. I guess you can say that the contingency is addressed before making the investment. We don’t invest anything we can’t afford to have locked up in an illiquid investment. You also should realize that the $105K that I invested in my company was as much for what I see as an opportunity of a lifetime as it was for political reasons to advance my career and compensation.

I saw this as an opportunity to show my commitment to the success of the organization. This investment allowed me to solidify a position in the C-Suite which came with $75,000 increase in total comp after just realizing a $60,000 increase in comp just 15-months earlier. The way I look at it is that I am going to earn an additional $375,000 over the anticipated 5 year holding period that I would have otherwise not realized. Also, think about the implications holding a C-Suite title over another 20 years of my career. So, even if I lose the entire $105,000 I still very much win.

You will notice that I tend to be very calculated and opportunistic in everything I do.

(2) I agree that it would be interesting to see how all these investments perform against simple indexing. I actually had a series I was doing quarterly doing just that but decided annually or even less often made more sense. The reality is that these are long-term investments with at least 5-year horizons. So, I may wait until exit to benchmark their performance.

Cheers,

Dom

Always enjoy when you put pencil-to-paper, GYFG. Your writing makes it easy to follow along with your intention, strategy, tactics, and process. Am loving your attention to Savings, as that is where the GYFGs have the greatest opportunity for NW impact, at the moment. As you note in your Savings post, ‘spend less than you earn.’

“Annual income twenty pounds, annual expenditure nineteen [pounds] nineteen [shillings] and six [pence], result happiness. Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery.” – Charles Dickens, ‘David Copperfield’

Your non-traditional investments are also quite interesting for me to read about, as you are at a great point on your ‘timeline’ to assume risk. Your savings will counteract any unpleasant results, compared to taking on these risks in 10, 20, 30 years (you will be long-retired by then, I am sure of it!) Looking forward to reading about your company equity and Life Settlements.

Liking your idea to move to a Quarterly metric. Not sure how you are using the Monthly figures to adjust/improve, as your salary/bonus is predictable, while the expenses (leaving $ available to save) are not. You probably see this in your worklife, with the number of work/non-work/holiday with a large variance (i.e. Feb compared to August).

The month-over-month figures are going to flatten out, and it might be interesting (for you, and us!) to see your ‘2017 baseline’ in a line overlay and compare it to your upcoming ‘2018 baseline’. I’ve done it, and it is astounding to see Budget/Actual and underlying Assumptions get measured from 5, 10 and 15 years back. Needless to say, I had a pretty optimistic view of my potential! But as you say, it is best to shoot for the moon!

Continued success to you, always interesting to read your work!

JayCeezy – Nice quote as always!

As you said, savings (paired with a high income) is the most powerful force behind our growth in net worth. It will be sometime before our investments are able to spit off returns that exceed what we are able to save.

Regarding my non-traditional investments, I have always marched to the beat of a different drum, but those are really a function of most assets looking bubbly to me. We continue to sit on way more cash than I would like, but if the investment doesn’t make it through the filter, we continue to sit on our hands and enjoy the optionality that cash brings. I agree that we are in the sweet spot of our journey to be taking these kinds of risks.

The quarterly reference was really about detailing out expenses and producing a special version of this report. I will still produce a monthly version in some form or fashion because it keeps me in the zone. However, I do recall a comment from long ago, where you and I discussed what I would do when the percentage increases in NW were no longer all that exciting. I still don’t know the answer to that question. For now, I am satisfied with the two P’s I get from putting this report together every month:

(1) The Process

(2) The Progress

I have noted your suggested idea of comparing baselines and will try to incorporate that in an upcoming post on my plans for 2018.

All the best!

Dom

This is my favourite personal finance blog due to the writing style and willingness to dig into the detail. The size of the numbers is also a drawcard as well, due to the potential for your progress to be extremely rapid. I am keen to see the first million to come up on the scorecard.

Troy – You are the first person to call GYFG your favorite personal finance blog. I’m stoked to be held so high on the list and appreciate you taking the time to read. If all goes well I might just hit the first $1M in the next 18-months…stay tuned.

I really enjoy the human-side you bring out from your numbers. Between never forgetting those who helped you (repaying your in-laws) and helping others (your brother), shows that everyone has their stuff to deal with in life, but you continue to push forward. Very admirable, indeed.

Two questions on the numbers:

1. $105k check to the private company you work for, is this equity? What kind of business is this?

2. $30k in Three Settlement Policies, what are those? I tried to click on the link, but it’s broken.

As always, well done. I enjoy following your journey.

Hey Church – Thanks for the kind words. I really try to keep the human element connected to the numbers.

Re: Your Questions

(1) The $105K check I wrote was for equity. I actually got $300,000 worth of stock but was only required to put up 35%, and the other 65% was extended to me in the form of a loan at 1% interest. I did this during a leveraged re-cap whereby a PE firm we partnered with from 2006-2016 exited and we partnered with a new PE form during the next leg of our growth. The company I work for is a consultancy in the construction management space.

(2) Life Settlement Policies are investments in Universal Life policies that policyholders have decided to sell to investors because they can get 3-4X more than what the insurance company is willing to give them in the form of the cash surrender value. I fixed the link (thanks for pointing that out).

Cheers,

Dom

Thanks for the transparency regarding your equity stake. I hope the investment in your company helps you accelerate your goals. All the best in that.

And thank you for clarifying the Settlement Policy question as well as fixing the link. I have always heard of this market, but never took the time to dive into. Looking forward to your post on them.

Great update – congrats!

At 2.25% interest, do you really want to pay off that mortgage so soon? You still have a few more years left on that ARM, but I’m sure you could easily generate returns above that in the stock market.

Thanks for stopping by Margin of Saving!

We have levered the ARM loans to pay the least amount of interest we can while working towards achieving our goal of paying off the mortgage. I have written several other posts around the thinking, strategy, and commitment to achieving this goal:

If you’re interested you can see those posts here.

There is also one other major play that I have yet to write about, but I plan to write about soon.

Cheers,

Dom

Yo yo, Sean here. Just checking in. Nice job keep it chugging along. I’m still amazed at the combined income..you guys are knocking it out of the park there.

It’s been a great year for my business and I’ve grown production nearly 100% year over year…I guess losing my salary really kicked me into high gear! Things have been cruising along for us as well. Net worth is currently right around 685k. We’ve been spending a ridiculous amount of money lately or else would already be above 700. If the markets are REALLY strong, we both just may hit the million mark next year 😀

Cheers!

Sean

Hey Sean – Stoked to hear that you have been able to kill it in your business. Up 100% is AMAZING!

You continue to stay a few steps ahead of us on the net worth front, but it feels like a close race. I think the best we will do is end the year around $650K with a big pop in Jan/Feb of 2018 (depending on when bonus hits). I’m also in process of asking for a $50,000 increase in base salary.

The march to our first $1M continues…