A few months ago I shared a post about helping my brother get a new car after he totaled his previous one. It really got me thinking about how much it was costing the GYFG household to have two cars. Unfortunately, we bought our cars before we had solidified our financial philosophies.

My wife and I both bought new cars within a 12-month period of each other. I bought my Hyundai Sonata in April of 2011 for $32,000 and we bought my wife’s Hyundai Tuscon in April of 2012 for $32,000. Back then we were only earning around $170,000 combined. Yes, we spent 38% of our annual income on cars! It makes me throw up a little in my mouth when I realize how much we spent on cars, especially in light of how much we gave up in market returns over that period.

This decision cost us $50,000+ in potential market returns had we invested this money in the S&P 500 via the SPY ETF. The returns were: 1.8% (2011), 16% (2012), 32.3% (2013), 13.5% (2014), 1.3% (2015), and 7.7% (2016 YTD).

That said, let’s not get lost in the potential and theoretical world. That was just to point out that cars are nothing but wealth destroyers. Okay, they do make transportation much easier (and convenient), but you get my point. With hindsight I can say without a doubt that we bought way more car than we should have based on our income. Worst of all we did it without really acknowledging the cost of use (which I will break down in detail below).

How Much Does A Car Really Cost?

Or more appropriately framed, how much does it cost to to have two cars???

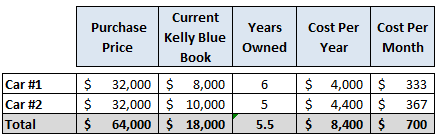

The cost of a car is first determined by the purchase price of the car, the current market resale value, and the total number of years you have owned the car (otherwise known as the depreciation cost). In the chart above you can see that the GYFG household has two cars, and based on the purchase price alone these have cost us $700/month on average. Of course the longer you keep a car the cheaper that car becomes, before considering costs like:

- Insurance (It’s the law to have this)

- Fuel (Kind of essential to make the thing run)

- Tires (Every two years for us)

- Oil changes (We get these every 5,000 miles)

- Car washes (I try to avoid these as much as possible, arguing with Mrs. GYFG that I don’t want to wash the protective layer off)

- Finance charges (If you don’t pay cash for your car)

- Speeding tickets (Among other violations;guilty here)

- Parking

- Other regular maintenance

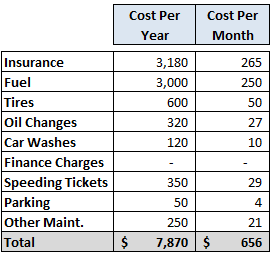

When you really start breaking down the costs associated with car ownership, I think you will be just as surprised as I was to find out how much two cars are really costing us. All the other stuff I listed above is costing us just as much as the cars themselves:

When you add the annual depreciation cost of $8,400 plus the other associated cost of $7,870, we are paying $16,270/year to have and maintain two cars in our household. Our insurance costs are higher than they should be, well because we both tend to be impatient when it comes to driving places, and inevitably one of us ends up getting a speeding ticket every year. So, not only do we have the added cost of the speeding ticket (and traffic school, which I didn’t list), but we also have our insurance rates getting increased on us (you only get a freebie from traffic school every 18 months).

$16,270 PER YEAR ON CARS (ARE YOU KIDDING ME?)

I really had no idea that it was costing us this much money for two cars. Since we own our cars outright, half of this cost is depreciation, and therefore a non-cash item. You could even say it is a sunk cost. Although it is effectively costing us $1,356/month to have two cars ($16,270 divided by 12), the real cash flow is only $656/month, and is the only place we could try to reduce. When you look at the different line items above, the two pieces of low hanging fruit are the insurance line and speeding tickets. The good news is that we do have a speeding ticket (i.e a point) falling off of our record, which will result in a $50/month savings in insurance (which has since kicked in since writing this post).

This post was really about figuring out how much a car really cost, so that in the future you and I could be aware of the true cost of car ownership. This will definitely stick with me when evaluating future car purchases, which we will all likely go through at least several times throughout our driving lives. After seeing the numbers broken down like this, I would now be open to a leasing option in the future (at least comparing the two side by side).

Do you know how much your car is actually costing you?

– Gen Y Finance Guy

28 Responses

Thankfully, in our early-retired situation, we don’t drive a ton. When we do clock miles it is usually for a trip, which we log under “vacation/travel” in our budget.

Even so, we spend about $200/month on the two cars we have. That’s insurance, fuel, and maintenance.

Might consider dropping down to one car at some point, but not just yet. Will drop cable before then (when the agreement runs up this coming October!)

Ayuuuup. There are so many hidden costs of car ownership that I think people don’t even realize. I found out how expensive cars were when I walked to work for a few months. We’d gotten rid of my expensive car and were saving funds to buy a used vehicle with cash. In the meantime, that meant I had to walk to work. I was amazed at how much more money we could save!! I estimated that I saved $20 each time I walked to work by preventing car costs.

Although I went through the exercise of figuring out how much our cars were really costing us, it won’t actually change our behavior much. The only thing it does doe is motivate me to literally drive the cars into the ground until we maximize their full value.

I was thinking the same thing the other week when I paid my insurance bill. I only drive about 4k miles a year… and yet here I go, spending about $2k for registration + insurance.

I heard about some new insurance providers that work better for people with very low mileage. Maybe this is one: https://www.metromile.com/

That might help!

I actually checked them out, but because of my tickets and mileage, it wasn’t going to work to my benefit. But people with clean driving records and low mileage should definitely benefit. They have you install a tracking device so that they can monitor your driving (speed, mileage, etc).

Erik – insurance is something that I need to revisit to get some savings. My cars value no longer justifies paying for full coverage, so I need to call the insurance company and look at reducing my coverage.

It’s nuts, in the last 3 weeks I have spent about $1,700 to replace tires on both our cars, replaced breaks on both cars, and some other misc. things.

Ya I agree they are crazy expensive.

Last year my wife and I both needed to replace our cars (my lease ended, hers broke down and was worth less than repairs). We ended up with a new $19k car and a used $11k car. Could have spent more, could have spent less, but overall I’m ok with it. We got 2 for what most people spent on 1…

The biggest factor is how long you keep the car. If you keep driving those for another 5 years, the depreciation average is much much smaller. So a new car you might want to keep 10 years. If you get a 2-3 year old used car, keep it 7-8.

Brian – I agree the key is to maximize the holding period of the car. We had and continue to have every intention to keep these cars going until at least the 10 year mark if not beyond. I am 6 years in on my car, so hopefully by keeping up with the regular maintenance it won’t be until 2021 before I am due to think about another new car. Then 2022 for my wife.

Cars are indeed a huge drain on one’s assets and that’s why choosing the right one is a tricky task. I once read and interview of a millionaire who said, when you wish to buy a new car, buy the best one you can afford and use it till it’s value falls to zero. That made sense to me because often people sell off their used cars in an effort to get a good price for it and use that money to buy a new car. I haven’t done the maths to figure out which strategy is better but I like the idea of fully utilising a product before replacing it.

Fehmeen – I don’t think I will buy another brand new car again. It’s amazing how much cars fall in value once you drive them off the lot. But I guess only time will tell 🙂

I like the advice you shared from the millionaire.

“washing the protective layer off”

Genius.

But yes, I’ve spent so much on cars over the years it’s not even remotely funny. And I’m only 23. It’s helped me a ton by always buying used (or very used). But it still makes me cringe when I start adding all the numbers up. I’m currently spending $400/month in fuel alone.

Nick – sounds like you are doing a lot of driving.

My girlfriend and I actually purchased a 1998 Toyota Avalon late last year, our Nissan we were financing at the time was totaled in an accident. We were already planning on different ways to cut our cost and save so that we can reach our goal of becoming debt free in less than 3-5 years (starting 2016). We pretty much came to your realization in your post. That cars are a money-pit and financing/leasing a car right now does not align with our current goals. We paid less than $2,000 for the Avalon and insurance runs us about $88 dollars a month. We haven’t had any major maintenance cost besides brakes and the monthly oil change. The car is in great shape just a “little” dated, it really runs well and I feel we have already gotten our monies worth and than some. Great post and “Here’s to a dream life!”

I would disagree with notion that we are wasting money on cars. That is too extreme. Then we should stop eating, taking bath, living in homes with electricity and so on. We need cars and other transportation to be able to live and work. To meet family and friends and visit far off places.

I never said we should stop buying them. The idea of the post was to get people to be more thoughtful on how much a car costs. I agree with you, cars serve a very useful purpose in our lives.

Between my wife and I, we drive almost 30k miles a year. It’s worth it to us so we can live in a cheaper home on a big piece of land outside the city. We purchased a two year old car (25k miles) for my wife for about 60% of the cost of buying it new. She will drive it for five years and then I will take it over and we will get her another new used car. This way, we keep each car for ten years and stagger getting a “new” car every five years.

You really can’t avoid maintenance costs except shopping for cheaper insurance and following posted speed signs. The big mistake people make is buying a car new. Most of your depreciation occurred within the first 3 years then it slows down significantly. The take home message is to always buy pre-owned, pay cash, and drive cautiously.

Hey Jake – I suck at following posted speed limits, which is why I got yet another speeding ticket last week. I think when it comes to both maintenance costs and insurance, your car selection can actually make a huge difference. For example, to replace the tires on one of our cars it costs about $600, but my sister in law has an Audi that needs high performance tires that cost $1,200 every 15,000 miles. We drive about the same mileage every year and I will replace my tires once every two years and she will replace them twice in that period.

Big difference in spending $600 vs. $2,400 (just by the choice of car, regardless of new or pre-owned or leased).

To your last point I will definitely entertain the pre-owned option. But I plan to make it to the 10 year mark with our current vehicles.

Cheers

One of my friends has a McLaren 650s, and the maintenance on that thing is ridiculous. Ontop of that, he has to have a regular SUV because you can’t drive the McLaren in a lot of places (due to the car’s closeness to the pavement).

My car costs $0 Dom! Because I don’t own one. That’s the only financial perk of living in NYC.

Of course I do have to rent them from time to time, so i guess I’m not getting away entirely free.

Josh – I honestly don’t think I could live in the city full time. I do like the convenience of being able to walk everywhere or grab public transportation, but anything longer than a week and I start to feel a bit claustrophobic.

To be honest I look forward to the day of completely autonomous vehicles. This will completely demonetize the entire transportation industry. The day I can pay a monthly fee to UBER to have a car take me anywhere I want to go. The cost will be reasonable when you take out the human error element. Insurance costs should go way down. You no longer have to pay for a human driver.

I personally don’t love driving.

I appreciate all the calculation and the analysis.

I have ran some numbers on this and I think I came up with a formula to maximize the per mile cost, cost of ownership plus cost of acquisition.

I think it went something like this: you buy a 3 year old car, keep for 5 years and repeat.

It seems like you drive a lot, that’s a lot for gas for just one car on your spreadsheet. We have 2 cars as well, but are fortunate that our jobs are close by. It also helps that one car takes regular gas. The diff between regular and premium is insane! 🙂

SMM – The figures are actually for two cars 🙂

I try to avoid driving as much as possible.