GYFG here checking in for the December monthly financial report. If you have been reading these reports for a while you will notice that I introduce each month with the same intro month after month. I do this for two reasons, a) for the newbies to the site (which make up about 50% of the sites traffic) and b) to remind everyone what these reports are all about. By all means if you have read the intro at least once, then please feel free to skip down to the “Summary of December 2015” section where the new content begins (click the orange link to be taken there automatically).

For those of you that are new around this corner of the internet, I wanted to fill you in as to what these reports are all about. These monthly reports are about full transparency. They are just as much for me as they are for you. It’s a hard decision to make all of your financial details public, but it’s also a very motivating one. It’s not just the post, but the process of putting this post together that really benefits me.

My sincere hope is that my transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom, if they are willing to do things differently. If you earn an average salary and have an average savings rate, then you can expect an average result! That means you will likely have to work at a job you may or may not enjoy until you’re 65 and then maybe you can retire IF you’re lucky.

Hey, there is nothing wrong with average. If you’re happy with average, then by all means keep doing what everyone else is doing. Not sure how you feel about that, but I have no interest in living an average life. I want EXTRAORDINARY.

Most people don’t want to live below their means in order to reach FINANCIAL FREEDOM, because that’s painful. They think it involves cutting out all the joy in life. You know what I’m talking about, those financial gurus that tell you that in order to get rich you need to cut out the $5 lattes and stop going out to eat. Then after 40 years of diligent and above average savings and super low spending, you will be a millionaire. Basically, you have to live like a college student and suppress all the things you want to do in life and then when you’re old you will be rich.

Okay, that doesn’t sound like the plan for me either.

The good news is there is another way. This site and these reports are here to show you the OTHER path to financial freedom. There is a way where you can have your cake and eat it too. I believe and hope that over time I will be able to convince you of the following:

In order to reach financial freedom you can choose to live below your means by cutting expenses to the bone and living in a state of scarcity or you can expand your means and live in a state of abundance by increasing your income and enjoying the $5 latte or other indulgence of your choice.

Not only that, but if you’re diligent you can reach financial freedom a lot sooner than anyone has ever led you to believe.

Our Mission Statement:

To Humanize Finance, Build Wealth, and Reach Financial Freedom.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (because not that many finance blogs or people giving financial advice do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities (and BS). Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

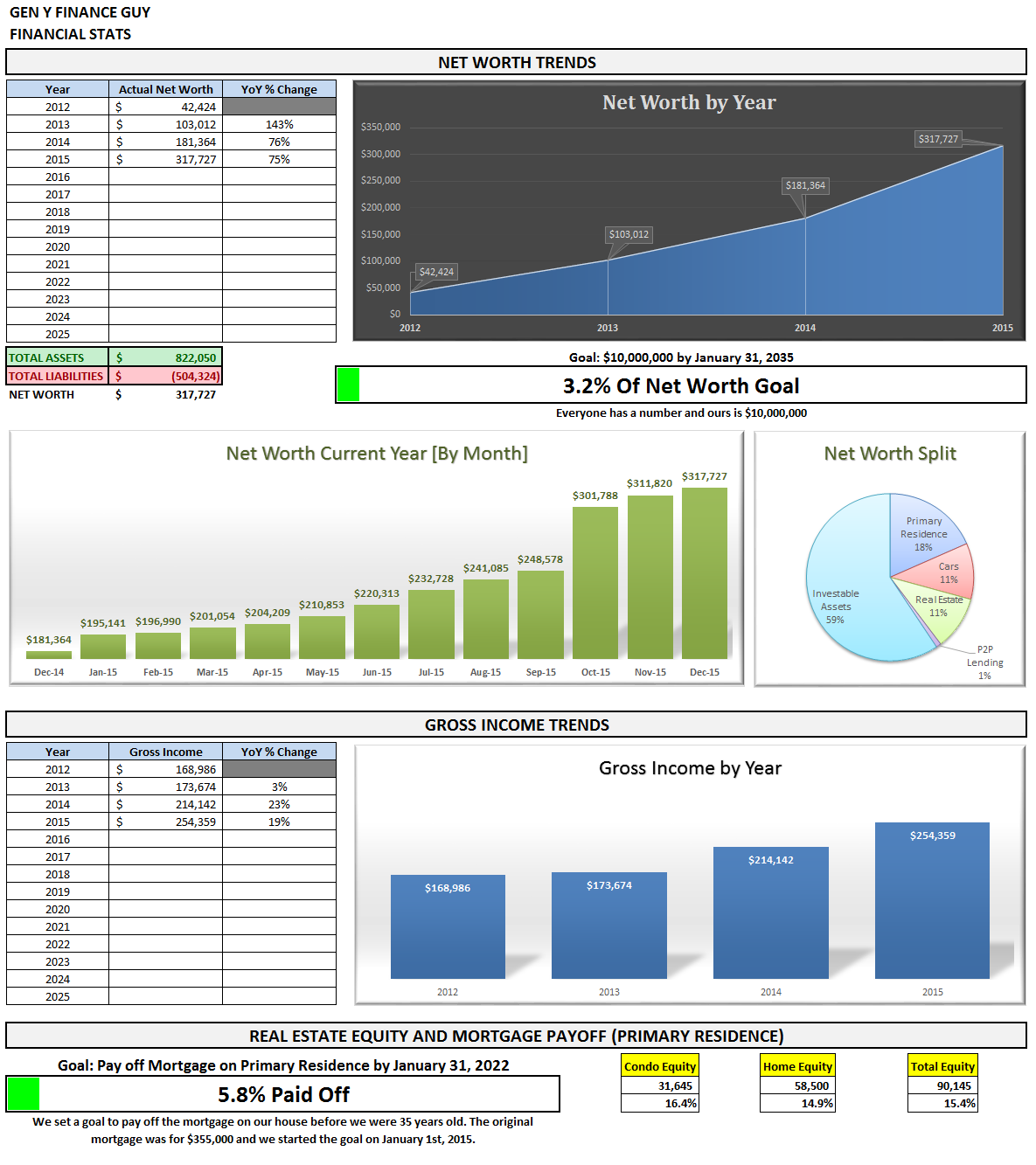

As always, you can find all my previous reports on the Financial Stats page (as well as annual trends and a few other financial metrics not found on this report). In these monthly reports the plan is to give you a month over month update on Gross Income, Assets, Liabilities, Net Worth, Expenses, Contributions, Savings Rate (NEW), and progress on the mortgage pay down goal.

Summary of December 2015

The holidays were in full swing in December with Christmas parties galore. Luckily the work schedule calmed down considerably to allow for a little holiday cheer while visiting with friends, family, and co-workers. We spent way more money than I expected, but we will get into that shortly in the expense section below.

As I write this, it is our last day at a beach house we rented for the last week of the year. It was a great place to get some much needed R&R and the perfect atmosphere for reflection and goal setting for 2016.

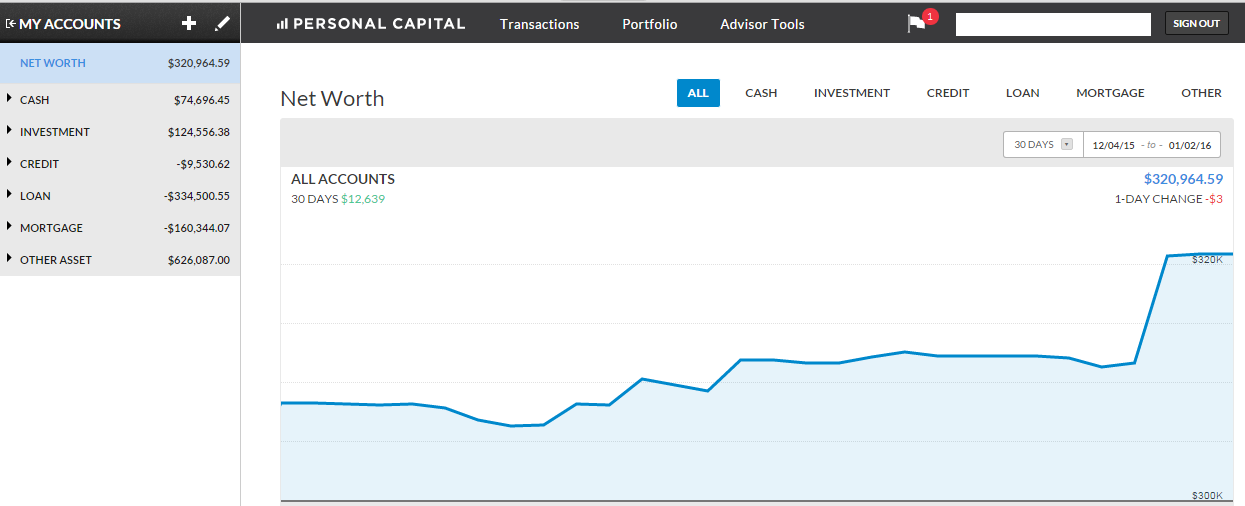

We use Personal Capital To Track Everything

I will continue to add screenshots of my Personal Capital account as another level of TRANSPARENCY in the numbers that I share. I forgot to take a screen shot on the last day of the month (AGAIN), so the screenshot below is slightly higher than the actual December ending number due to pay day on the 1st of the month.

We use Personal Capital to aggregate and consolidate our transactions from across all of our financial accounts (checking, savings, retirement, credit cards, mortgages, HSA, and other investment accounts). At the end of the month I then drop that information into my financial stats spreadsheet for this monthly report.

We use Personal Capital to aggregate and consolidate our transactions from across all of our financial accounts (checking, savings, retirement, credit cards, mortgages, HSA, and other investment accounts). At the end of the month I then drop that information into my financial stats spreadsheet for this monthly report.

Tracking your finances is, in my opinion, the best way to stay on top of your finances. You can’t optimize what you don’t measure. You can’t make informed decisions if you don’t know what you having coming in vs. going out. Without a holistic view of how much you spend every month, there’s no way to set savings, debt repayment, or investment goals. It’s a financial freedom must, folks.

Personal Capital (which is free to use) is a great way for us to systematize our financial overviews since it links all of our accounts together and provides a comprehensive picture of our net worth. If you’re not tracking your expenses in an organized fashion, give Personal Capital a try.

Month Over Month Financial Summary

What went down in December?

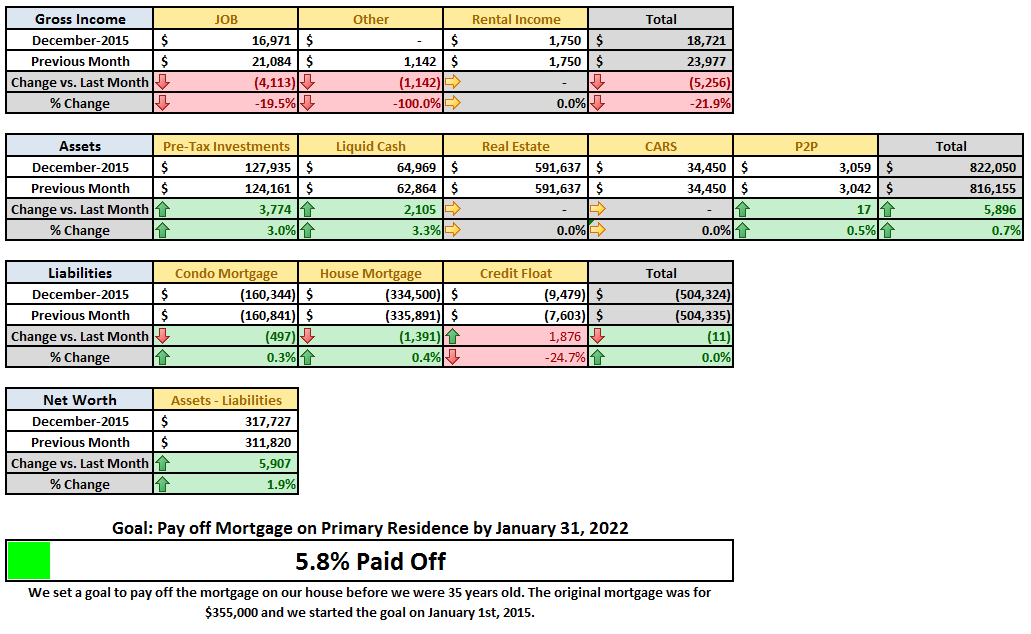

I had only forecasted income at $16,500 for the month of December, but as has been the theme for 2015, we came in higher at $18,721. Again this month it was Mrs. GYFG that help us beat the forecast by $2,200.

Here is a look at the trend for the last 13 months:

For 2015 we realized $254,359 in gross income. If you’ve read my blueprint for how I plan to reach $10M, you will notice that I was actually forecasting a drop in revenue to $178,000 this year vs. $214,142 in 2014. This ended up being a huge favorable swing of $76,359!

I didn’t have us at this earning level until 2019 in the original blueprint…which will obviously need to be updated (post to come probably early February).

Looking ahead, January of 2016 is going to be another all-time record month. Based on what I currently know, it is shaping up to be a $50,000 (or more) month (2X that of January of 2015).

The Juicy Details

- Previous Month: $23,977

- Difference: -$5,256

Income in December was down 21.9%, but it was an expected drop. As I mentioned above, we were only planning for income of $16,500, so it was still $2,200 above our expectations.

Now where did all that money go?

I have come to the realization that there are always going to be unplanned expenses. Our goal is to save 50% of our income and live off and enjoy the difference guilt free. With that type of rule governing our financial life, it is a free pass to inflate our lifestyle, but only proportional to our income. You can see prior financial reports here: January, February, March, April, May, June, July, August, September, October, and November.

Note: The format of this section of the report has been changed to show a better view of month over month expenses and to help reduce the time it takes to put this part of the report together every month. Let me know what you think in the comments below.

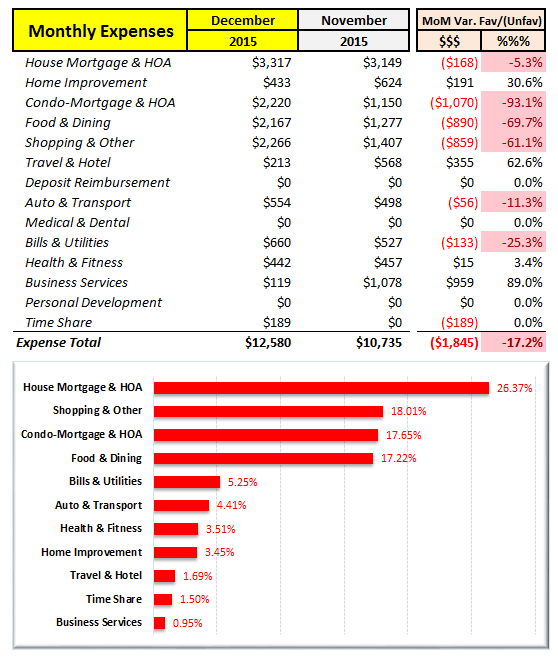

The three major increases for December were for the following 3 categories:

- Condo Mortgage/HOA – Property Taxes were due in the amount $1,070.

- Food & Dining – The holidays were here and we found ourselves going out to eat with friends and family a lot. And a few of those meals were not cheap, but worth every penning.

- We had the best Brunch EVER! We went to the Hotel Del in Coronado for their Christmas Brunch at $90/person. We spent 5 hours there before being reminded that they were closing in 15 minutes. There was so much good seafood and the Bloody Mary’s were to die for.

- We had our annual friends Christmas dinner at Maestro’s Steakhouse in Malibu. Always a great experience…that set us back about $225 as well.

- Shopping & Other – Let’s just say I went a little nuts, but don’t regret anything I bought for me or my wife. It was a good year and we celebrated a bit. We also bought plenty for others.(Mr. CEO here – I am still waiting on my Christmas package – should I follow up with the Post Office?).

Total Expenses $12,580

- Previous month: $10,735

- Difference: -$1,845

Expenses were up 17.2%% this month vs. last month.

Here is the trend for the last 13 months:

What is great about all this detailed tracking that I started this year, is that that it is allowing me to plan for 2016 at a very detailed level.

CALL OUT: It is crazy how slippery money can be. Because of this I totally recommend you automate as much of your finances as possible, especially the saving and investing piece. We set our financial goals at the beginning of the year and then automate the process of reaching them.

Examples:

- Our mortgage payment is automatically set up to pay $800 in additional principal.

- My 401K contribution is automatically deducted at a rate that will ensure I max out by year end ($18,000)

- We have an auto investment of $500/month into my wife’s IRA to make sure we max it out by year end ($5,500).

All of these things take priority over any spending that we do in a given month. We monitor expenses but don’t really manage them. Instead we manage savings and investments and let the expenses work themselves out.

What were Investments and Contributions?

- Contributed $500 to the wife’s IRA for the 2015 tax year.

- Previous month: $500

- Difference: $0

- Contributed $728 Into my 401K [MAXED OUT].

- Previous month: $1,058

- Difference: -$330

- Prosper Lending $0 We have deposited $3,000 so far this year.

- Previous month: $0

- Difference: $0

- Rich Uncles REIT $0 We currently have $5,158

- Previous month: $0

- Difference: $0

- Increase in Savings $2,105 This includes checking, savings, and CD’s.

- Previous month: $6,234

- Difference: +$3,776

- HSA Contribution $1,000 This is set up to max out by the end of the year. We currently have $6,536 here (JUST SHY OF MAXING OUT).

- Previous month: $1,000

- Difference: $0

Total Investments & Contributions $4,333

- Previous month: $8,792

- Difference: -$4,459

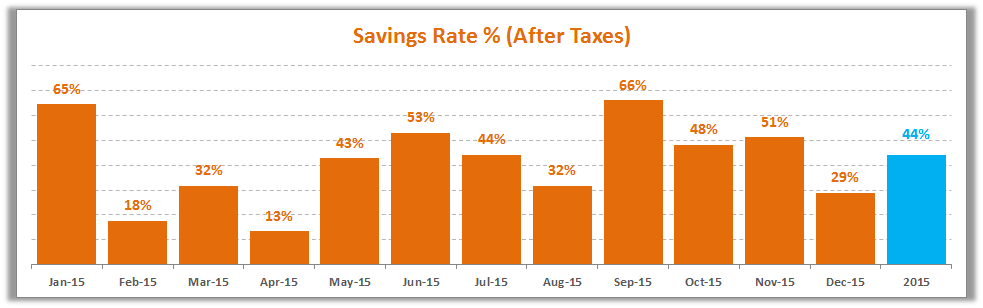

Savings Rate

In July Mrs. GYFG and myself formalized our goal of saving 50% of our after tax income. Below is how we did.

You can see that although our goal for the year is 50%, we bounce all over the place on a monthly basis. We did end up missing our goal of 50% and ended the year at 44%.

I will call 44% a win, since this represents an all-time high for us and we only formalized this goal half way through the year. It will be very interesting to see what we can do in 2016, going in with such a solid foundation.

Speaking of savings rate, have you checked out my recent post where I mathematically prove the importance of your savings rate as a higher priority than the compound return? If you are trying to build wealth quickly, then you have to read this post.

Net Worth and Mortgage Pay Down Update

My ultimate goal is to build up a Net Worth of $10M returning 6% a year or $50,000/month in gross income (at the end of December we are officially 3.2% there). Don’t freak out, this is only about $5.5M in today’s dollars when you take into account a 3% inflation rate.

I am not anywhere close to a 7-figure net worth yet (or what some refer to as the double comma club). However, it is growing at a very respectable rate (just take a look in the side bar for growth at a glance). If you want to see how I plan to get there you can read all about it here (soon to be reviewed and updated in February of 2016).

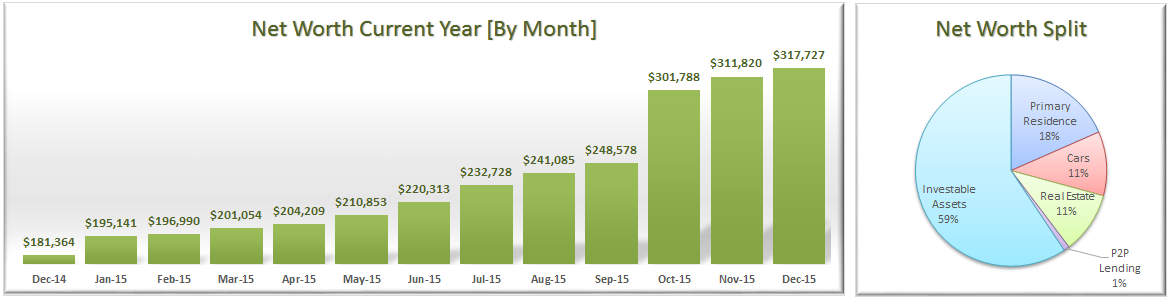

December Net Worth $317,727 (this puts us up $136,363 or 75.2% vs. 2014)

- Previous month: $311,820

- Difference: +$5,907

We were able to post 12 consecutive months of positive gains to Net Worth. Let’s see how long we can continue this trend. The larger the number becomes, the more difficult it will be to continue this trend.

Net Worth Component Break Down:

You will notice that in the second chart above that I have broken our net worth out into 5 categories: Primary Residence, Cars, Real Estate, P2P Lending, and Investable Assets. I want to continue to see our primary residence and cars make up a smaller and smaller piece of the overall pie. Over time I can see myself potentially adding more categories.

Note: I think people tend to glaze over the fact that the savings rate plays a much bigger role in increasing your net worth than the rate of return on your investments (in the early days of your journey). In the short term, savings rate has a bigger impact on net worth. The goal is to eventually build a big enough asset base that the gains from compounding will eventually outpace the gains from savings. Actually, check out the post I recently wrote: Savings Rate – The Most Important Variable to Wealth Building [and the math to prove it]

Progress On Our Mortgage Payoff Goal

You can read about our strategy to pay off our mortgage in 7 years (and 3 months). When you break it down and follow the 3 simple rules, it’s not as hard as it sounds. We bought our house in February of 2014 and then refinanced it into a 5/5 ARM in September of 2014 to remove PMI and free up cash-flow to put towards the principal and keep us on track to pay the mortgage off at an accelerated pace.

The progress chart above shows how much of our goal we have completed. Last month we were at 5.4%, which means we picked up another 40 basis points in December. Those monthly 40 basis point improvements have really started to add up (we ended 2015 with 5.8% paid off vs. 1.2% at the end of 2014).

In a few of the previous reports I had hinted that we may be changing up our strategy of paying down the mortgage. It now looks like we will continue as originally planned. So, starting in January of 2016 the additional $800/month we have been paying will increase to $1,600/month.

There still will be a post dedicated to updating everyone on where we are, our thinking, as well as concerns we will be watching out for closely.

The End

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years of slaving away for the man before you have the option to retire. I personally think that 15-20 years is really all you need, and for the folks that are more aggressive (i.e. extremely frugal, not us) or very high earners you can probably reach financial independence in 10 years or less (maybe us, it’s yet to be seen but income is our focus vs. expenses).

I am looking forward to chatting with you all in the comments below. How was your month? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

One last thing before we go. If you are new or even if you’re not new and you have been wanting a more guided tour of the blog, I finally launched a “Start Here” page. I highly recommend you check it out.

Cheers!

– Gen Y Finance Guy

PS: Here are my favorite ways to track this stuff:

- The “Financial Stats” spreadsheet – a simple Excel template I created to provide the tables and charts you see in this post as well as on the Financial Stats Page. If you would like a copy of this spreadsheet, sign up for my email list (sign up form in the right side bar) and I will send you a copy.

- PersonalCapital.com (free) – I track everything in Personal Capital and then enter into my custom Excel template. Check out my Personal Capital Review to see if its right for you.

11 Responses

Congratulations, thank you for the detailed statistics, i also will start to track my expenses, let´s hope the best!

Thanks Robert! You will find that tracking is very beneficial.

What an interesting start to the year! I love it. Mr. Opportunity isn’t here yet, but another couple days like this one and he’ll be knocking on my door.

What do you think?

It has been a really interesting start to the year!

I sat on 50% cash on average for most of 2015 until the August melt down. Took advantage of the decline and volatility…but ended the year with almost 80% cash in my brokerage accounts…not counting the mounting cash stockpile in the bank (still finished up 4.6% vs. total return of SPY of 1.25%).

I don’t think we will hit new highs this year. We should see way more volatility than last year…it will be the theme in 2016 (I think).

It is going to present some great opportunities for premium sellers like myself. I actually found one such opportunity today. I sold the SPY $194 put for $16.60 and the $195/$225 call-spread for $11.25 (using January 2017 expiration). In total I collected $2,785 in option premium and set up a huge range of profitability. This position makes money anywhere between $165.66 to $223.25. Anything below $165.66 and I start losing money (that is my effective long price, which is 22.5% off the all-time high of $213.78). On the upside, the most I can lose is $364 (losses don’t start until beyond $223.25).

Here are what the probabilities are currently predicting: There is a 60% probability of touching $165 on the SPY with only a 26% probability of touching $225 between now and January 2017 expiration.

This will be my core position that I trade around. I really hope we get to the lower end of the range so that I will have more opportunity to load up the boat on short option premium. One thing you need to know about my style of investing is that I try to remove as much of the directional risk as possible and just cash in on fear via option premium. Higher volatility allows for wider profitability ranges to be set up. I just put them on and what for the value to decay. In low volatility environments there is not as much premium to be extracted from the markets, but in high volatility it is VERY NICE.

However, I only think this is the beginning. There should be much better opportunities ahead. But today I executed tier 1 of my 4 tier system (slightly ahead of the -10% off the high price target).

“We should see way more volatility than last year.”

Yeah, there sure is a lot of sh*t going on.

Regarding your option plays, all of that stuff sailed right over my head. Some day, I’ll get around to studying it like we discussed in San Diego.

I mentioned that I may be back in your ‘hood. I just learned today that the meeting is on Wednesday, 2/10. I’m not excited about the date and am still trying to figure out if I’m going. I’ll let you know if I make it: http://www.valuewalk.com/2016/01/daily-journal-annual-meeting-2016/

Here’s to a profitable 2016! Onward and upward!!

Is the income just your income or is it combined income with your partner?

John – the income you see in these monthly reports is combined for my wife and I.

A tidy little end to the year there Dom! While I’m sure you would have liked a higher savings rate sure you picked it up at the start and into 2016..

Great year 2015 was from the looks of it.. Congrats 🙂

Jef – All things considered it was a great year. We didn’t actually land on the 50% savings rate goal until the middle of 2015 sometime, so it was a good attempt to get there.

We should be really close in 2016, and 2017 should see a significant increase in savings rate over 50%.

Cheers