It’s been three months since my last financial update and this is the first report in the new quarterly cadence. This month includes several major milestones to celebrate:

(1) We sold our prior primary residence.

(2) We used the net proceeds from the above sale to pay off the mortgage we assumed when buying our dream home.

(3) The above two actions allowed us to become 100% debt free again! (besides our credit card balances that we pay in full every month)

(4) We deployed over $1M in a single month.

It may not seem like it was a quiet quarter for the GYFG household but it certainly felt quiet, while also being very productive and massively impactful. One of the investments made allowed me to finalize my 2022 tax planning, about which I will go into more detail below. It also marked the sixth month in a row that I didn’t work over 40 hours a week, a goal I set just prior to closing the sale of 60% of my business last year. This was coming off of almost a decade of 70-80 hours a week (on average – certainly had 90-100 hour weeks sprinkled in there). This is one of my proudest accomplishments, because it means that not only did I pull off my financial goals but also that I’m delivering on my promise to myself to ensure it wasn’t at the expense of my family. This is exactly where I planned to be at this stage of my family life.

The next major transition happens in October of this year when Mrs. GYFG and I will both be going down to four days a week, or to ~32 working hours.

Once upon a time I wrote a post titled Don’t Get So Consumed Building Wealth That You Forget To Build A Life and like all my writings it was a way to remind myself (along the way and at the appropriate time) that all of this hard work has a purpose, which is to LIVE LIFE BY DESIGN! And that is just what the GYFG family has been doing this past quarter, growing into the life we designed many years ago. I’d be lying if I said it’s been all rainbows and butterflies, as life is still challenging when you have two little ones to look after, but LIFE IS GOOD!

I want to start this next section diving into our performance, compared against the plan that I created to fund our desired lifestyle.

THE $10M BHAG

As a quick reminder, in 2015 I put together a rough blueprint for achieving a $10M net worth over 20 years (by the time I was 48). For context, I entered 2015 with a starting net worth of ~$181,000 and a household income of ~$215,000. At the time of publicly announcing this goal, there was essentially a $10M gap between my starting point and where I plotted the finish line. This exercise was really centered around landing on THE number, you know, as in everyone has a “number.” I tried to envision what the composition of what net worth would look like at the finish line paired with the income stream and savings rate required to hit it on the original 20 year time horizon. Seven years later (just 35% of the allotted time) we have achieved 80% of the goal…not quite the 80/20 rule but pretty darn close!

I’ve prepared some charts to help visualize our net worth journey…

Note: The below charts will only focus on performance through the last full calendar year (2021) although net worth is currently $416,753 higher ($8,003,869) than on December 31, 2021 ($7,586,316).

I’ve tracked my gains over time to fall into one of two buckets: (1) Contributions (i.e. savings) and (2) Investment Gains. I actually got the idea from a long-time reader (JayCeezy) to do it this way. I should point out that I include the gains from the value created from the business I founded three years ago that allowed me to turn a very small investment of $267.42 into millions within the Investment Gains bucket. My original blueprint was actually broken up between contributions and gains, which you can see in the side-by-side charts below (actual on the left and planned on the right). It’s interesting to see how heavy the concentration was skewed to contributions through 2020 in our actual performance and how a single year (2021) was large enough to skew the entire time period towards investment gains.

I regularly admit to being conservative in the plans I pull together because there are just too many unknowns, and I want to accommodate for those as best I can. And while I say that in one breath, the results today could have also never materialized and proved the plan very aggressive. That said, I’m a big believer in planning for success and regularly remind myself of the quote that “if you fail to plan, you are planning to fail” by Benjamin Franklin. A plan sets direction and acts as a compass to keep you on course. Like life, the weather can be unpredictable, so the plan shows you where you are and where you’d like to go, and it might even contemplate what may happen on your voyage…but the plan is never going to get it all right. Inevitably we all have setbacks and accelerators that are very hard to plan for…while also not impossible to be prepared for.

My natural bias is one of optimism and positivity so this blog may present a skewed version of reality since the majority of what I write focuses on what is or has gone right. I believe this mindset helps me live my best life, believing that “where your focus goes your energy flows.” I believe that if you focus on what is working you tend to have more success than failure. Maybe it’s the rose-colored lenses I wear through life but I do know people that tend to do the complete opposite, obsessing about their setbacks and unlucky breaks. From my perspective that tends to create a dark cloud that follows them wherever they go…actually more of the “something wrong” they are focused on. Perception becomes reality!

I’d boil down the three major drivers in the acceleration of progress towards this goal as follows:

(1) The business piece of the pie I contemplated back in 2015 performing far better than my imagination could contemplate when the business hadn’t existed yet. It was just a slice of a pie chart back then.

(2) Income grossly outperforming the original assumptions. You all know how obsessed I’ve been with increasing our income over the years. And #1 above has played the lead role in this story.

(3) Mindset! (full stop)

Financial Dashboard

I remember when I first created this financial dashboard back in 2015 and how that first update I shared had us at less than 2% of the way to our $10M goal. Here we are, seven years later, 80% of the way there. The most astonishing thing to me is the compound annual growth rate (CAGR) we have been able to maintain since 2012. Our income has grown at a robust 40% CAGR. Even more mind-blowing is that our net worth has been compounding at a 76.2% CAGR during that same time period. From the end of 2012 through March of 2022, we’ve grown our net worth by 18,764%. To put that in perspective, our net worth has doubled more than eight times in the last decade! AND 80% of the $7,960,645 in net worth increases between December 2012 and March 2022 have happened in the last three years, which also happens to align with when I started my business. The magic of owning a business is that you get to double-dip, enjoying a salary, profit distributions, and a more tax-efficient life, while at the same time building equity based on some multiple – on revenue or profits depending on what industry you’re in – of past results (adjusted with some assumptions of future performance in relation to past performance).

For example, let’s say you have a consulting business that generates $1M a year in profits and that you’ve been running it for at least three years. During your tenure of running the business, you paid yourself a $250,000/year salary and you own 100% of the company so you get to reap all the profits every year (ignoring working capital needs for this example). Also to simplify the example let’s assume that from day one that you were generating $1M a year in profits. So, over three years you got to enjoy $750,000 in cumulative compensation in the form of salary and $3M in profit distributions for a total of $3,750,000. That by itself is a pretty sweet deal but that’s not all of the sweetness. Your business now is established with three years of history and has further value for you to extract. Multiples are all over the place but let’s assume that you find an interested buyer and they are willing to value your business at 5X profit. All of a sudden you now have another $5M if you decide to sell. There are an infinite number of permutations to this example but I think you get the point of how owning a business allows you to double-dip.

TTM Gross Income

The income figure I like to track most is our Trailing Twelve Month (TTM) gross income. As expected, we hit another all-time high in January of $3,787,626. I expect to make one more all-time-high in September when I receive the final payment for the sale of my business last year before an extended decline unless something else not on my radar happens to change that outcome (I wonder what kind of x-factor may be on the horizon). Mrs. GYFG and I were having an interesting conversation about our income expectations for 2023 that would have sounded ridiculous to anyone else listening in…we realized that our income was going to drop substantially from the last two years but that we would still likely be able to realize a low seven-figure income in 2023.

Net Worth

Current Net Worth: $8,003,069 (up $416,753 or +5.5% for 2022)

Previous Quarter: $7,586,316

Difference: +$416,753

The majority of our net worth that isn’t cash or stocks only gets re-valued periodically and we fully expect to periodically have large and lumpy changes up or down. To further punctuate this, I have ~$1.7M in investments that are being held at book value.

Net Worth Break Down:

Real Estate (19%) – This is a mixture of private placement deals, equity, debt, and crowdfunding.

Primary Residence (19%) – We have officially sold our old home and used the proceeds to pay off the remaining mortgage we assumed when buying our dream home. Since late 2020 we have now plowed $1M of cash into this home and our portion is currently worth ~$1.5M. We expect to spend an additional $200,000 to finish up our list of renovations this year.

Net Cash (8%) – We currently have $684,681 in cash vs. $973,180 last quarter-end. A big chunk of this cash is spoken for:

- We made a $250,000 capital commitment late last year for a Cannabis-related fund and still have $137,500 of uncalled capital that will be called later this year.

- We still expect to spend an additional $200K in home improvements.

- Although we think we are covered, the personal tax deadline is right around the corner and we want to be prepared in the event that we made any miscalculations.

Alternatives/Other (18%) – This is a catch-all category that captures our investments in the following: life settlements, Bowery Farming – a vertical farming company, Private Equity Fund, a Wine Village, and Cannabis-related investments.

Business Equity (29%) – This includes the value of the equity I still own in my business – including the remaining sale proceeds I have yet to receive (the next payment comes in September).

Crypto (4%) – This is mostly Bitcoin and some Etherium.

Stocks (3%) – This continues to be much smaller than I thought it would be. I do see this increasing to a range of 5-10% as we move throughout 2022.

Note: I’m noticing that I am biased towards investing in illiquid assets and that is because I like the forced discipline they bring to the table. I continue to see a lack of liquidity as a benefit, not a bug…as long as you can maintain the right amount of liquidity in terms of monthly cash flow and cash in the bank. It’s funny because in my original $10M blueprint I had projected stocks making up ~60% of net worth, but that obviously isn’t the case as my current allocation is only 5% of that target. I do think the stock allocation will increase over time but I have a hard time seeing it getting anywhere close to 60% at my current vantage point.

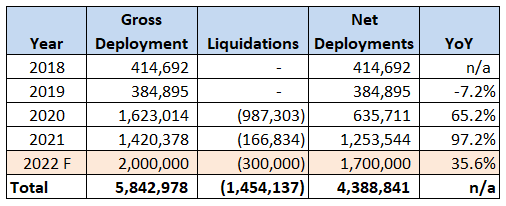

Total Capital Deployed in 2022:

It has already been a big start to the year but as you can see from the table I carried over from the December report below, it is not unexpected – with $1.7M in net deployments having been expected this year. This is the first time we have ever deployed seven figures in a single month and I don’t anticipate it will repeat itself very often. The solar investment is the standout at $720,000 and that is only 60% of the $1.2M commitment that I made. It is the second-largest single investment I have made to date, with the runner-up at $480,000 made in 2020. The investment was large because it also helped me address a large tax liability for 2022 based on projected income of almost $3.3M for calendar 2022. It is split 60% in 2022 and the remaining 40% in 2023.

Here are the characteristics that made the solar investment so appealing to me:

- Dividends of $549,798 split 60/40 between 2022 and 2023 to align with capital deployed…well, almost; a small stream continues through 2028

- $312,000 in Solar Tax Credits, which can be used to offset any type of income including W-2.

- $1,044,000 in bonus depreciation (87% of $1.2M investment per IRS calculation).

- Will shield the entire dividend stream.

- The remainder can offset passive gains like the $1.7M I receive in 2022 related to the equity I sold in my business last year.

- Paid back within 12 months on each deployment

- Exit Return ends up somewhere between 18-20%

Dividends + Tax Credits + Bonus Depreciation = $549,798 + $312,000 + (1,044,000 * 52.65%) = $1,411,464

Note: the 52.65% represents the highest marginal tax rate that we fall into (37% Federal + 2.25% FICA + 13.3% CA State).

Every time I make an investment I liken it to planting seeds that will one day yield a future liquidity event (size unknown). I mentioned in December when I first shared the below table that I knew we would have some sort of liquidation but didn’t know what…we sold our house and that caused a $720,000 liquidation and there could be others on the horizon.

Closing Thoughts

It’s been a great quarter all around. All I need is another five quarters like this last one and we are at our goal…but I’m highly suspicious it will be that easy. The GYFG family will continue focusing on growing into the life we have worked so hard to be able to live. It continues to be a blast to see our home transition week by week. We reached a point towards the end of February when we were officially ready to start having guests and as we wrap up more of our projects we plan to increase the frequency and amount of guests that we host at our private little resort we are creating. The next big project we are tackling is the remodel of the pool, with an addition of a spa and full outdoor kitchen – figures crossed we get to enjoy it for at least part of summer.

Cheers,

– Gen Y Finance Guy

2 Responses

Love the update Dom! I’m excited to hear more about your home renovations and the dream resort you’re creating.