I know I say this every month but I can’t believe another month is in the rear view mirror. The first week in April was very tough with the loss of my mother-in-law as she lost her battle with cancer. The grieving process is nowhere near done but each passing day and week is getting easier…although there is nothing easy about losing a loved one. We continue to remember the good times and hold onto those memories and stories when the reality of loss gets us down. There is also a bit of guilt that we are all fighting as we continue living our lives. We know that this is what my mother-in-law would want us to do but it doesn’t prevent those of us that were closest to her from feeling guilty about moving on and living life again. There is a surreal aspect to it as we move on back into life. Death is an unfortunate part of life but it is also what makes it so precious.

We continue to turn to the expected arrival of our baby girl in September as the light guiding us through this difficult time. We also continue spending lots of time with my father-in-law to support and comfort him as he processes this devastating loss. His grieving process will no doubt take longer than that of anyone else as he lost his soul mate and the woman he had been madly in love with every day for the last 47 years. No relationship is ever perfect but we are all in awe of how special their marriage was. We (Mrs. GYFG and I) are so inspired by their relationship and we are not the only ones. There have been so many stories shared from friends and family about how palpable their love for each other was.

My biggest takeaway from this experience is to remember to live, love, and laugh often with those I care about most. I know this blog is narrowly focused on personal finance but please don’t forget that the big “WHY” behind everything I share about money is all about living life by design. Money is only a means; not an end. It’s the resource that gives us the optionality to spend time in a way that fits our life vision. It’s about having the resources and the freedom to live well and give well.

For example, because of all the hard work and discipline we have built into our financial lives, we didn’t hesitate to give the bed that cost us $10,000 to my mother-in-law to help bring her comfort as her health deteriorated and to spend another $5,000 to buy a new bed for ourselves. Also, I’m grateful that I didn’t have to choose between showing up for family vs. showing up to run my business. My business ran fine without me as I took a major step back in March and early April to do whatever my wife and her family needed from me. That meant picking up lunch and dinner. Picking up friends flying in from out of town to say goodbye. That meant pitching in more to take care of our son so my wife could spend as much time with her mom as possible. It was making calls and sending texts to keep people updated about the status of my mother-in-law. It was spending afternoons and evenings comforting family and friends as we shared great memories.

There will certainly be additional losses in our future and other bad things that happen in life and I accept that. That doesn’t mean I will consume my days worrying about what could or eventually will happen because that isn’t congruent with a life well-lived. We accept reality, but we will still choose to live!

With that, let’s dive into the financial update, and go through the details of what allows the GYFG family to live well and give well.

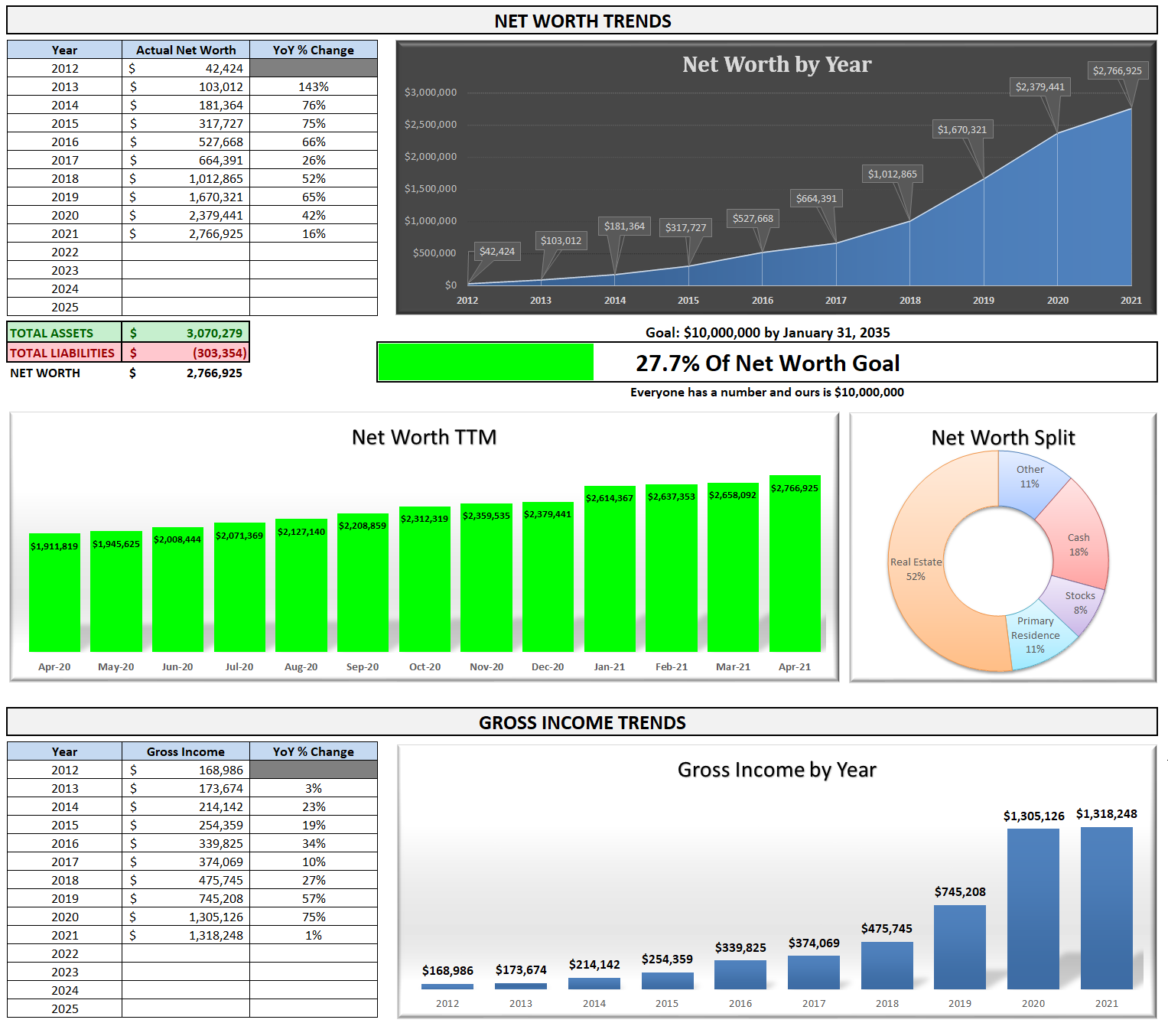

Financial Dashboard

I remember when I first created this financial dashboard back in 2015 and how that first update I shared had us at less than 2% of the way to our $10M goal. Here we are, six years later, at 26.4% of the way there. The most astonishing thing to me is the compound annual growth rate (CAGR) we have been able to maintain since 2012. Our income has grown at a robust 24.3% CAGR. Even more mind-blowing is that our net worth has been compounding at a 65.1% CAGR during that same time period.

Note: I’ve finally got the confidence to forecast an income in 2021 that will be higher than what we earned in 2020. That is even after accounting for the large $415,000 capital gain we had in February of 2020. A large part of this increase is coming from Mrs. GYFG who is absolutely killing it in Real Estate. The other is based on a little more visibility that I’ve gained in the performance of my business through the end of the year. Nothing is guaranteed but I have a strong level of confidence that we can hit this forecast income figure.

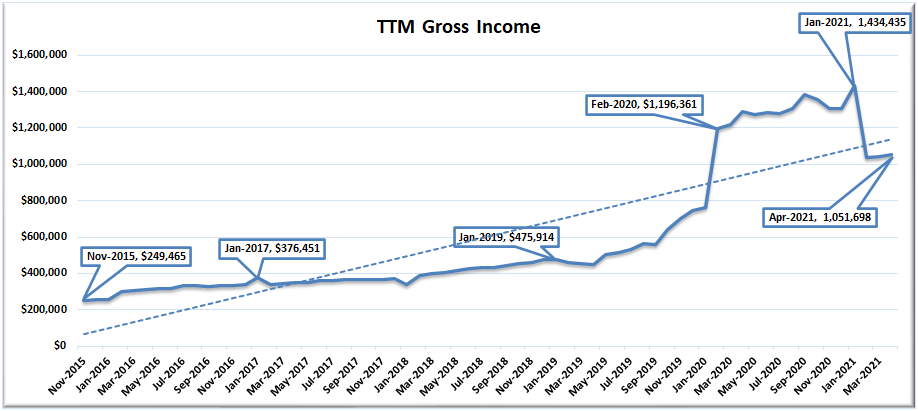

TTM Gross Income

The income figure I like to track most is our Trailing Twelve Month (TTM) gross income. After falling off a cliff in February we continue to climb towards our previous peak in January of 2021. It’s going to take us the rest of the year to get anywhere close to that previous high, but now that we are on track to match our income for the calendar year 2020, it’s now time to find another $150K to make a new TTM high (I’ve got a few tricks up my sleeve that I’m working on to do just that).

Net Worth

Current Net Worth: $2,766,925 (up $387,484 or +16.3% for 2021)

Previous month: $2,658,092

Difference: +$108,832

A fairly large portion of our net worth only gets re-valued periodically and I currently think our net worth is understated, which means we will periodically have large and lumpy changes to our net worth.

Note: I’m still not holding a value for my business in my net worth. Depending on the multiple you use, the value of my business is somewhere in the range of $820,000 (1X EBITDA) to $8,200,000 (10X EBITDA). You’ll notice that I’ve moved the upper range of this shadow valuation to 10X from the previous 5X. Internally we still value the company at the conservative 5X, but the longer we sustain our triple-digit growth profile the higher the potential multiple, especially paired with our robust profitability. I’m hesitant to hold a value in my net worth for this until we achieve a liquidity event. That being said, below I’m going to start holding a “Potential Net Worth” figure as I think we will likely achieve a liquidity event in the next 12-18 months.

Potential Net Worth: $5,226,925

^This values the business at 5X EBITDA implying a value of $4.1M in total Economic Value (EV). I then multiplied the EV by my fully diluted ownership stake of 60%, which potentially adds $2,460,000 to our net worth.

Net Worth Break Down:

Real Estate (52%) – This is a mixture of private placement deals, equity, debt, and crowdfunding.

Primary Residence (11%) – I decided to split this out on its own because it is something I do want to manage separately from our overall holdings in Real Estate. Our primary residence currently makes up 12% of our total net worth (down from 23% in September 2020) due to a cash-out refinance (locking in 2.8675% for 30 years) that put a mortgage back on the property. I expect the concentration to continue its downward trend until we move into our new house in October of 2021.

Net Cash (18%) – We currently have $492,000 in cash vs. $466,000 last month.

Alternatives (11%) – This is a catch-all category that captures our investments in the following: life settlements, a special purpose acquisition company (SPAC), a private investment in the Robinhood trading platform, and the newest addition of Bitcoin.

Stocks (8%) – Our 401K accounts are maxed out and we don’t have any new investment planned here for the year. The only thing that could tick this up is when we get the shares from a SPAC that we participated in that currently sits in the alternatives bucket above.

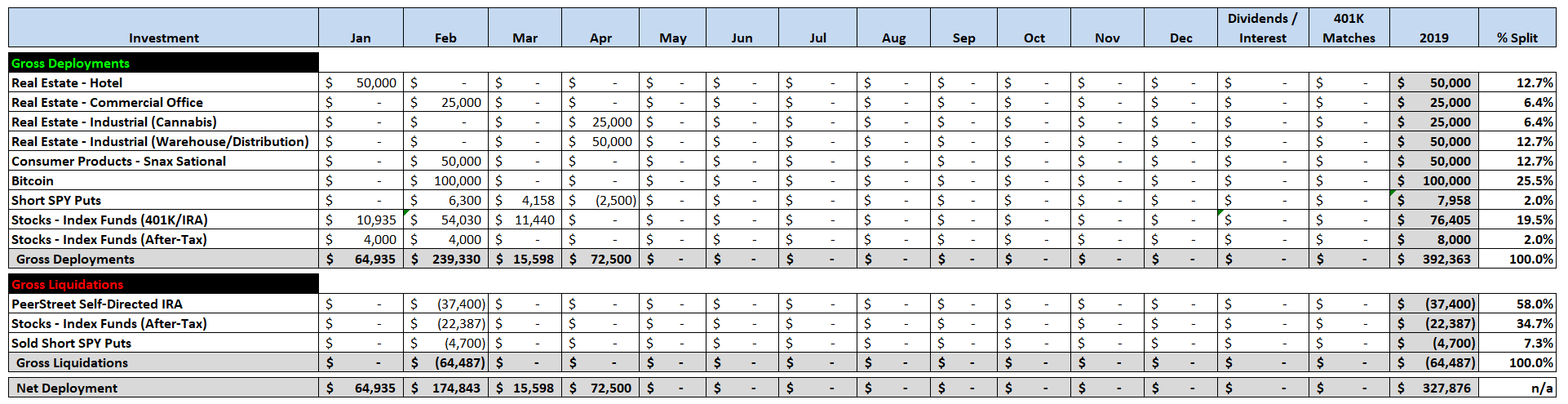

Total Capital Deployed in 2021:

Towards the end of the month, there were two Real Estate deals that I participated in through the CrowdStreet investing platform. Our real estate holding company now holds about $715,000 in real estate assets (at cost) with an expected cash flow of $120,000 per year or 16.8%. The holding company doesn’t hold all of our real estate assets but this is a large chunk of it (~41% of the total $1,741,978 that is allocated to real estate including our primary residence).

There are a number of liquidity events that I’m expecting later this year:

(1) $75,000 hard money loan at 10%. The original loan was for $150,000 and was made back in November of 2019. Half of it was paid back six months ago and I expect the remainder sometime in the next couple of months as the last property securing the loan is currently being listed for sale.

(2) Robinhood Investment. I invested in a round led by Sequoia Capital at a $8.3B valuation back in July of 2020. The last round they raised in August 2020 was at an 11.2B valuation. They announced that they would be filing for an IPO in 2021 and some of the chatter is that it could go public at a $40B valuation. I’m not going to make F-U Money but my $10,000 could turn into $40,000+. Only time will tell.

(3) Life Settlement Policies. I invested $70,000 across seven policies in late 2017 and early 2018. Four of those policies are now past the expected maturity date. I’ve had to make several capital calls to keep the policy active as the insureds have lived past the expected life spans. If all four policies payout this year, I will receive $59,300 on an original investment of $40,000.

(4) $38,000 in maturing hard money loans made on the PeerStreet platform. The volume has been significantly less since the Pandemic hit and of the new loans being added to the platform, not many have been matching my criteria of a max 60% LTV and 8% interest rate. Therefore, I have been transferring money out of the two accounts with PeerStreet and the notes mature. On top of that, the majority of my remaining notes are in some form of default.

I could see a continued deployment of capital in the range of $25,000 to $50,000 per month for the remainder of the year (mostly real estate and/or alternatives). That said, it also depends on the timing of our remodel and the cash needs of that, while maintaining a comfortable cash cushion.

Things I’m Loving

After dipping my toes into the cryptocurrency waters in February, I wanted to find a way to gain additional exposure without allocating additional risk capital at this time. I discovered the FOLD card recently, which is a pre-paid debit card that allows you to earn bitcoin as a reward on all your purchases. I’ve been using the card as often as I can the past two months and have so far earned ~220K sats (For those not familiar a Satoshi or Sat is a fraction of a BTC. At $58,000 per bitcoin that is $126.49 in rewards). I did sign up for the premium card and it comes with a $150 annual fee but the rewards system is better. The team at FOLD has also gamified the spending so you spin a wheel after each purchase to see what your reward is. I really like this card because it allows me a synthetic way of dollar-cost averaging into additional BTC based on the normal spending I would have done anyway. I also love that the sats you earn have upside as their value is tied to the live price of BTC.

The other item I’m really excited about is the smart bed we recently purchased through Eight Sleep. We had purchased a Sleep Number bed in late 2018 when my back issues were really bad. I needed a much firmer bed and my wife preferred a much softer bed, so we got the Sleep Number to accommodate both of our preferences/needs. We ended up giving this bed to our in-laws in early March as my mother-in-law battled cancer. She was approved for a hospital bed but we wanted her to feel more natural at home and less like a patient in a hospital and offered up our bed to make her more comfortable. This opened up an opportunity to see what new beds were on the market and to address the changing preferences and needs of Mrs. GYFG and me. Mrs. GYFG was never a big fan of the full split we had on our King Size bed. In addition, I run very hot (I sometimes will wake up in a puddle of sweat) and would like a cooling mechanism, while Mrs. GYFG is always cold. As my back has now been healed I don’t need the cement-like firmness I did previously. Therefore, we chose Eight Sleep for its dual cooling system – the bed creates a temperature range from 55 degrees to 110 degrees depending on what your body needs and will adjust through the night as your body temp changes through different cycles in your sleep. It also has a gentle way of waking you up in the morning. We haven’t received the bed yet but expect it any day now and we are excited to get it set up.

Closing Thoughts

I’m proud of the financial engine we have built and am in awe as it takes on a life of its own. The majority of the heavy lifting to get the wealth flywheel going is behind us. The focus now is to keep the momentum going by making sure the flywheel stays in motion by periodically making new investments and letting existing investments compound and distribute cash…which then gets re-invested.

I’m obsessively more focused on expending a disproportionate amount of energy on the life side of the ledger. Mrs. GYFG and I are having conversations on how we might do this by allocating additional capital towards buying more time back (hiring help where needed) and buying experiences (with friends and family). We have historically spent an average of $150,000 per year since 2015. Recently I threw out a wild idea: what if we spend an additional $100,000 per year? We would like to spend 40-50% of that on hiring a full-time nanny that can not only take care of baby #2 when Mrs. GYFG goes back to work but also someone that will help with laundry and light cleaning between days our weekly cleaners come. The remaining would be for pure fun with the family and our friends (this is on top of the $250,000 we plan to spend over the next 2-3 years in making improvements to our new house).

Like many families, we have a lot of pent-up demand to spend money on experiences, food, and anything else that brings us joy, and perhaps even more motivation to do so now after having been dealt the worst reminder of how fleeting life is. All the best to you – live, love, laugh, and create the life you envision, always with an eye on your WHY.

– Gen Y Finance Guy

9 Responses

Great report, Dom. That is a huge increase year to date. 🙂 I don’t think it’s a crazy idea to spend an extra $100,000. You can’t put a price on the freedom and time saved having a nanny around, plus the other things you want to do. So I think it’s worth it. What’s the point of working hard for money if you aren’t going to enjoy it during the best years of your life? Good luck with your crypto investment. ????

Thanks, Liquid!

Dom,

Sending sympathy, prayers and hugs to you and your family on the death of your mother in law. That is so good that you are spending lots of time with your father in law and taking time to emotionally support the family.You’re a great son in law.

Thanks, Heather!

I had no clue you actually was able to invest in Robinhood pre-IPO. If I learned that I could do something like that, I would have put a lot of money into it!

Hey David – it wasn’t open to the public but I happen to know someone that got an allocation and let me participate.

Ah, got it. Great opportunity!

Sorry for your loss. I’ve had some close family losses to cancer the past few years and they are terrible. I’ve been chipping away at the mortgage balance on my second home. It’s a vacation condo near the ocean. I have a small mortgage 150k at 2.75%. Like you I’ve paid places off early, and often oscillate between keeping the mortgages/investing in market. Being mortgage free is pretty awesome though. Is there any rationality to paying this down/off? I say no, but then I keep accelerating payments…haha

Hey Dom,

Sorry for your loss, hope your relentless optimism is serving you guys well during this time.

I’ve been watching your income reports for the last year, and all I can say is wow! Not only the performance of your portfolio and the creatively allocated assets, but your reports are super detailed and easy to read, nice work.

As an aside, your guest post link doesn’t seem to be working, but I guess that means you’re all set for now. Keep us posted if that changes?

Cheers,

Gary