Time has started to move at an increasingly accelerated pace for the GYFG household. It might be because of a slow but steady march back to some level of normalcy after months of “lockdown.” Here are a few highlights from May:

- We made a trip out to Lake Meade for the Memorial Day Weekend (with other people).

- We ate in a restaurant not once but three times and were served by…people.

- We had a BBQ at our house with friends (there are those people again).

- We went to the beach with friends and again there were lots of other people.

As you can tell, the theme here was that we were not locked down in our house for the entire month of May and we got to see friends and family for the first time in several months. It kind of felt like that M&M commercial…”they do exist.”

After dodging a few bullets the last few months shot by COVID-19 at most investments, this month we weren’t so lucky. We were notified by Rich Uncles (a Commercial REIT we are invested in) that the net asset value (NAV) had been reduced by ~30% to reflect the current market conditions and the risk they saw in the portfolio in the short term. They also announced that the dividend was being cut from 7% to 5%.

Regardless, we continue to focus on the income side of the equation and were still able to out-earn the write-down and also add 1.8% to our net worth in May vs. April. It’s been a few years since I wrote about this but one of my goals is to get a little richer every year despite the performance of our investments. This means we have to keep pouring jet fuel on income generation.

If you’re a regular reader you know that I typically have a formula to this post, but for the next couple of months I feel the need to change it up. I realize that my family is in a fortunate financial position to weather a storm like this and I feel awkward going through the normal cadence of this report as if everything is hunky-dory in the world for everyone. I want each reader to know that I am hesitant to continue sharing our financial statistics in light of the pain that many are feeling right now. At the same time, I have pledged to continue publishing these reports every single month until I hit my BIG financial goal. It is also important for me to lead by example to continue responsibly managing my family’s finances – through both good times and bad. Furthermore, I think it’s important that transparency is maintained to see how finances are managed in both bull markets and bear markets. That said, I will be removing some elements so it is not as “in your face” when it comes to certain aspects of the normal report.

Net Worth

Current Net Worth $1,945,625 (up +16.5% for 2020)

Previous month: $1,911,820

Difference: $33,806

Net Worth Break Down:

Real Estate (60%) – This is a decrease from the 63% figure last month. This category includes the equity in our primary residence, a hard money loan at a 10% interest rate, our investment in the Rich Uncles commercial REIT, and our hard money loans through the PeerStreet platform. This took a decent (indecent?) hit this month after I was informed of a 30% write-down in my Rich Uncles investment. Certain types of Commercial RE are getting hit pretty hard due to COVID.

Net Cash (29%) – This is unchanged from last month.

{kind=link}

Life Settlements (5%) – Flat vs. last month. We currently have investments in seven policies. They are accreting in value by about $1,000 per month. For anyone familiar with options, I liken the fixed return of life settlements to the theta of a short option. In this case, the accreted value is like the theta decay of an option you’ve sold. In more simple terms, with this fixed return you are amortizing (realizing) that value with the passing of time. Two of these policies have required capital calls as the insured has lived past the estimated life expectancy (which eats into the expected return). I started investing in these policies in late 2017 and have yet to see a return of capital or a return on capital. I have another year before another two policies are expected to mature and if they don’t I will be required to make annual capital calls to those as well to keep the policies in force.

Stocks (6%) – This is up from 3% last month.

Even though we took a sizable write-down in one of our real estate investments we were still able to increase net worth by a very respectable $33,806 or 1.8% for the month.

Total Capital Deployed in 2020:

The plan for the next couple of months is to continue building up our cash war chest. The stock market makes absolutely no sense to me right now. I don’t understand how we can have so many people unemployed, many businesses still shut down, trillions out in federal stimulus money, trillions of dollars being printed by the fed (by increasing their balance sheet), and still no certainty on when this pandemic will truly be behind us (and don’t forget about the riots and protests now). GDP for the first quarter fell at an annual rate of 4.5% with the back half of March being the only period impacted by COVID-19, meaning we have theoretically only seen the beginning of the damage done. Economists are forecasting a 20-30% annualized decline by the end of Q2. The world (still) doesn’t make sense to me right now!

I did put some money to work in a secondary offering for shares in Robinhood (the investing platform). I’m part of a private investors circle that brought this deal onto my radar and so I decided to follow the money – Sequoia Capital led a series F round that raised $280M and valued the company at $8.3B.

You will also notice that I put $9,100 to work by purchasing puts on the S&P 500. I’m working on a post to explain this move and the rationale behind it; now I just need to find the time to finish writing it.

We are currently sitting on about $570,000 in cash and I believe I have found a home for another $181,000 (the amount sitting in an IRA that I rolled over after leaving my employer). I’m currently in the process of rolling this into my self-directed IRA as I am going to be participating in an Industrial Real Estate deal – specifics to come once I make the investment. The sponsor has negotiated a property with about 450,000 square feet of space at $20/sqft. The replacement cost to build the same is about $120/sqft. It is a fire sale deal by a very large public company that isn’t in the business of real estate and just wants it off their books (they got it through an acquisition). More details to come.

Expenses

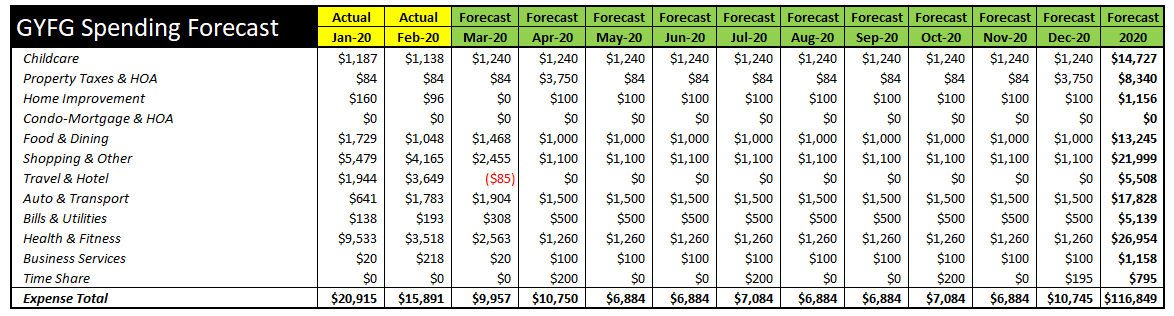

Coming into 2020 I had made the decision to not track our expenses anymore. Well, that lasted for all of two months. I have not had a section for expenses in these financial reports for well over a year, but with the new spending plan my household is adopting, I find it necessary to track our spending against that plan. Each month I will be comparing our actual spend vs. the forecast spend in the screenshot below.

The above table represents the original forecast that I put together for the remainder of 2020 and is the benchmark I will be tracking to. I expect to see more volatility in the month to month figures as our spending is lumpy and not evenly distributed. In May, we were close to being on forecast overall, within $272 or 4%.

The big negative $2,172 stands out on the table above – it’s a credit for expenses that didn’t come out of our personal earnings. This is because I had been entering the cost of health, dental, and vision insurance here on my personal P&L. However, this is an expense that my company pays 100% for and doesn’t come out of my personal finances. To be consistent with when I was employed by someone else, I only ever carried the expense that came out of my personal earnings, not what the company paid.

May did come in at about 50% of April’s spending of $14,459. We are currently trending to $113,335 in total spending for 2020 vs. the forecast from March at $116,849.

Savings Rate

Tracking our expenses means we are back to tracking our savings rate as well. The only difference is I’m going to update it only once a year. Our goal remains saving 50% of our after-tax income.

Below is a historical snapshot of our after-tax savings rate since we started tracking it in 2015.

Do you want to calculate your own savings rate? I’ve made it super easy for you with the savings rate calculator included in the free GYFG FI Toolkit that you can download instantly by clicking the link below. Here’s a peek. Did I mention it’s free? You have nothing to lose and everything to gain, Freedom Fighter! Remember, what gets measured gets managed.

Speaking of savings rate, go check out my post where I mathematically prove the importance of your savings rate as a higher priority in achieving financial independence than your compound return. If you’re trying to build wealth quickly, then you have to read this post.

Closing Thoughts

Although there is still plenty of uncertainty on the horizon I’m grateful for the position the GYFG household is in to weather this Pandemic. I do hope for the best in terms of a speedy recovery for all – health as well as financial – but I’m prepared for the worse. So far, the measures I’ve taken proactively to decreases our expenses have proven not to be needed, but I don’t regret making those moves. We continue to strengthen our position to not only weather the Pandemic but to take advantage of opportunities that may arise due to the damage it leaves in its path of destruction over the world economy.

– Gen Y Finance Guy

4 Responses

Great article GYG!

I’m really looking forward to your rationale piece on the index puts!

Thanks, J!

I’m going to try to get it finished in the next week or two.

Dom

Awesome. GYFG, I’ve always had a bit of dyslexia, and my first pass at “Total Capital Deployed” read as “Destroyed.”:-) Thought you might get a kick out of that, and that is where my head is at in these crazy times. I’m old enough to remember when there were 27 genders, Princess Meghan was considered good-looking, Kobe Bryant was alive, and looters weren’t the good-guys. But I don’t want to dwell Boeing and Congress.

Am liking your explanation of ‘Health & Fitness’ variance and awhile back when you established your company I wondered if you would write that into your company charter.

The REIT revaluation makes sense but it there might not be much point to apply it to the rest of the Real Estate, until the smoke clears. Your savings continues to be on point. Rooting for your continued success!

Hey JayCeezy,

Yes, savings is the one variable we have the most control over. I don’t see similar reductions happening to my other real estate holdings at this particular moment. But who knows…the world is in la la land at the moment – so, anything is possible I guess.

When you have the ability to print as much money as you want I guess weird things can happen – LOL!

Cheers,

Dom