In a previous post, I mentioned that I had recently become debt-free outside of the mortgages on my primary residence and investment condo. In that blog post, I announced an outrageous goal of paying off the mortgage on my primary residence in 7.5 years. I gave you the Cliff Notes version there of the strategy I devised to accomplish this big, hairy, and audacious goal. In this post, I want to expand upon the thinking and get more granular on the strategy. My hope is that by the end of this post you will realize that this strategy is easy and anyone can follow it…even though most won’t. Only those truly hot in pursuit of financial independence will have the discipline and willpower to follow through on this strategy.

To the Victor go the spoils. – Virgil

First, I would like to point out that this is a plan that involves absolutely no austerity to your current lifestyle. I got the idea from a retirement savings strategy referred to as the “save more tomorrow plan.” The premise is that you start with the minimum contribution to your 401K that your company matches, which is typically in the 3-6% range. The goal is to increase your contribution as a percentage of your income in order to max out your 401K (max as of 2015 is $18,000). However, the objective is never to feel any pain during this increase process. So you only increase your contributions every time you get a raise. Because you never spend that increase, you never get used to having it, so you effortlessly eventually max out your 401K. Thus the “no pain” comment.

Although we are talking mortgage snowballs here, I need to state that I have a different philosophy on maxing out your 401K. In my opinion, it’s imperative that you max it out as soon as possible, and ideally, during your first year in the workplace. If you think about it, you’re typically just getting out of college and are making more money than you ever have in your life. Even if you maxed out $18,000 on a $50,000 per year salary, I would wager that you’re likely still making multiples of what you made while you were going to school. Play poor a little longer and get that 401K working for you. You’ll never get back the power of those first years if you don’t. Perhaps I’m a bit biased since this is the path I chose when I first entered the workforce, but it’s worked for me so far. I have been maxing out my 401K since day one.

Nonetheless, I do like the underlying philosophy of the strategy and its application to paying down debt and particularly a mortgage. So let’s dive in and get under the hood of this strategy…

If you have ever heard of “Snowball Momentum” then you will immediately understand why I chose the name I did. The basic concept is that if you start with a small snowball and roll it down a hill, you will gradually get a snowball that increases in both size and speed. As I lay out the fundamentals of this strategy, you’ll see the exponential “snowball” power come to life.

The Fundamentals

Let’s define the fundamentals of this strategy. If you can stick to the framework I have developed, it will make it much easier to adhere to and will increase your probability of success.

(1) Buy a house that is less than you can afford. Most people get pre-approved for a loan during the house buying process. During that process, they find out the maximum loan they can obtain in purchasing a home, and then most people go out and buy as much house as they can right up to that maximum amount of money the bank says they can borrow. In my case, my wife and I were pre-approved for a loan of up to $750K. But we had no intention of buying a house that would require a loan that large. My rule of thumb is to borrow around 2X your annual gross pay (at most 3X).

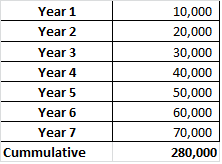

(2) Increase your after-tax income every year. Ideally, you will increase your after-tax income by about 2.9% of your starting mortgage every year. So in my case, with a mortgage of $350K, that calculates to about $10,000 per year. Over seven years that is an additional $280K (2.9% x $350K x 28 = $280K). In the table below you will see that by year seven you are earning an additional $70,000 per year based on this example.

Note: Numbers are rounded for illustration purposes. The income is after-tax because you can only spend what you take home after Uncle Sam has taken his cut.

(3) Practice the “Pay More Tomorrow” strategy. Like in the “Save More Tomorrow” plan, we only pay more to the mortgage in the form of additional principal payments when we get raises. Every time you get a raise, divide that after-tax amount by 12 and increase your mortgage’s payment to principal by that amount. So again, based on my real life example, in year one I would take the $10,000 increase in income (2.9% of our initial mortgage balance) and divide it by 12, resulting in $833 per month paid to the principal of our mortgage. Increase your income more than 2.9% of your initial mortgage? Do what you want with anything above that $10,000 per year increase. Or you could be more aggressive and pay the mortgage down even further, thus getting it paid off even faster.

That’s it. Those are the only three underlying fundamentals to make this strategy work. Let’s take a look at the details over the next seven years based on my own real life example…

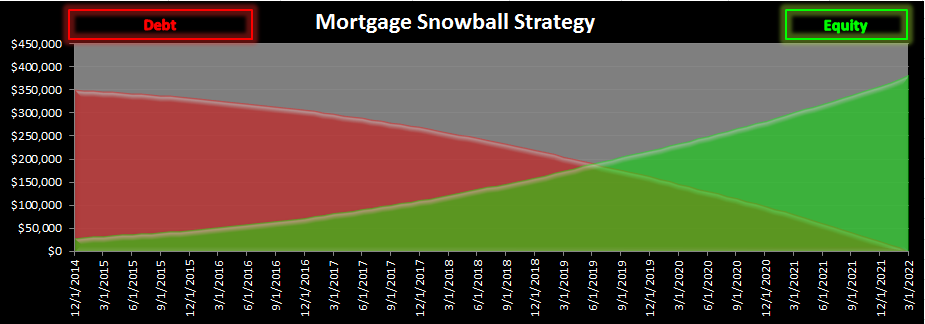

What paying my mortgage off in 7 years looks like

In the above chart, you can visually witness the true snowball momentum or exponential effect of this strategy. Also, I will point out that the equity curve is based on the current market value of $383K per Zillow. We purchased the house for $370K and have an outstanding loan of $350K.

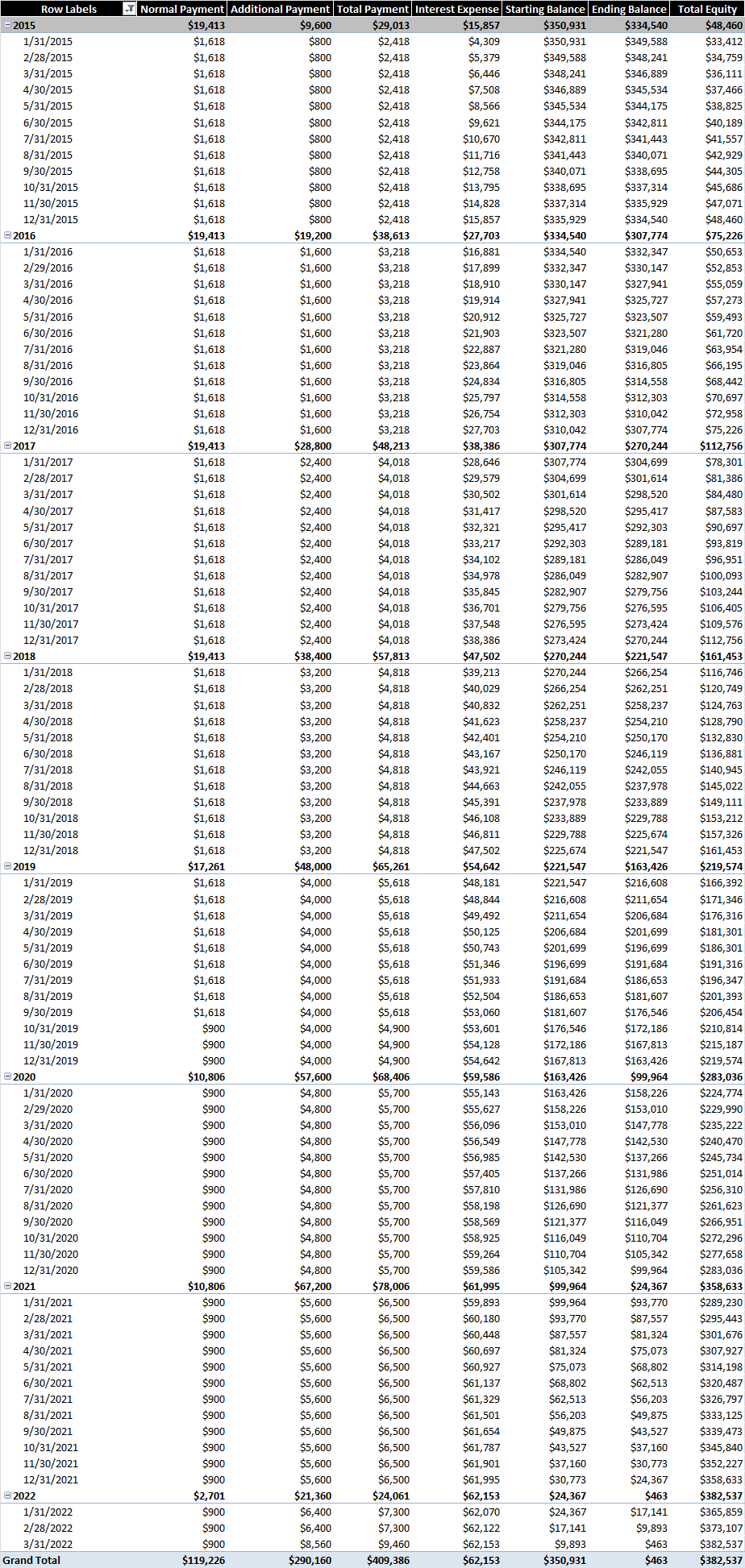

Below is the detailed data table with all the relevant data points by month, with each year representing a yearly milestone.

Remember from my previous post, that it was going to cost us $230K in interest over the life of the loan if held for the full 30-year term, assuming no rise in interest rates. But we have a 5/5 ARM that is impacted by increasing rates. A good point to make is that if our rate was to go up the maximum 5% stated in the loan agreement, as fast as allowed by the terms of the loan, this plan looks even better: by paying it off in seven years instead of the 30, we save an additional $215K in interest savings. Nice!

All savings calculations were done very conservatively, by assuming no rise in interest rates. So with this very conservative example, we will only end up paying $62K in interest. YES! That is a $170K savings based on the conservative base case I’m sharing here.

The awesome part is that we will be mortgage-free before we are 35 years old. This is when many of our peers are either just buying their first house or are still in the first decade of their 30-year loan. More and more of our generation are living with their parents longer, thus delaying the home buying process even longer.

This plan is very easy to do. But it’s also very easy not to do. Imagine the options being mortgage-free gives you if you have just a little discipline and intentional action.

Let me be honest. My real goal is to pay it off in five years, but that is my stretch goal and it may be a bit aggressive (although still worth trying).

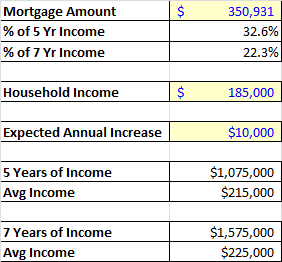

Here are the numbers that made me realize that there is no reason why this wasn’t feasible. Over the next seven years, this strategy will only account for about 22.3% of the cumulative gross income we will earn (see table below). The numbers don’t lie. How can I not do this? 22.3% is not that much in the grand scheme of things. And look, over five years it’s still only 32.6% of cumulative gross income. Some people pay up to 50% of their gross income just to amortize their regular mortgage over 30 years.

So what do you think? Are you ready to put a plan in place to pay your mortgage off early? Can you imagine what life would be like with no mortgage? Let me know what you think in the comment section below.

– Gen Y Finance Guy

Other Posts You Might Like:

Murder Your Mortgage in 7 Years Q&A

Paying Off Your Mortgage Early vs. Investing The Extra Payments In Stocks

82 Responses

This is a great post and I enjoyed the math you provided. We actually own a mobile home outright right now, but we will certainly purchase a “normal” home in upcoming years. I can’t decide right now if I want to pay cash and never have a mortgage, or just have a small mortgage and invest the rest…

That is awesome Jacob! It is for sure a personal choice. You will find people on very opposite ends of the spectrum on this one. But if you ever want to chat about it, let me know.

Thanks for stopping by and contributing to the conversation.

Cheers!

Great job! I have my own home paid off, plus 4 other rental properties so I know it can be done. Squirrel away as much as you can, and live on last years income. Save the rest. I save ~80% of my income, so I know it can be done.

Thanks for the encouragement and reassurance. Since setting a goal to pay off the mortgage I have been finding examples of people who have done it all of the place. Although our savings rate is high, I actually have never taken the time to calculate it. That’s one reason I am going to start putting together a monthly financial report. I know I probably spend way too much money on dinners out and am sure I will find other items where there is room to cut some expenses.

Cheers!

I love this plan, I myself finished paying off all debts (cars, land, college loans). Just had our 1st son so 2013 – 2014 was a wash but for 2015 I’m back on the pay off mortgage early with principal only payments plan!

Good work Big AL. I am glad you like this plan. I personally had my ah-hah moment when I realized how much money I would make in the next 5-7 years and compared that to the mortgage. I figured it was a not brainer to pay the thing off. As you read over 7 years it is less that 25% of my gross income. And its structured in such a way that you don’t fell any pain.

Would love to hear updates as to how the mortgage pay down is going.

Cheers!

This sounds like an awesome plan. I too have been thinking about way to pay down extra principle quickly and this might be something worth considering. Regular old amortization tables are depressing, I will be following your progress closely.

Hey Brian,

Thanks for stopping by. I have always been a strong believe that the math doesn’t lie. When I realized that I would be making $1.4M over the next 7 years. I realized that I would be irresponsible not to pay off the $350K mortgage. It ends up being about 22% of the gross income over that 7-year period. In all reality like I mentioned in the post, I am really shooting to have this bad boy paid off in 5 years. This will likely mean that we apply a few lump sum payments through out the years.

You mentioned that you will be watching closely. Be sure to check out my monthly financial report as well as the financial stats page, as this is where I will be reporting everything for others to follow along with.

Also let me know if you decide to do this or something similar.

Cheers!

Hey, thanks for an insightful post. It’s a really interesting idea, that I never heard of before. I hope you’ll manage to pay it off in 5 years, that’d be awesome. Paying 32.6% of your cumulative income for the mortgage seems more than feasible, and it’s definitely true that many people pay close to 50% of their income for the mortgage (I know a bunch); I am not sure for now if this is something we’ll be doing, since we are in a period of time when we’ve decided we need all the cash we can get in order to make real estate investments (that’s why we chose a low mortgage extended over 30 yrs). Maybe in a year or two we’ll feel like we don’t need the cash and we can spend more on higher mortgage payments. It’s definitely something worth considering.

Thanks Felix!

We are kind of on a dual path. I came up with the pay more lat strategy so that we can still allocate money towards other investments. I look at it as just an allocation within a bigger portfolio.

Instead of bonds this is my safe portion of my portfolio.

I am looking forward to report how it goes.

Cheers!

It’s nice if you can do both. For us, this year we won’t be able to save us much as usual, since my spouse quit and is doing student teaching to start a new teaching career in fall (and you know the kind of salaries they get…). I’m looking forward to your progress!

Great post GenY…like how you illustrate the numbers and especially like the “pay more tomorrow strategy”!

We are debt free and have been contributing to both our 457K, Roth IRAs, and dividend stocks account. We’ve thought about paying more towards our mortgage to pay it off sooner, but we have a 15-year mortgage at 2.875%. Although seeing the mortgage balance drop each month is rewarding, its hard to put our extra funds toward the principal when the interest is so low.

As the market continues to climb back up to record setting levels, and stocks become a little less attractive, we may start putting some monies toward our principal rather.

AFFJ

Thanks AFFJ!

Sounds like you guys are doing well. You already have a bit of an accelerated mortgage pay down being that you have a 15-year mortgage. And 2.875% is a great rate.

We too are maxing out a 401K, an IRA, and looking to also add another investment property in the 2nd half of the year. Just need to get taxes done to see where we land, if you know what I mean.

And like you mentioned with markets at all time highs, I would rather divert capital to pay off the mortgage. I look at the extra capital I allocate to the mortgage as my “bond” allocation, and safe investment. With a 3.675% mortgage rate, that is my guaranteed return for every extra dollar I throw at the mortgage. Plus I am not really one to follow conventional wisdom.

I have gotten lots of questions about why I would give up the tax deduction. But I did the math and I have a post going live on 2/20 that walks through the math. But the short story is that the interest savings far exceeds the lost tax savings over a 7-year period. You really don’t conceptualize that until you do the math.

Anyways thanks for stopping by. Looking forward to seeing you around.

Cheers!

Awesome plan, there is definitely something to be said for the freedom of being debt free. However your plan doesn’t seem to take into account the taxes you will pay on the income increase every year. Also, being a little long in the tooth myself, I have seen that one of the positives of say a 30 year mortgage is that years down the road you will be making payments with cheaper dollars. Because of inflation your mortgage payment will not be as great a percentage of your income as it is now, and hopefully inflation will also increase the value of your home. Perhaps ones net worth would be better off if you took the extra money you would pay towards the mortgage and invest it in the same asset class (investment real estate)?

Hi Frugal Senior,

Thanks for stopping by. You make a good point, that there is definitely a psychological aspect of being debt free. Not sure you can put a dollar value on it.

Your right, I don’t really address taxes related to the increased income. Unfortunately, those will be something to manage and pay whether I proceed with this plan or not. Over the 7 year period I did the math and I will end up paying an additional $10,559 in taxes by paying off the mortgage early (and as you pointed out, there is also in increase in taxes related to the additional income). However, over that same 7 year period I will realize about $27,000 in interest savings. So with respect to total money out of pocket, I am still better off paying the mortgage off early. And over the life of the loan I am saving anywhere between $171,00 and $386,000.

I actually don’t have a 30 year fixed mortgage. Instead I have a 5/5 ARM at 3.675% and am considering a refi towards the end of the year into a 5/1 ARM that would get my rate down to between 2.25% and 2.5%.

You can see my follow up post with the math here:

Regarding a better use of the extra money

It is a very good and valid point. Debts tend to get cheaper over time because of inflation. And most financial folks will advise you to put the money to work for you in the market that historically has returned 8%. And I get it, I am a Finance guy. However, I look at the extra principal as if it were a bond allocation in my portfolio. The equity in my house currently represents about 16% of my net worth. I would re-evaluate if this number started to climb north of 40%. But since I am not following this plan in lieu of investing in the stock market and other investments that could yield more than the rate I pay on the mortgage, I really don’t think this will be the case.

Additionally, we do plan to look to add another rental property (we have one already) sometime in the next 6-12 months. I am not opposed to having leverage. But I would rather not be leveraged more than 3X my annual income, that’s just a personal preference.

I really appreciate the questions and your participation in the conversation. I hope to see you around more often.

Cheers!

I paid off the first 50% of my mortgage in about 2.5 years from when I bought the place. I have a 5/1 ARM and would love to have it paid off before the rate resets (I have just under 3 more years until that point). We’ll see how life plays out in the next few years! It is most likely completely realistic provided that I keep my current income.

That is awesome Leigh. It sounds like you are pretty committed, so there’s no doubt in my mind that you will get paid off.

We have a 5/5 ARM that we just refinanced into in September and bought the house in February of 2014. I am actually considering refinancing one more time by the end of the year into a 5/1 ARM because at 2.25% we could save another $300/month that we can then throw against the principal.

Thanks for stopping by!

I like your way of thinking. I owe about $160,000 on my condo. I have about 50k in stocks I’m thinking of selling, and then accelerating payments kind of like your graphs. Right now I’m at 3.75% 30 yr fixed at 35 yrs old. Would like to be mortgage debt free as soon as possible!

Hey DD, glad you like the plan. I think now is a good time to sell stocks to book profits. The only caution I would give is toast sure you set enough aside for the tax hit on your profits.

Other than that, I say kill that mortgage.

Cheers!

Nice detailed post. I like the idea of paying the mortgage off. I am taking a slightly different approach on managing my assets than many financial pundits (including myself, as I am a financial advisor) would disagree with. I would NEVER recommend any of my clients, friends, or family to do what I am about to mention. So full disclaimer, no one should follow this advice, but just thought it would put an interesting perspective 🙂

I will NEVER pay my mortgage off until I am more wealthy than I know what to do with. The current cost of carrying my mortgage is around 2%, net of tax deduction. I can pay 2% a year and have leveraged gains on my property. In fact, I plan to pull the equity out often. Now, with the extra money I am intelligently investing it, not out buying extravagent things. I am also paying interest only. I am currently paying $1500 a month in interest, which net of taxes works out to around $800 a month, $1300 after HOA. The cost of renting my condo, which is a base/cheapest rental you can find in my area, would be around $3500. I will use the difference to invest it in the market.

Secondly, I will only contribute up to the match in my 401k. $5000 contributed to a 401k on an annual basis compounding at 9% will turn into roughly $1,078,000 in 35 years. This amount will still need to be taxed. Conversely, $3300 contributed to an after tax account (the equivalent of $5000 pre tax) compouding at 10% will turn into roughly $900,000, which is after tax money. There are lots of other things to consider obviously, but essentially I need to do 1% better a year than my 401k for it to make sense for me to not contribute. The way I do this is kind of complicated, but involves using free leverage that costs me absolutely nothing to carry with no chance of a margin call. I alo expect to do markedly better than 1% over the indices.

There’s a couple of other unconventional things I am doing as well, but just dropping a couple lines to stir the imagination 🙂

Hey Sean – Glad you liked it.

Actually, as a Finance Guy, your strategy actually makes a lot of sense. Money is cheap and with inflation your debt will only get cheaper over time. You don’t risk having a bunch of capital tied up in your house in the event some unexpected event happens and your income temporarily.

Regarding 401K contributions – Again, I get this. Instead of locking all your money up until your are 59.5 and as a hedge against higher tax rates, I can see why you would only want to contribute up to the match.

Curious to get more insight into the “free leverage” and your overall strategy.

Love unconventional.

I know you are a new reader, but in my last two financial reports I have alluded to a change in execution to the early payoff goal of the mortgage. You may like the content coming up in the future. It involves using the very controversial “Whole Life Insurance” as part of the strategy. It is going to make for some good fodder.

If you are ever up for a guest post to walk us through some of your unconventional plans, the door is open. And we can keep it anonymous as well.

I am not sure if you were the one that asked me, but I created a Start Here page that walks you through some of the more popular posts.

Cheers!

Great goal! Are you currently living in your forever home? My fiancé and I want to move back to where we grew up so I feel we are in a bit of limbo with our house. Definitely would love to attack the mortgage though.

MB – We think it’s a pretty good goal 🙂

We actually just started year two of the goal in January, so now we are paying an additional $1,600/month towards the mortgage. It’s probably not our forever home as we do have a desire to build our own house one day. We do plan on being here for at least 10 years, and then turning it into a rental.

We were similarly on a 6-7 year plan but your post nudged me to actually do the year-to-year math to take into account:

1) Applying the take-home amounts of our after tax 3%/year estimated raises;

2) 4% annual growth in the conservative mutual fund I want to store this cash in rather than paying down mortgage principal. (My field is volatile and I like the utility of having liquid assets that I can get to if absolutely needed);

3) Withdrawing our original $20,000 Roth IRA contributions as a final step in order to apply those dollars to the mortgage.

With that plan we could pay off the $290K mortgage in just 5 years. It is possible that we would choose NOT to pay off the mortgage until we want to retire in order to enjoy the benefits of further compounding growth of this stash, but there will be great comfort in knowing we could and in having options. Thanks for showing the way, Gen Y Finance Guy!

Glad you found this post to be thought provoking. I actually should have an update post on our own strategy in the next couple of weeks. Since putting this plan in place there are a few other variables that we are now watching and using to guide us in this very systematic pay down strategy. They include:

1 – Liquidity, we want to make sure we don’t risk being ill-liquid by putting to much towards the actual mortgage before we can pay it off. The goal is to keep 1 years worth of bare minimum expenditures in the bank.

2 – Net Worth Concentration, in addition to liquidity concerns, we also do not want to have more than 25% of our net worth tied up in our primary residence. This forces to continue to save an invest outside of just paying down the mortgage. A very balanced approach.

Cheers!

Just looked at most recent statement for my mortgage. My last comment was about 1.5 years ago. Mortgage was 160k, now 148k….looks like the plan is working! I appreciate your motivation to assist me with this!

That is excellent progress Diamond Dave. Thanks for checking in with an update. I hope you will check in again sometime.

Cheers

Great Post. I myself am one of those that bought my home at the exact amount the bank approved me. I live in Central California and bought my 1st home at $162,500 at age 26. My plan was to make biweekly and add a specific amount to the principal every month. I currently owe $138,500 after 3.5 years in my home.

My home according to Zillow is now worth $205,000

My plan is to sell my home, and purchase a Condo following the rule you gave (2x your annual salary 3x MAX) Looking a loan of around $100,000 and coming up with the down payment of $66,500 (Equity in my home)

A little sacrifice at first to downsize my living, but if i continue to make the $1200 monthly payments towards the $33,500 mortgage … I haven’t done the exact math but in 2-3 years i will be mortgage free at age 32.

Then i will continue to save the $1200 per month and in a few years have the 20% down payment for a second home.

Rent my Condo (say $900 per month) and use that income to add to the principal of my second mortgage. Then let the snowball effect begin with plenty of houses being paid off!

Little simplifying at first, but long run financial independence!

hi..I’m lost with number 2 of 3 regarding increasing after tax income. let’s say I make 100k, @2.9 % increase , that’s about 3k per year. how do u get the factor of 28? where do u get the additional 10k per year to pay additionally. the following year doubles. how does this income double?

Don,

Thanks for writing in. Rule #2 is to increase your after-tax income by 2.9% of your mortgage loan. So if you have a $350,000 loan (like in my example), you need to find a way to increase your after-tax income by ~$10,000 per year after-tax. So, going into year one if you are earning $100,000, you need to increase your after-tax income by $10,000 (which would mean you would have to increase your gross income by $13,333, assuming a 25% marginal tax rate, or about 13%). This would put your gross income around ~$113,333.

Then in year two, you would need to increase your income by another $10,000 after-tax (or another $13,333, still assuming a 25% marginal tax rate). This time the increase is only 11.7% and now your gross income is $126,666. Your goal is to increase your income every year of the seven-year period so by the end your gross income would be ~$193,331.

The 28 is how you calculate the cumulative increase in income over the 7 year period.

Cumulative after-tax income increases:

Year 1 = $10,000

Year 2 = $10,000 + $10,000

Year 3 = $10,000 + $10,000 + $10,000

Year 4 = $10,000 + $10,000 + $10,000 + $10,000

Year 5 = $10,000 + $10,000 + $10,000 + $10,000 + $10,000

Year 6 = $10,000 + $10,000 + $10,000 + $10,000 + $10,000 + $10,000

Year 7 = $10,000 + $10,000 + $10,000 + $10,000 + $10,000 + $10,000 + $10,000

You get the income increases by actively managing your career, picking up side hustles, and through investments.

Dom