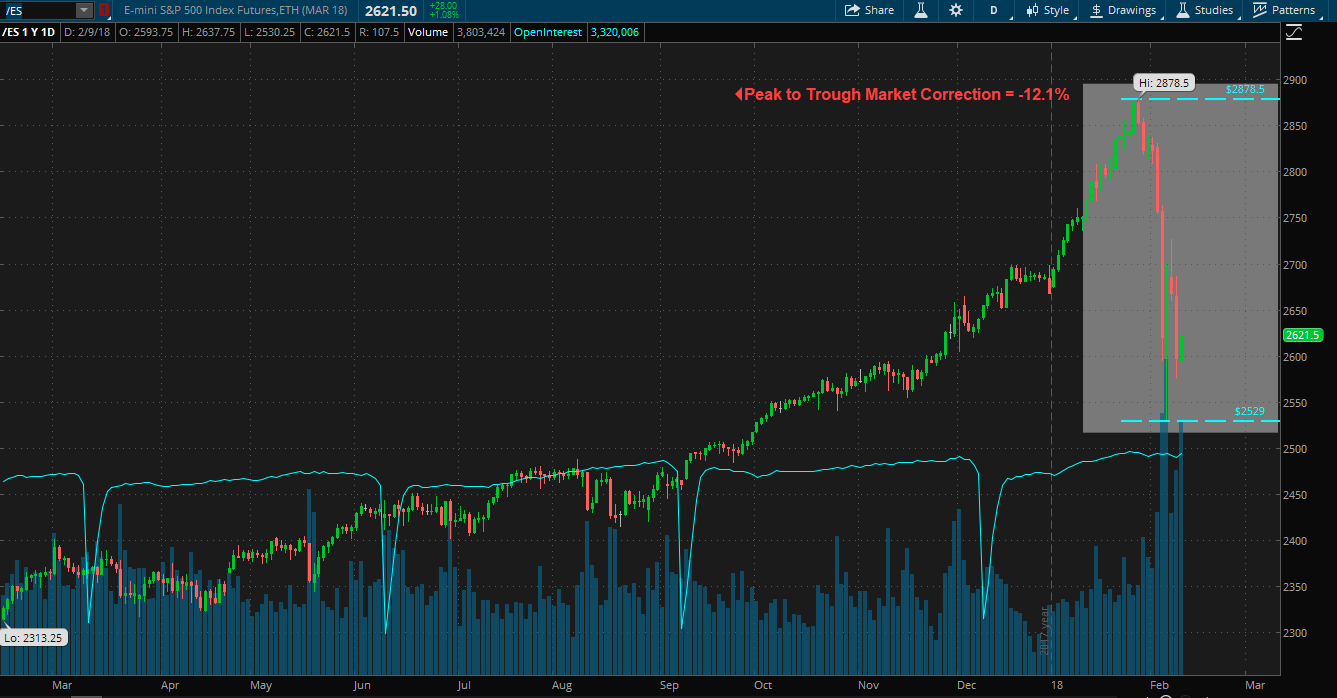

It’s been quite some time since we’ve witnessed the kind of volatility we saw over the past two weeks of trading (1/29/18 to 2/9/18). But I really don’t know how anyone can be surprised that we finally got this long overdue correction in the stock market. Corrections are natural and healthy. Perhaps it’s because we’ve had such a long run of upward motion this time that people acted as if they’ve forgotten this! If you look at the peak to trough correction of the date range referenced above, the S&P 500 experienced a -12.1% decline. These are the types of opportunities that justify building up an opportunity fund (what I like to refer to as “dry powder”).

Note: I will use “the market” and “the S&P 500” synonymously throughout this post.

(Oh, and did you see Bitcoin? It hit a high of $19,183 on 12/17/17 and a low of $6,998 on 2/5/18. This only reinforces the thoughts I shared in my Warren Buffet piece about what constitutes an investment.)

I have to admit that it is quite hilarious to me how fast human emotion can flip people. Two weeks ago, according to the chatter of the general internet, and the general population at large, the market was unbreakable – headed to infinity and beyond. Then we get a market move like this and it shows how as humans we are not innately equipped to deal with volatility. Now in the general chatter, we can hear how human emotion takes over, panic sets in, and selling begets more selling. A lot of people just got hurt in the short volatility trade that has worked for so many years (look at XIV, an ETF that shorted volatility: six years of gains wiped out in a single day and now the fund will have to shut down). I’d bet that many people didn’t truly understand the risk of investing in a fund like XIV, which was a function of ignorance, and more importantly…greed.

My post on selling options was rather timely when you consider the explosive move that we had in volatility during this correction (volatility moves inversely to the direction of the market). The market has experienced very little volatility (fear) for an unusually long period of time. It’s not healthy for a market to only go up day after day. The longer this happens the more dramatic a move to the downside can become. As is typical with volatility, everything seems safe, until we get a catalyst that causes fear to go parabolic. The peak to trough move in the fear index (VIX) was an incredible 487% (the VIX peaked at 50.3). This creates a lot of opportunities if you’re a seller of options.

Recent Dialogue From Another Post

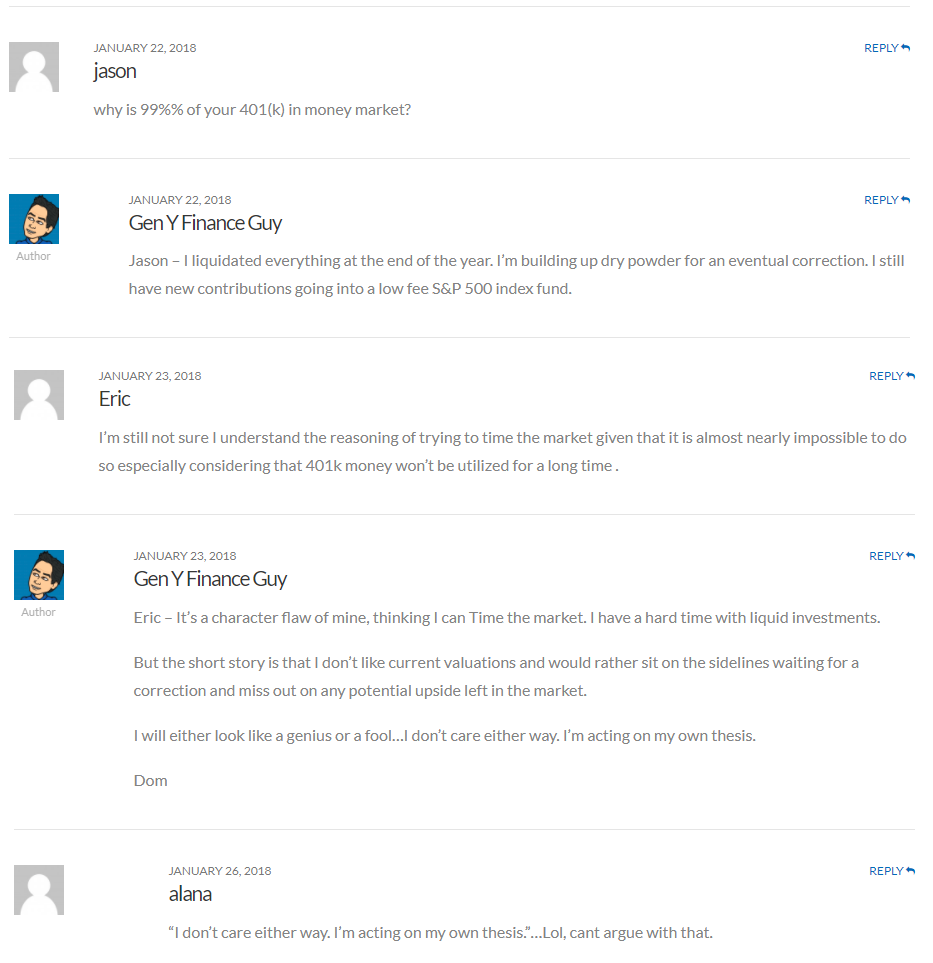

Below you can see a recent exchange I had with a few readers asking me why 99% of my 401K was sitting in cash. I should first point out that I am not suggesting anyone do what I do (or did); rather, I’m sharing my own thought process and actions. And although it may look like I made a brilliantly timed decision, I give all credit to luck, because we all know that timing the market is like catching a falling knife. Furthermore, if it’s confession time, I also have to point out that my stock portfolio has underperformed during this long-running bull market (yet, I have still managed to take my net worth from negative $300,000 in March of 2009 to almost $700,000 at the end of January 2018, so don’t feel too bad for me).

In the comment string above, I openly admit that I have a character flaw (although I only admitted to one of my many!). This particular character flaw is one I plan to finally fix in 2018. As a former trader, I have found it hard to fight the urge to treat my long term investment portfolio (401K) as a repository of funds for short term trades. The reality is that this is money that I will not be touching for decades and in this case “time in the market is more important than timing the market.”

The New Plan For My 401K

Going forward, I resolve to treat my 401K account as a “set it and forget it” account. New monthly contributions will take advantage of dollar cost averaging and the funds sitting in cash will be deployed to that end systematically. But I will also be opportunistic when it is warranted (but only with the current cash balance, not future contributions, as they are automatically set to invest as they are deposited). This is now one of those times it is warranted: of the $81,233 of cash available in my 401K, I placed a buy order for $21,233 on 2/9/2018 to take advantage of this recent market correction.

As outlined in this post, I have set my yearly 401K contributions to be front-loaded, thus maxing out by the end of March 2018. All future contributions are set to automatically invest in a low fee S&P 500 index fund. This still leaves $60,000 to be deployed as I see fit. I have set up a monthly recurring reminder to invest $5,000 on the second Wednesday of every month. I have given myself the discretion to be opportunistic to invest this money faster should the current correction make new lows (i.e., if the S&P 500 trades below 2,529).

Although my actions have not always seemed to support it, I truly believe your 401K should be passively invested in index funds, and not actively traded. Today I’m distinguishing my employer-chosen 401K, which has only a handful of funds to invest in, from my TD Ameritrade IRA account that allows me to invest in any stock or fund, and grants me the ability to sell options (one of my favorite things to do, if volatility is sufficient to make premiums worth selling).

There Is Still A Case To Be Made For “Dry Powder”

Further addressing the issue of how I may have seemingly mismanaged my 401K by not “setting and forgetting,” I still believe there is a case to be made for building up some “dry powder.” Because I resisted being fully invested and instead opted to pile up a war chest of cash (both in and out of my 401Ks), I’m in the fortunate position now of being able to capitalize on this decline. However, these funds are not only for taking advantage of declines in the stock market; they are there to seize other types of unexpected opportunities, as well, or even to take advantage of non-correlated investments like life settlements.

I have never felt any pressure to be fully invested (meaning that I typically have a lot of cash lying around). This philosophy has allowed us a lot of flexibility and optionality. A good example was the $105,000 investment we made into the company I work for. Or after finding PeerStreet, meeting with the team, doing due diligence, and then rolling over idle cash (about $70,000) from an old IRA to set up a self-directed IRA to invest in hard money loans.

Personally, I like to take my time evaluating investments, and then once my conviction is strong, deploy large amounts of capital. This works for me. You will have to find out what works for you. Either way, I encourage you to not be sucked into the FOMO (fear of missing out) when it comes to your idle cash. Do your due diligence, be prepared and remember that there is always opportunity in some asset class with a good risk to reward ratio.

– Gen Y Finance Guy

9 Responses

Liking your chosen re-entry strategy; big chunk upfront, remainder DCA. You are taking two paths, towards one destination.

Ben Stein and Phil DeMuth wrote a great book, https://www.amazon.com/Yes-You-Still-Retire-Comfortably/dp/1401903177 In it, they describe several solutions (nothing we all haven’t been exposed to before). But the ‘lightbulb moment’, for me, was this takeaway: If you can’t decide, or have multiple choices that look good, then you can choose several. In my investing past, I’ve also succumbed to my own character flaw(s). But this multi-pronged tactical approach to a Personal Finance strategy worked very well for me. I hope it does for you, too, GYFG!

Thanks, JayCeezy!

The idea of having a ‘play money’ account is good if it helps you to leave the passive funds alone. Does putting yourself in a position to have play money in the first place count as a character flaw? 😛

Keeping dry powder / emergency funds on the side is also a good idea. Although it can be painful thinking about the possible opportunity cost of missing out on investment gains if / when you have to deploy money at short notice it’s far better to be left thinking “it’s lucky I have my emergency fund” rather than having to scrabble around to pull money out of investments or, even worse, be forced to sell investments at a loss because you need cash asap.

HH

I wish I used some of my dry power a couple of weeks ago, but I missed out. I’ve transferred some over to my brokerage account and am waiting for another dip to happen. Not a matter of if, but when. I plan to buy in tranches. My 401k is doing its thing with DCA. But it’s been tough seeing the balance increase at the end of 2017 and kind of level off right now.