For the past six months, we had been thinking that our next big move would be to pick up a 2nd rental property. We were pretty set that we would do this sometime between September of 2015 and March of 2016. Living in Southern California, we were looking at investing in something with a price tag between $200K and $300K.

This price range would require a down payment between $40K and $60K (assuming 20% down). Then you have closing costs which I would estimate at another $3,000, which is a bit on the low end, but that’s because we have friends and family in just about every step of the real estate transaction.

In order to make this happen on our own, we were going to have to look for properties on the lower end of our range at around $200K. At one point we were considering an investment with friends that would allow us to expand our property choices. But after careful consideration, we decided that we would like to avoid doing deals with friends and family, due to the potential of ruining the relationship.

Then after months of consideration, I decided to look at other ways to get exposure to the real estate market. I looked at public REITs, mobile homes, and crowdfunding platforms like Realty Shares (which unfortunately require you to be an accredited investor). What I liked about these alternative options is that we didn’t have to leverage beyond our current level. Between the house and the investment condo, we are already carrying $509K in debt.

I think everyone has a different comfort level with leverage. It can be a great tool if you use it correctly, especially in your youth, when you are first getting going. The problem is that it can be a double-edged sword and most people take on too much debt. We saw firsthand during the financial crisis what happens when we over-leverage ourselves.

Personally, I’m probably a bit conservative in my use of debt. The amount of leverage I am comfortable carrying on our balance sheet is largely dependent on the interest rate. First, the only debt we carry is mortgage debt. As a rule of thumb, I like to keep the minimum service of all debt at around 25% of gross income.

Keeping that rule in mind, our minimum monthly payments related to servicing our two properties runs about $3,400/month (inclusive of principal, interest, HOA, and property taxes). Based on a monthly income of around $15K, this puts our debt service at approximately 23% of gross income.

By keeping this percentage low compared to gross income, it allows us the ability to max out retirement accounts, live a certain lifestyle, and still have plenty of excess income to make other investments. It also provides peace of mind if one of us lost our jobs as it would still be manageable on one income for an extended period of time.

Besides the desire to be completely debt free one day, this was one of the major reasons for such an aggressive pay down of the mortgage on our primary residence. Especially since an additional property would take us beyond the 25% comfort level. An investment property of around $200K after $40K down would have added an additional $1,500/month in debt service. This would have pushed us above 30% of gross income.

The goal with paying down the mortgage on our house was to get to 20% equity so that we could refinance one more time into another 5/5 ARM that would allow us to get a rate around 2.5% (our current rate is 3.675%). This would have dropped our payment by about $350/month. We just really weren’t sure if we wanted to add any more leverage to the balance sheet.

(Mr. CEO here – did you seriously just write all of those words to say, “So we’re struggling with whether another piece of real estate is the right move for the house?” Geez GYFG, you’d think you were the English major!)

Maybe you’re right Mr. CEO. But let’s be honest, it’s a big decision. So all of this back and forth with the wife has lead me to my Rich Uncles…

My Rich Uncles Provide Us a Solution by Allowing Us to Invest In Commercial Real Estate

(Mr. CEO again – so why are you writing about something that only you have access to? I don’t have any Rich Uncles and I have a feeling most of our readers don’t either.)

No, you’re not getting it. I don’t personally have any blood relatives that are Rich Uncles, but I now have some internet Rich Uncles.

Recently Vawt over at Early Retirement Ahead was contemplating a real estate investment and was looking for feedback and other ideas from his readers. In the comments, I suggested that he look at Realty Shares. I made an assumption that based on being a CFO that he would likely qualify as an accredited investor. In his response he suggested I check out Rich Uncles.

I am stoked that I took the time to check them out. They are a Commercial Real Estate Investment Trust (REIT). They are a public, non-listed REIT that requires governmental permitting and audited financial statements. (Mr. CEO here – so you’re saying they are not traded in the stock market but are still required to be audited, right?) That’s exactly right. The best thing about a non-listed REIT is that the value of your investment is determined by the value of the real estate itself.

Let’s Meet The Rich Uncles

Now you are probably wondering why they decided to name their company “Rich Uncles,” aren’t you? It really has to do with how they define a “Rich Uncle”:

- A Rich-Uncle is a person in your life that you can count on for prudent advice–financial or otherwise.

- A Rich-Uncle is someone who is available to lend a helping hand and provide guidance and information, all from a trusted person who has “been there.”

I don’t know about you but these are definitely the kind of people that I want looking out for me.

What is the investment strategy of this REIT?

First and foremost the REIT only invests in Commercial Real Estate and they are currently only set up to invest in California based properties. Only California residents are able to invest at this time. There are 8 major criteria that each property must pass in order to be considered for inclusion in the portfolio:

- Single-Tenant Freestanding

- Strong Tenants – large, recognizable, creditworthy companies (Chase, Del Taco, Chevron).

- Long Term Leases

- No Management Responsibilities

- No Leasing Costs

- Not Responsible for Property Taxes

- Not Responsible for Insurance

- Not Responsible for Maintenance and Utilities

Items 5-7 are possible because of “Triple Net” leases, where the tenant pays all property related expenses. The fund only purchases properties that they can put at least 60% cash down, keeping leverage to a manageable amount.

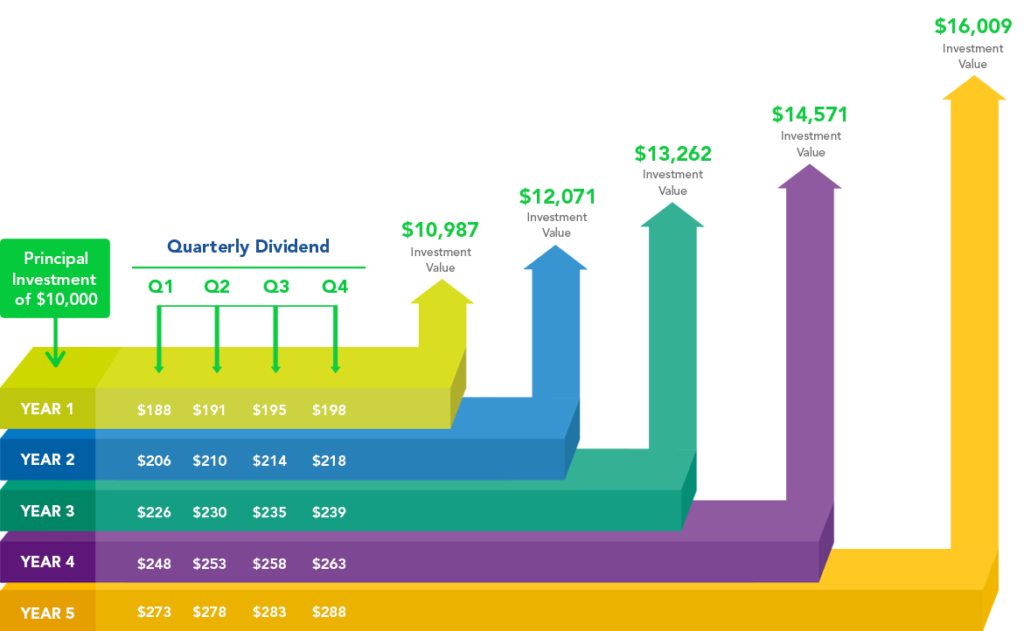

The fund has a planned exit date of 2020 in which they are planning for a liquidation event. Currently, when you invest in the fund you will earn 7.5% in dividends quarterly with an expected annual return of 12% over 5 years. When the fund is liquidated the priority of payment is as follows; return of your original investment, then reinvested dividends, then your share of property value appreciation.

Like I mentioned above, the exit plan is targeted at 2020, but there is a way to get your money out sooner if needed through the share repurchase program.

Below you will find an example of $10,000 invested. It assumes a 7.5% dividend and a 2% property appreciation as well as dividend reinvestment. I don’t know why, but I really dig the graphic they put together to represent this.

When I spoke with one of the account executives over at Rich Uncles he informed me that they have paid over 7% for 9 consecutive quarters now. However, it is good to keep in mind that the dividends are determined by the board of directors and depend on the cash availability and project cash requirements. They are required to distribute at least 90% of taxable earnings in order to maintain qualified to operate as a REIT.

What am I doing?

Well if you haven’t already guessed by the prelude, I am making a pivot. Instead of investing in a 2nd residential property and taking on more leverage, we are instead going to invest in this public REIT. This will give us exposure to the commercial real estate market that we would not be able to get on our own and will provide a really nice 7.5% dividend.

I have only made an initial investment of $500 to test the waters and get familiar with the platform, which is 100% online. So far the experience has been great. The platform is really easy and intuitive and the follow-up call from Harry, one of the account executives, was great! Best of all Rich Uncles is headquartered in Newport Beach and they have invited me to come down to the office for an interview that I then will get to share with all of you on this blog (so think of some questions).

Beginning in May we will start investing $1,000/month into this fund (as this goes live, we now have $1,500 invested). We may do some lump sum investments in July and January, which happens to be bonus time for me. Although we were willing to put $40K down on a $200K property, it is likely that we will only allocate a maximum of $20K to this REIT.

I look forward to sharing my experience with you guys. Oh, and if you invest with them, don’t forget to tell them that Gen Y Finance Guy sent you 🙂

– Gen Y Finance Guy

p.s. When you sign up you have the opportunity to earn 5 bonus shares by giving a testimonial. (I just received mine)

p.s.s You can get 5 bonus shares for each person you refer that results in a shareholder (with a minimum $500 investment)

p.s.s.s If your referral invests $5,000 or more than you get 10 bonus shares.

p.s.s.s.s Here is a link to a recent article from the OC Business Journal.

40 Responses

Interesting how they are only allowing California based investors at this time. I usually play devil’s advocate on these types of things, so I have a few questions:

1) What convinced you to invest with them? Past performance? Your discussion with an account executive? The fact that their audited?

2) Are the dividends taxed as ordinary income or can they get qualified dividend treatment?

3) You say they have paid over 7% for 9 consecutive quarters, have they only been around for over 2 years?

Thanks!

FF – I like the way you think!

They are currently only allowed to let California based residents into the fund based on the way they are currently set up. However, they are working on launching another fund that would not only allow people from out of California in as investors, but that would also allow the fund to venture out of state for other investment opportunities.

Your Questions:

1) I was already looking to expand my exposure to real estate. The more I thought about getting an additional investment property and leveraging up, the less I really liked the idea. The fact that they are located in Newport Beach is really ideal, especially since I have been invited to come and check out the office and interview the president of the fund. I do like the fact that they are audited (always nice to have checks and balances). More importantly I like that they our pretty conservative in their approach only borrowing up to 40% of the property value. I think this will really keep them out of trouble by not over leveraging themselves.

2) The dividends will generally be taxed at ordinary income unless you want to hold them in a self directed retirement account. However, a portion of the gains will be deferred because of depreciation expense. This defers a portion of your tax until your investment is sold or liquidated, and will be taxed at capital gains rates.

3) Yes they are a new fund that has only been around for a couple of years. They do have a liquidation/exit event scheduled in 2020.

Cheers!

I have been evaluating this move for quite some time now! I have yet to pull the trigger, but I like that $500 is the minimum.

One thing you didn’t mention is that they purchase with 60% equity in each property. That made me feel like they are not overreaching for returns. The thing that concerned me the most is how much of an admin fee it takes to run it.

Vawt – The $500 minimum is certainly a low barrier of entry. I also appreciate that it does not require the “accredited investor” designation.

I totally forgot to mention the 60% equity in each property. Hopefully people will read through the comments and pick that up 🙂

Regarding the admin fee…what have you seen with other REITS? I thought it was pretty good that 97% of gross proceeds were going to fund investments. I was also under the impression that the 3% they use to manage the fund was less then other REITS, because they are growing it all organically and not paying broker commissions to spread the word and bring in new investors. And now advertising, just word of mouth.

Let me know.

Cheers!

GYFG,

I like that you are expanding into new opportunities. I have been trying to do the same thing recently dabbling in some option trades. I have not yet ventured into the real estate game other than owning some REITs. I have several friends that have rental properties and one in particular who owns a VAPE shop and has a condo that he rents out. There are a lot of “hustlers” out there working hard and it is very inspiring to say the least.

My competitive nature compels me to join the party and grow my “mini empire”, but my conservative nature tells me to keep focused on buying income producing stocks and avoid using leverage

It will be fun to watch your current and future progressions!

MDP

Thanks MDP!

We already have a rental condo and the idea of picking up an additional property was good until we started thinking about increasing the leverage on our personal balance sheet. So this seems like a really good alternative.

Thanks for the support as always.

Cheers!

Hey GYFG,

Interesting article and thoughts that you have here. I am curious to find out how this will evolve for you. I like the idea that you stay conservative on your leverage. I am a bit like you. My goal is to be debt free in 10 years (deliberate choice, due to tax advantage I have). I will lower my outstanding this month with about 12pct, to pay less each month.

3 weeks ago I met with a similar Belgian fund. They invest in student housing, they focus on prime locations and renters and they seek to increase their debt a little more (towards 60 pct I thought). I hope to meet them end of May when they have an investor day. Their closing date is around 2020 as well.

Reasons form do to so

1- I sold last year an investment property and used the cash to reduce my mortgage (I have a need to be debt free somewhere deep inside me), remodelled the garden and put the rest onto the stock market. Why sell? having 2 kids, a wife, a garden, a job I love and some hobbies leaves little time for redoing the rental after the last tenant left. I do want however more real estate exposure

2- Owning a rental is not for me now (see point 1)

3- It should not be more than 10pct of my portfolio (not counting my main house)

For now the entry ticket is too high for me, but they might do a next round later this year with a ticket size around 10K. Might be doable.

Cheers

Hi Amber Tree,

So we are officially in Belgium 🙂

You have to do whats right for you.

Thanks for stopping by.

Cheers!

We’re looking real hard at rental properties in Houston, but the market has gone nuts the past 2-3 years. It’s really hard to find anything affordable that cash flows.

That is what I have heard. Will this be your first investment property? What are prices like for what your looking for?

Just to warn you -here’s what the MMM forum has to say about Rich Uncles.

http://forum.mrmoneymustache.com/welcome-to-the-forum/rich-uncles/

Personally I would be very wary of investing with something like this especially in the volume you are talking about.

Thanks for looking out Michael. It’s funny because Vawt is the one that started that thread and he is also the guy who put the Rich Uncles on my radar.

I think everyone has to evaluate investments for themselves and determine if the risk AND fees fit their objectives. In this case I am comfortable with both.

Cheers!

The concept itself sounds great, one of the red flags for me while reading was the 2020 liquidation, my first thought would be doing a fire sale of sorts during 2020 wouldn’t that bring the property value down and possibly not get your investment money back? Also does it work in a Tranche or Waterfall payout? Since they are doing all the leg work what fees are they getting out of this?

Just a couple questions, maybe you answered them already I haven’t had a touch of coffee yet;)

Hey man,

Good Questions!

First when I said a 2020 liquidation, that is just a target date for some sort of liquidity event. That could mean selling the properties, taking the fund public, sell it to another fund. I have worked in a lot of private equity, and trust me these guys are going to be very opportunistic about their sale. They want to make investors as much money as they can.

Here is the quote strait from the prospectus: we intend to create a liquidity event for our Share owners, which liquidity event may include the sale of all of our Properties and the dissolution and winding up of our REIT, the listing of our Shares on a national exchange, or the merger of our REIT with another entity that is listed on a national exchange (the “Liquidity Event”).

There is a waterfall of how the funds get paid out after the liquidation event. It looks like this:

1 – Return of your original investment

2 – Then Reinvested dividends

3 – Then Your share of property value appreciation

The fund gets 15% of net sale proceeds after investor money is returned (including original investment and reinvested dividends).

Hope that help!

Cheers,

GYFG

I lost my first $5K in commercial real estate at the ripe old age of 13 thanks to my Rich Grandpa), but it was worth the education. In general, he’s made a killing off of commercial real estate, but this one turned out to be pretty bad (he lost about $150K). I’ve learned a ton about commercial real estate, zoning laws, tenant and lease laws, all as a result of this particular dropping in value by almost 90% since we bought it.

This looks like a great REIT too. I don’t know that I will pull the trigger, but I love their strategy. Good find GYFG!

Hey Hannah,

I think we can all share a story of a bad investment.

Glad you found it interesting.

Cheers!

Ha that’s so funny their name is Rich-Uncles. I never would have guessed that. Sounds like quite an intriguing investment opportunity. That’s cool you get to interview them in person too. Keep us posted on how it works out!

It certainly made for an interesting blog title 🙂

I am excited to get down there to interview the team. I will definitely keep everyone updated on how it works out.

Cheers!

Hey just stumbled across this post as I was looking into reviews for Rich Uncle. How has your experience been so far with them? Have they returned 7.5% dividends monthly? I’d be looking to put $500/month or so into the fund. Thanks!

Hey Bob – The dividends are not paid monthly, they are paid quarterly. Also just to clarify the 7.5% is the annual yield. That said, the fund has paid quarterly at the rate of the annual 7.5% yield. I have been invested in the California fund for well over a year now. However, that fund is now closed as they just opened up a national fund, which I am not sure what the dividend rate is on that one, you will have to look into it.

Cheers

Are you still investing with RichUncles? Have you invested in the newer fund? I’m intrigued.

TJ – I am still invested with Rich Uncles, but have not yet invested with their new national fund. I do however plan to put new money to work with them in 2017.

Don’t you qualify as an accredited investor based on income? >300K

GG – Yes we do qualify as accredited investors now, but did not at the time of writing this post back in May of 2015.

Cheers