The year is officially 33% complete. I can honestly say this is the post I get most excited about writing each and every month. (Mr. CEO here – One thing I want to say right now before we get too far, is that THIS POST….THIS VERY POST is our 50th post. WOW!!! Can you believe it!? Time is absolutely flying by)

WOW! That is amazing that we are already on post number 50!!! (I love those little !!!!!)

These reports are a way for me to track my progress and stay accountable to my goals. But it’s also one of the many ways I try to humanize finance for all of you reading this blog. By the way, in case you missed it, our mission statement is:

To Humanize Finance, Build Wealth, and Reach Financial Freedom.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (because not that many finance blogs do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities. Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

As always, you can find all my previous reports on the Financial Stats page (as well as annual trends and a few other financial metrics not found on this report). In these monthly reports the plan is to give you a month over month update on Gross Income, Assets, Liabilities, Net Worth, Expenses, Contributions, and progress on the mortgage pay down goal.

Can I ask you for one small favor before you continue reading? Could you use one of the icons to the right of this post to share it on your favorite social media channel to help spread the word?

Thank you, thank you, thank you soooooo much!!!!

Shall we begin?

Summary of April 2015

What went down in April

During the month of April we actually had a 3% increase in gross income. The increase is really coming as a result of two things: a $250 referral fee for helping a recruiter place my friend into a new job, a $226 refund for out of pocket medical expenses that I contested and got refunded, and the remaining $35 was from miscellaneous sources. You may recall from the January report that I paid $450 out of pocket when my wife got her wisdom teeth removed. For some crazy reason they said everything but the anesthesia was covered by insurance.

That made absolutely no sense to me. So I have been contesting it and going round and round with the insurance company and the dental office and they finally issued a refund for half of that expense. I was hoping to get it all back but half is better than nothing.

April’s income doesn’t include any income that has been produced by the blog just yet, since I actually haven’t received payment yet. Since monetizing in March, the blog has produced about $300 in revenue. But don’t worry, I will be detailing all that and more in a separate blog update, where transparency will still be the name of the game. I am sure you guys have seen a lot changing and I want to share the results with you all – especially those that are currently blogging or those thinking about blogging. You can learn from my successes and my failures. Let me be your blogging and financial guinea pig.

March Income = $15,509

- Previous Month: $15,057

- Difference: +$452

Going forward, gross income should come in around $15,000 a month from April through June. In July I anticipate a nice spike in income due to semi-annual bonus payments and a 3-period pay cycle (I get paid on a bi-weekly schedule).

Now where did all that money go?

The last four months have been very high with regard to expenses due to some planned and some unplanned expenses. I THINK I can finally say that our “one-time expenses” are behind us. If you want to see what I mean you can go look at the prior three reports here: January, February, and March.

Home Mortgage & HOA $3,099 The normal payment is $2,215/month for the mortgage and $84 for the HOA. However, as a part of our 7-year mortgage pay off plan, we started adding an extra $800/month towards principle.

- No change vs. previous month.

Condo Mortgage & HOA $2,263 This is the payment on our rental condo and includes the mortgage of $888 and HOA of $250. We currently rent this place out for $1,350/month, as seen in the summary table above. In April we had to pay property taxes of $1,125, since we don’t have an impound account set up to collect this on a monthly basis. The property was recently valued higher and thus increased our bi-annual payments almost 38%.

- Previous Month: $1,138

- Difference: -$1,125

Timeshare $190 My grandparents left me their timeshare before they passed away. This is a quarterly installment of the annual maintenance expense. I typically just rent it out for enough to cover the annual maintenance fees. I haven’t placed it with the property management company yet, but this reminds me that I should probably get on that soon. It’s not likely that we will use it this year. I really only hold onto it because I can cover the cost by renting it out and it’s in Vegas on the main strip between the Bellagio and the Cosmopolitan. My bet is at some point one of those hotels is going to offer a buy out to tear the thing down.

- Previous Month: $0

- Difference: -$190

Home Improvement $262 We don’t have any other projects planned this year (February was the big one with the cabinets in the garage and my wife painting the interior of the house), which will be good for our savings plans. However, there will always be small projects that hit now and then. My wife is always working on little projects around the house and in the backyard. I also had to fix a sprinkler valve.

- Previous Month: $245

- Difference: -$17

Food & Dining $1,085 This amount includes money we spend at the grocery store, dining out, drinking out, and dog food/treats (our two dogs eat well). In the month of March we spent $531 on groceries, $135 dog food, and $419 on eating out at restaurants. This is an expense that tends to get a little out of control for us. Last year we spent $14,000 on eating out or almost $1,200/month on average. The goal for 2015 is to keep this combined expense at or below $1,200/month; $500 for eating out and $700 for groceries.

- Previous month: $1,322

- Difference: -$237

Shopping & Other $401 We got my dog groomed for $75, bought some sleeping pads for our camping trip ($75), and then there was some shopping at the following places: Victoria’s Secret ($30), Carter’s, Delias ($7), Home Goods ($11), Target ($30), iTunes ($60), Michaels ($45), and other ($68). (Mr. CEO again – I feel like you need to remind Mrs. GYFG that it’s perfectly acceptable to go over the budget to spend at Victoria’s Secret).

- Previous month: $499

- Difference: +$164

Travel & Hotel $0

- Previous month: $0

- Difference: -$0

Auto and Transport $1,186 This includes fuel, car insurance on two cars, and toll roads. I had to get my transmission serviced for the 60,000 mile maintenance. We also had to pay registration on both of our cars this month. Oh, and I took an UBER trip that cost me $56. Next month I have a few more services that I need to get done on both cars that will likely keep this expense a bit elevated than normal, but you need to keep up with the routine maintenance so you don’t end up spending more than you need to by letting things break.

- Previous month: $459

- Difference: -$727

Personal Development $2,350 You may remember that last month I mentioned that my wife had started some business coaching that was going to be a total cost of $4,500 for 6 months’ worth of coaching. We are paying it in two installments, with the first installment paid in March and the final installment in April. This is an investment in my wife and her career. We are more than happy to make investments in ourselves. It saved us $300 to make two payments, instead of making monthly payments of $800/month.

I also registered for a conference to help me take my blog and business to the next level. It was $100, but what is cool is that after the 4 days you get your money back as long as you stayed for the whole thing. The event is called Life on Fire and registration is still open if you want to join me in San Diego. It looks like they lowered the deposit to $47.

- Previous month: $2,250

- Difference: +$100

Bills & Utilities $412 This includes our monthly utilities like gas, electric, water, internet, and cell phones. Not much to say here.

- Previous month: $481

- Difference: -$69

Health & Fitness $164 This includes a monthly massage subscription, monthly dues to remain an active member of Team Beachbody to ensure my discounts on supplements like Shakeology and Results and Recovery Formula. And a new order of Shakeology that should be her any day. (GYFG hits the workouts hard and has been an inspiration to me. I try to get something in every day no matter how small just to keep my body on pace with my mind).

- Previous month: $167

- Difference: -$3

Business Services $65 The new theme I purchased and installed this month. It’s actually the first theme I have paid for since starting the blog 7 months ago.

- Previous month: 0

- Difference: +$65

Total Expenses $11,477

- Previous month: $9,615

- Difference: -$1,862

Last month I was forecasting that expenses would come in around $13,000 for the month. However, this included income taxes that I would need to pay for 2014 in the amount of $2,200. In order to keep things consistent I have actually included this payment in the “Tax & Benefits” section below. When you factor this in, we actually spent about $800 more than I forecasted. This is explained by the $450 we paid for car registration, $130 for transmission service, and the $190 for the timeshare.

With that said, May will be the month where we really reign in the spending and crank up the savings and investing. After saying this for the past few months, I am really excited for May. We really get to put some jet fuel behind increases in Net Worth going forward. And soon you will be hearing about some new after-tax investments I am getting into.

What were Investments and Contributions?

I currently work for an employer that offers a 401K with matching. For years now, I have taken advantage of maxing out my 410K for both the tax benefit and company match. This works out to be about 16% of my income off the top before I ever even see my paycheck.

My wife happens to work in a family business and unfortunately they are not able to offer a retirement plan, let alone matching. So starting in 2014 we opened up an IRA for her that we plan to max out with $5,500 every year. Starting with February, we have set up an automatic contribution of $500/month.

I also have an IRA due to a 401K rollover from a previous employer. I personally wish I could have all my retirement money in my TD Ameritrade IRA account because of the unlimited investment choices and the ability to invest in many different asset classes, including options.

Now lets take a look at what activity went down this month:

- Contributed $500 to the wife’s IRA for the 2015 tax year.

- Previous month: $500

- Difference: $0

- Contributed $1,169 Into my 401K. The normal contribution will average 16% for the year, but I do play around with the percentage occasionally.

- Previous month: $1,169

- Difference: $0

- Prosper Lending $500 First deposit of new money here since 2010. This is included in the “Liquid Cash” section of the summary above. I will eventually break it out as it gets bigger.

- Previous month: $0

- Difference: +$500

- Increase in Savings $0 This includes checking, savings, and CD’s. This is where I want to see the increase of $2K to $3K a month I mentioned above.

- Previous month: $300

- Difference: -$300

Total Investments & Contributions $2,169

- Previous month: $1,969

- Difference: +$200

Summing it all up against the Gross Income

Benjamin Franklin famously said, “that everything has a place and that everything should be put in its place.” With that, let’s summarize where the total gross income for the month of April went.

Gross Income $15,509

(Less) Expenses* $11,477

(Less) Investments & Contributions $2,669

Sub-Total $1,863

(less) Taxes & Benefits $4,377

(Plus) Draw-down from Savings $2,514 (This was the amount that our cash-stash decreased since we spent and contributed more than we brought in this month)

Total = ZERO

Everything is accounted for (phew!).

Net Worth and Mortgage Pay Down Update

My ultimate goal is to build up a Net Worth of $10M returning 6% a year or $50,000/month in gross income. Don’t freak out, this is only about $5.5M in today’s dollars when you take into account a 3% inflation rate.

I am not anywhere close to a 7-figure net worth yet (or what some refer to as the double comma club). However, it is growing at a very respectable rate. If you want to see how I plan to get there you can read all about it here.

Arpil Net Worth $204,209 (with four months down in 2015, this puts us up $22,845 or 12.6% vs. 2014 so far and we still have 8 months to go)

- Previous month: $201,054

- Difference: +$3,156

With a year to date net worth gain of $22,845, that puts us right on target. On Monday I published a post where I outline our goal to increase our net worth by $69,000 in 2015. We are officially 33% through the year and have reached 33% of our goal.

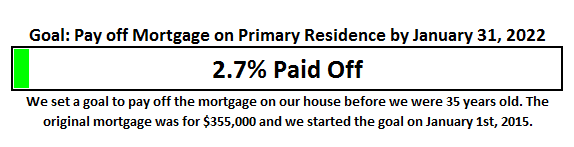

One of the other huge goals that I announced on the blog recently, was the strategy to pay off our mortgage in 7 years. When you break it down and follow the 3 simple rules, it’s not as hard as it sounds. We bought our house in February of 2014 and then refinanced it into a 5/5 ARM in September of 2014 to remove PMI and free up cash-flow to put towards the principal and keep us on track to pay the mortgage off at an accelerated pace.

The progress chart above shows how much of our goal we have completed. Last month we were at 2.3%, which means we picked up another 40 basis points in April. At this rate we will be 5.9% complete with this goal at the end of 2015 (assuming no extra lump sum payments).

The End

April was nothing to write home about. Things pretty much came in where I thought they would with the exception of the $800 of additional expenses. May is the magical month. We should see savings increase and net worth should be increasing by about $6,000/month or more (starting in May that is).

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years of slaving away for the man before you have the option to retire. I personally think that 20-25 years is really all you need, and for the folks that are more aggressive (i.e. extremely frugal, not us) or very high earners you can probably reach financial independence in 10 years or less.

I am looking forward to chatting with you all in the comments below. How was your month? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

(I must say GYFG, this was another great post and enlightening view “behind the curtain.” I really admire you for setting goals and holding yourself accountable in a public way. As I saw this month, it’s not perfect when it comes to managing personal finances. But it’s great to see that others are in similar situations – accidents happen, windfalls come that weren’t expected, etc. I look forward to seeing the evolution over the next couple of months).

Cheers!

– Gen Y Finance Guy

PS: Here are my favorite ways to track this stuff:

- The “Financial Stats” spreadsheet – a simple Excel template I created to provide the tables and charts you see in this post as well as on the Financial Stats Page. If you would like a copy of this spreadsheet, sign up for my email list below or at the top of the page and I will send you a copy.

- Mint (free) – Mint is great for setting up budgets and automating the tracking of your actual spending habits vs. the budgets you set.

- Personal Capital (free) – This is like Mint, but is geared towards investments and net worth tracking.

24 Responses

Hey GYFG,

Just wanted to post from the silent majority of readers that aren’t commenters. I have thoroughly enjoyed your blog since stumbling across it over at Financial Samurai. I really do appreciate and I am sure others do as well, your willingness to open your books and share with us your true to live financial life. I am one of those personal finance guys who are so concentrated on the “spending” side of my budget but I definitely appreciate reading your investment strategies and income growth blogs.

Keep up the good work.

Thanks man!

It is always nice to get feedback from the readers. I am glad that you are enjoying the blog. Stoked that I can present some posts that focus on the other side of the equation 😉

I appreciate the comment.

Cheers!

Sometimes a non-descript month is not all that bad.

I am impressed that you have been successful in monetizing so quickly. I look forward to that post.

You are so right Vawt. The last few months have not been block buster, yet I have still managed to grow net worth by a respectable amount.

Like you I am very surprised at how fast I was able to monetize. I plan to write a post sometime in June or July to update everyone on the blogging side of things as far as what’s working and progress being made. So keep your eye out for that post, because like everything else I will be very transparent.

Cheers!

Are all of these figures for you and the Mrs. collectively? Regardless, $15,000 per month is BIG! Congrats!

Professor,

Yes the income number is inclusive of my wife’s pay.

Cheers!

I think those dogs eat and get groomed more than I do! 😉 Nice month. I’m looking forward to May which will bring in three paychecks compared to the normal two. Take care.

Hey FF,

I am starting to thing that those dogs get better treatment than I do. What a life it is to be a dog 🙂

Sounds like May will be a nice one for you.

Cheers!

Congratulations on becoming a peer to peer lender!

Thanks Simon!

Don’t know if I shared this with you already or not. But after logging in to make my first transfer in years. I went back to the history and saw that the last activity I had in the account was back in 2010.

Still less than the $5,000 that you recommended.

Cheers!

GenYFinanceGuy, keep it up! You are building an empire just like the Romans did, one brick at a time.

Am very interested to learn of your experience at the “Life On Fire” seminar. Maybe you will find the experience worth posting about. There is an excellent book about the Self-Help And Motivation industry by Steve Salerno, which discusses how the most likely clients/customers of books, podcasts, seminars, coaching, etc. are people that have already bought before. I’ll leave it at that for now, but I’m always interested in facts, no matter the p.o.v. of the messenger. Anyway, the persons putting on this seminar have also made some inroads with ‘motivational speakers’ and getting them to sign up for a “package” that involves the platforms of Facebook, Twitter, LinkedIn, podcasts, blogs, and other ‘found media’ with low barriers to entry. So your experience is of interest.

Am also curious about your experience with options and covered-calls. The concepts are clear, but learning of real, live success with measurable results from those who practice the concepts is hard to come by. In updating my data, a metric I find helpful is to calculate the annualized return for both period and YTD. That way I can see how I am doing against my benchmarks (Wilshire 5000 and 10-yr Treasury). Keep up the momentum, thanks for sharing!

Hey JayCeezy,

Always nice to see you hanging around in the comments. I am pretty excited for the “Life On Fire” event, and will most definitely be writing a post about my experience. As you know I am a pretty huge fan of Jim Rohn and one of his quotes that comes to mind and I totally agree with is:

“If you want to get more, you have to BECOME MORE!”

I think events, books, podcasts, etc., are the paths to becoming more.

Feel free to shoot me any questions you have about options and covered-calls. I will slowly be leaking stuff out over time. I have so much I want to share, but I don’t want to overwhelm anyone including myself. So been trying to find a systematic way to slowly leak it out and let it soak in.

Thanks for the support as always.

Cheers!

Gen Y Finance Guy,

Regarding the goal of paying off your house in 7 years; Have you considered an alternative strategy?

Such as saving that money and using it to buy investment real estate which could potentially provide the income stream to pay your mortgage payment. This may not be practical in your area, but it certainly is in mine. Ultimately, while paying off a home is a noble achievement, it just seems that the money used to do this would be better served on other investments that create a higher rate of return then interest rates on personal mortgage debt.

Hi Midwestern Landlord,

I have certainly thought about alternative strategies. Actually it’s something I think about a lot. We do own an investment property and were contemplating a 2nd one until we recently changed our minds and instead are investing in a Commercial REIT that is currently only open to California residents.

We are not opposed to leverage, but at this time we don’t really want to leverage up any more than we currently are.

We also look at paying our mortgage off as a substitute for a bond allocation. If our equity in our primariy residence started to grow grater than 50% of our total net worth than it may be time to reconsider.

I have also contemplated holding onto the cash until we could pay it off in a lump sum. Because of course there is always things that could happen that would make having so much cash tied up in the house a huge inconvenience.

But based on some longer term goals, this is the best option for us at the moment.

Really good question.

Cheers!

Just thought I’d throw it out there. Ultimately you have to go with what you are most comfortable with. I agree that a risk of paying off a mortgage early is having substantial sums of capital tied up in the property with a continued mortgage payment still in place until it is paid off. If the funds are more liquid in nature, it allows for greater flexibility in a pinch.

Totally appreciate the question.

The other thing to realize is that this whole plan is based on what I call the “Pay More Tomorrow” principle.

Not sure if you have read my original post or not (it’s linked in the post). But in it I detail that this plan assumes an increase in income of $10,000/year and those are the funds that go towards paying down the mortgage early.

So the whole strategy is highly dependent on income growth.

It’s also not in lieu of making other investments. We are still maxing out our retirement plans. We have started two after tax investments (a REIT & P2P Lending) that we will be beefing up over the next 8 months.

So if you look at as a % of our total net worth increase, it only represents about 14%, based on contributing an additional $800/month in 2015.

So it’s really only a small piece of a much bigger plan.

Cheers!

It’s amazing how fast it comes and goes. Sometimes, just when you think you have it made, some other bill comes along…

Hey NNL,

That’s so true. There will always be surprises. However, I do anticipate that the BIG surprises our out of the way.

May will be very telling.

Cheers!

Some great detail here GYFG, and awesome to see you’re on track for your $69k increase in net worth. There’s definitely some awesome energy and enthusiasm pouring out of your posts, hope you can keep this momentum up on your journey towards $10 mil!

Cheers,

Jason

Thanks for the encouragement Jason!

It has been really fun so far. I didn’t share it in the post, but since putting together that $69,000 goal I have done a little calculating based on my forecast of May through December, and it’s possible that the $69,000 could be $85,000.

But no need to put the horse before the carriage.

I will make you a deal. If you promise to continue reading, I will promise to keep the energy and momentum up 🙂

Cheers!

I just love how you can make monthly financial reports so fun to read. I’m looking forward to reading next month’s update! I wish I could be transparent about my financial progress on my blog as well, but a large chunk of my readers are friends/acquaintances, so I’m still contemplating on whether or not that would make things awkward. I’ll be sure to share the link with you I ever decide to go ahead with it – I would need all the support and accountability I could get haha

Hi Anum,

I am so glad that you enjoy reading them. Hopefully I can make them even more fun and interesting to read over time.

It is definitely a very big decision to share all the juicy details of you financial situation. Since I write under GYFG, it makes it a much easier decision to share all my information. Only a few of the closest people in my circle of family and friends know that I even have a blog.

It’s also a big reason I chose not to disclose my full name or tell anyone what I was doing online. I wanted the freedom to talk about things I thought should be talked about. Things that people want to talk about, but feel uncomfortable to do so.

You could always choose to share one aspect of your financial life to test the waters…

Cheers!