Wow! Where does the time go? I can’t believe that it’s already time for my 2nd detailed financial report. I can honestly say this is the post I get most excited about writing each and every month.

These reports are a way for me to track my progress and stay accountable to my goals. But it’s also one of the many ways I try to humanize finance for all of you reading this blog. By the way, did you notice we officially have a mission statement?

To Humanize Finance, Build Wealth, and Reach Financial Freedom.

It has been something that has been on my mind for a while. It has finally been articulated into words and can be seen by all on the home page as well as on the about page.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (because not that many finance blogs do this). I publish all of my financial details not to brag, but instead to show you what is working, as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities. Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

As always, you can find all my previous reports on the Financial Stats page (as well as annual trends). In these monthly reports the plan is to give you a month over month update on Gross Income, Assets, Liabilities, Net Worth, Expenses, Contributions, and progress on the mortgage pay down goal.

Shall we begin?

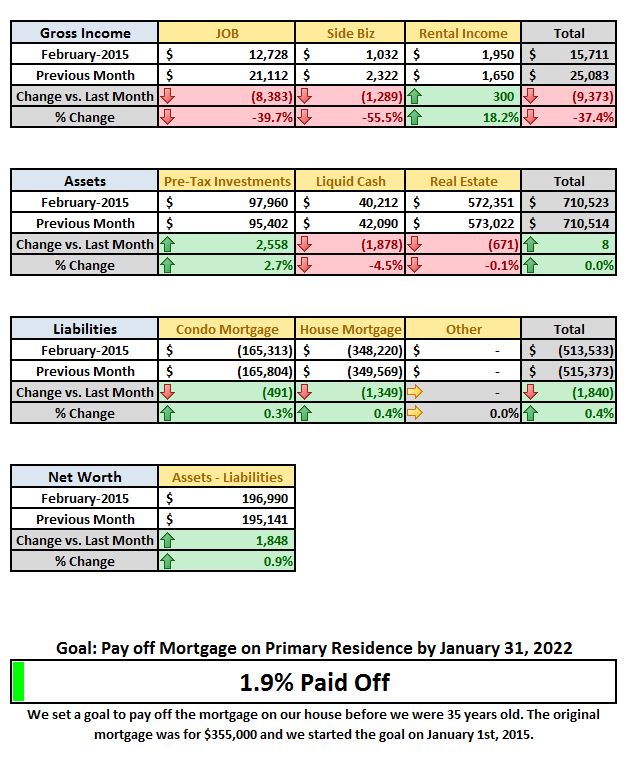

Summary of February 2015

Note: Above chart was updated on 4/1/15 due to a formula error on the month over month change. Thanks goes out to Wisdom Junkie for pointing it out to me in order to fix it. Need you guys to keep my honest 🙂

What went down in February

Last month (January that is) was a record month on the income side of the equation. But we knew it was a one-time event and not something to count on going forward. There were a few big items that drove gross income to astronomical levels in January.

So let’s take a walk down memory lane to point out the anomalies that occurred in January:

- Due to my bi-weekly pay schedule January happens to be one of the two months of the year that has 3 pay periods. This accounted for an extra $3,500 in income for the month. This will not happen again until July (I think???).

- January also happens to be raise and bonus time. And during my review, I found out that I got a raise of $5,000/year and an additional $5,000 in bonus. This accounts for $5,600 of the increase vs. last month.

- And the last piece was $2,150 in business income. This was income for a client that I was managing online marketing and analytics for. I invoice them quarterly, so this was the 4th quarter payment for 2014. Unfortunately, this contract expired in January and I will receive my last payment from this client in February (but it was only a third of the payment in January). You can look back at my previous report if you want to read why I decided to close this business down.

Moving on to February now…

February Income = $15,711

- Previous Month: $25,083

- Difference: -$9,373

Wait just a minute…when the anomalies are added up it suggests your income month over month should had dropped by $11,250, but it only dropped by $9,373!

What gives???

Ok, let me explain.

There were some pickups that partially offset the drop in income. Here is what the pickups were that offset the drop in income:

- We collected an extra $300 in rent for the room we rent out in our house. Our roommate had been gone for almost two months, so I gave him 50% off the rent for both December and January. Mostly because I didn’t feel right charging him the full amount when he wasn’t actually here. But now we are back to the regular $600/month rate.

- We collected $300 on a personal loan that we gave to a friend (who also happens to be the roommate mentioned above).

- I received my last commission check of $720 related to my business that shut down as of January-2015.

- And finally my wife brought in an extra $557 from her notary business.

Although it was hard to give up the extra money from the side business, I honestly think that with enough time, effort, consistency, and content, this blog will far out-earn this side business. In 5 years from now I will look back on this decision with no regrets regardless of the outcome. I wake up so excited to share new content on the blog.

Now where did all that money go?

Home Improvement $4,796 in last month’s report I warned that we had a pre-planned home improvement project. During February we had cabinets installed in our garage. We also had to buy another 5 gallon bucket of paint so my wife could continue painting the interior of our house. Yes, she is way handier than I and has already painted 75% of our 3,300 sqft house by herself ( thank you baby). We don’t have any other projects planned this year, which will be good for our savings plans.

- One time expense

Home Mortgage $3,015 (the normal payment is $2,215/month; however as a part of our 7-year mortgage pay off plan we started adding an extra $800/month towards principle)

- No change vs. previous month.

Condo Mortgage & HOA $1,138 (This is the payment on our rental condo that is just 10 miles from our house. We currently rent this place out for $1,350/month, so we have a small but nice positive cash flow of $117/month after our $95/month property management fee.

- No change vs. previous month

Note: Both mortgage payments are inclusive of property taxes. Property taxes run $583/month on the home mortgage and $160/month on the condo.

Food & Dining $1,151 (This amount includes money we spend at the grocery store and eating out. In the month of February we spent $834 on groceries and $317 on eating out restaurants. This is an expense that tends to get a little out of control for us. Last year we spent $14,000 on eating out or almost $1,200/month on average. The goal for 2015 is to keep this combined expense at or below $1,200/month; $500 for eating out and $700 for groceries).

- Previous month: $1,130

- Difference: +$21

We did really well cutting our expense eating out. We virtually spent the same amount of money in this category, but we also stocked up at Costco on Valentine ’s Day for items we don’t buy that often. Maybe in March we can see this edge closer to $1,000.

Shopping & Other $1,356 this was bit of a surprise that caused me to do some digging and also make some changes. First, my wife had a spa day planned with her mom that was a Christmas present ($300), my wife got her hair done and paid for skin care products ($200), our quarterly wine shipments ($240), our quarterly cheese shipment ($50), our quarterly olive oil shipment ($40), and then William Sonoma ($200) [and I am not even sure what we got, this was news to me]. We spent another ($50) on iTunes and Amazon, and ($50) at sports authority, ($40) on dry cleaning, a haircut for me ($20), and other ($6).

- Previous month: $907

- Difference: +$449 (Yikes, I thought this would go down not up)

When I put the January report together I had forgotten about our quarterly memberships. These are things that are nice to have, but I actually hate committing to recurring expenses. So as soon as I saw them hit this month I was on the phone to cancel a few of them. We canceled one of our wine club shipments that will save us $153/quarter and our cheese membership at $50/quarter. I really need to find out what we got from William Sonoma (that one is puzzling).

Travel & Hotel $0

- Previous month: $722

- Difference: -$722 (finally a decrease)

Deposit Reimbursement $0

- Previous month: $500

- Difference: -$500 (another win)

Auto and Transport $593 (This includes fuel, car insurance on two cars, and toll roads) we spent a little more because I guess our car insurance did not get charged last month. I got a notice in the mail that they needed me to update my payment details. So we got hit twice with insurance this month.

- Previous month: $438

- Difference: +$155

Medical & Dental $0 we are really healthy and I don’t anticipate any additional large expenses this year. In fact, I am actually going to switch our plan from the Kaiser HMO to a HSA PPO, which my employer will be depositing $850/year into for us. So hopefully we can make money here instead of spending it. I am also in the process of disputing the $452 we spent the last month for the anesthesia related to my wife getting her wisdom teeth pulled. The insurance company is currently re-running the claim…so keep your figures crossed.

- Previous month: $452

- Difference: -$452 (another win)

Bills & Utilities $400 (This includes our monthly utilities like gas, electric, water, internet, and cell phones) Not much to say here, besides our usage was up slightly.

- Previous month: $409

- Difference: +$9

Health & Fitness $180 we made some cuts as planned from last month’s report. We should see this come down another $70 in March.

- Previous month: $315

- Difference: -$135 (another win)

Business Services $0 (This is for some expenses related to the business I recently shut down) I don’t expect any more of these expenses for a while. But at some point I will be investing in the blog, these expenses should be minimal and by then I will also have some income to offset the hit.

- Previous month: $154

- Difference: -$154 (another win)

Total Expenses $12,629

- Previous month: $9,275

- Difference: +$3,354

If you recall, in last month’s report I thought we would have normalized spending around $7,500 plus an additional $4,500 for the home improvement project. However, we ended up closer to $8,500 due to the expenses I had forgotten about. Additionally, we spent a bit more on the home improvement front, which is how we ended up spending a bit over $13K.

Like last month, I think there are a lot of one-time expenses that won’t be hitting again next month. We won’t have the huge $4,800 home improvement expense next month. I think our food and dining is right where we want it, the trick is going to be to hold it there. I think we can cut the shopping category by $700 in March since we won’t have the delayed Christmas present and my wife won’t be getting her hair done or buying skin care products for at least a few months. We cancelled a wine membership and we don’t NEED anything else from William Sonoma. So if you add the savings up from no additional home improvement projects and the one-off expenses in the shopping category, we should realize a savings of $5,500 next month.

However, there is a large expense that we will be incurring in March and April for some business coaching that my wife has signed up for. We are paying it in two installments to save some money on the total cost of the coaching program. The coaching will cost $4,500 in total and will be split into two payments of $2,250.

As I have mentioned on this blog before, my wife is in a family business that she intends to grow and one day take over. So this is an investment in her professional development, our future, and the future of the business. We are big fans of making investments in ourselves-the ROI is huge!

So with that upcoming one-time expenditure, we can expect to save about $3,250 in March vs. our February spending. I am projecting spending to come in right around $10,000 in March.

Due to the heavy spending during February through April, the wife and I have agreed to have weekly check-ins on our spending to see if we can find more ways to offset this and get our spending down closer to $9,000 for the month. This will likely mean less spending on eating out and/or in the shopping category.

Additionally, we have taxes coming up in April where we will be cutting a check for about $3,000 (uggghhh).

It looks like May will be the month where we really reign in the spending and crank up the savings. Not exactly what I want to be reporting, but its reality.

What were Investments and Contributions?

I currently work for an employer that offers a 401K with matching. For years now, I have taken advantage of maxing out my 410K (2014 max was $17,500, and this increases to $18,000 in 2015) for both the tax benefit and company match. This works out to be about 16% of my income off the top before I ever even see my paycheck.

My wife happens to work in a family business and unfortunately they are not able to offer a retirement plan, let alone matching. So starting in 2014 we opened up an IRA for her that we plan to max out with $5,500 every year. We actually just contributed $5,500 in January of this year to max out 2014. The IRS allows you to contribute for 2014 until the tax filing deadline in April of 2015. Then starting with February, we have set up an automatic contribution of $500/month.

I also have an IRA due to a 401K rollover from a previous employer. I personally wish I could have all my retirement money in my TD Ameritrade IRA account because of the unlimited investment choices and the ability to invest in many different asset classes, including options.

Now lets take a look at what activity went down this month:

- Contributed lump sum of $500 to the wife’s IRA for the 2015 tax year.

- Previous month: $5,500

- Difference: -$5,000

- Contributed $1,215 into my 401K. The normal contribution will average 16% for the year, but I do play around with the percentage occasionally.

- Previous month: $2,540

- Difference: -$1,325

- Made a personal loan of $0

- Previous month: $3,100

- Difference: -$3,100

- Increase in Savings $0 (this includes checking, savings, and CD’s) we actually had to tap into our savings this month due to the heavy spending.

- Previous month: $1,592

- Difference: -$1,592

Total Investments & Contributions $1,715

- Previous month: $12,732

- Difference: -$11,017

Summing it all up against the Gross Income

Benjamin Franklin famously said, “that everything has a place and that everything should be put in its place.” With that, let’s summarize where the Total Gross Income for the month of February went.

Gross Income $15,711

(Less) Expenses* $12,629

(Less) Investments & Contributions $1,715

Sub-Total $1,367

(less) Taxes & Benefits $3,245

(Plus) Draw-down from Savings $1,878 (This was the amount that our cash-stash decreased since we spent and contributed more than we brought in this month)

Total = ZERO (all income accounted for…plus some)

Everything is accounted for (phew!).

* I will point out in case it wasn’t clear in the expense section above, the expenses include an additional principal payment of $800 on our primary residence.

Net Worth and Mortgage Pay Down Update

My ultimate goal is to build up a Net Worth of $10M returning 6% a year or $50,000/month in gross income.

I am not anywhere close to a 7-figure net worth yet (or what some refer to as the double comma club). However, it is growing at a very respectable rate. If you want to see how I plan to get there you can read all about it here.

February Net Worth $196,990 (with two months down in 2015, this puts me up $15,626 or 8.6% vs. 2014 so far and we still have 10 months to go)

- Previous month: $195,141

- Difference: +$1,848

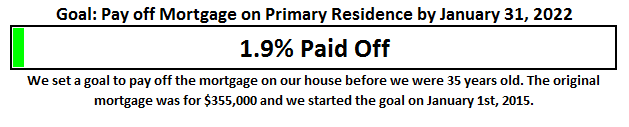

One of the other huge goals that I announced on the blog recently, was the strategy to pay off my mortgage in 7 years. When you break it down and follow the 3 simple rules, it’s not as hard as it sounds. We bought our house in February of 2014 and then refinanced it into a 5/5 ARM in September to remove PMI and free up cash-flow to put towards the principal and keep us on track to pay the mortgage off at an accelerated pace.

Year 1 of the plan has us adding an additional $800/month to our payment. And as you can see from the summary above we were able to reduce our principal by $1,349 in the month of February.

The progress chart above shows how much of our goal we have completed. Last month we were at 1.5%, which means we picked up another 40 basis points in February. At this rate we will be 5.9% complete with this goal at the end of 2015.

The End

February wasn’t a stellar month like January, but it was still forward progress.

This month you get to see that I am not superhuman and have my own financial hurdles to work through. I don’t particularly like spending more in a given month than I bring in. Although our income is high, I still think that our spending has a lot of room for improvement. We’re not going to make these changes over night.

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

“If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!”

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years slaving away for the man, before you have the option to retire. I personally think that 20-25 years is really all you need, and for the folks that are more aggressive or very high earners you can probably reach financial independence in 10 years or less.

I am looking forward to chatting with you guys in the comments below. Anything I should elaborate on? What can I add that would help you take action? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

Cheers!

– Gen Y Finance Guy

PS: Here are my favorite ways to track this stuff:

- The “Financial Stats” spreadsheet – a simple Excel template I created to provide the tables and charts you see in this post as well as on the Financial Stats Page. If you would like a copy of this spreadsheet, sign up for my email list and email me at mrgenyfinanceguy@gmail.com and I will send you a copy.

- Mint.com (free) – Mint is great for setting up budgets and automating the tracking of your actual spending habits vs. the budgets you set.

- PersonalCapital.com (free) – This is like Mint, but is geared towards investments and net worth tracking.

27 Responses

I love how you’re so organized. Do you use a software program to track transactions and create these financial reports? I use good ole excel because of all the flexibility it offers.

I use Personal Capital to track all my expenses and then I have a custom template built in excel that I use to paste in the graphics you see on this report as well as my financial stats page.

I still love my Excel.

Cheers!

I think you have the correct attitude. It takes time to make changes. Our spending is always less than what we bring in, but it takes time to pare things back.

Home improvement is a killer!

Yes, that will probably be my next rant piece I talk about.

Besides February – April just being very high spending months, we have plenty of room to make some cuts. But we will never be the Fruglewoods, nor do we desire to be. Starting in May I am confident that we should be back to building our net worth by at least $3,500/month for remainder of the year.

We are almost half way through the month, and we have been doing really well on holding our budget down on eating out.

Cheers!

I’m interested in your ideal amount of liquid cash. Do you keep a certain figure or percentage in cash for emergencies, etc? What would you suggest for the average American. I’ve heard the 6-months salary figure bandied around.

Hey Simon,

I am a bit of a cash whore…A few years ago I didn’t like seeing my liquid cash dip below $20K. I think that is still a very real psychological number for me. But we have gotten comfortable maintaining a cash balance of around $40 to $50K. If something really bad happened like we both lost our jobs at the same time and we went into survival mode this would likely last us a year without needed to dip into investments or anything.

I think 6-months is a good number. It really is a personal decision. To me the less financial obligations you have on a recurring basis the lower this number can be. But when you have a mortgage and a rental property a larger cushion helps me sleep at night and not worry about much.

The biggest thing for me, is I never want to be living paycheck to paycheck. This month is a perfect example where my expenses are high, and although I don’t like spending more than I bring in on a given month. Having a big cash stash makes it pretty stress free to take care of anomaly months.

Cheers!

You really don’t have a clear picture of your expenses until you list them out. I think Personal Capital is a great tool that I use. Looks like you’re taking a great stab at “cutting the fat” off your expenses which you do not feel are of value for the price you pay. I think cutting recurring expenses is a great way to trim the fat. Luckily since moving to the city I’ve cut all recurring expenses except cable, internet, and electricity (and rent of course) since moving to NYC. I sold my car so no personal property taxes or car insurance. Didn’t really ever use Netflix so don’t have that anymore. Amazon prime gone (since the two day shipping made it to easy to go online and buy whatever I wanted). Any other random memberships got cut too. My cell phone gets paid by work and half of my gym membership gets paid by work (I negotiated a large discount as well by paying for 18 months in advance last year). Keep up the good work.

Thanks FF.

As soon as we can get through March and April I will feel better about our progress. But this month is shaping up to be pretty good so far vs. what we planned for. Should be able to increase that net worth figure by an additional $1,000 vs. February.

Good job on cutting your expenses. Getting rid of Amazon Prime certainly removes that temptation to go hog wild with purchases.

Thanks for stopping by.

Cheers!

GYFG,

Your income looks really solid even though you made less than in January. Those home improvement expenses can be a bitch especially if you recognize the expense in all in one month. I had a fence set me back over $4k last summer. Everything else in your month looks pretty good. Do you have a yearly budget you are trying to stay within?

MDP

Thanks MDP!

I knew income would drop this month. But I would love to bring in January’s income amount every month.

We are done with home improvements for the year. Now we just have the business coaching and taxes to overcome in March and April.

Regarding a budget do you mean for home improvement or total spending? Or something else?

Overall the goal is to grow our Net Worth by about $70K this year.

GYFG

You might be the most detailed person that I know, Gen Y! Progress is progress however you slice it. Keep it up and you’ll surely retire on schedule to live out the remainder of your life in jobless bliss.

And by the way, your house is huge! 🙂

You are so right Steve! Sometimes we forget that forward movement of any kind is still progress towards our goals, even when it is not at a pace we prefer.

You know what they say, the devil is in the details. I feel obligated to share the details to really give full transparency.

Our house is bigger than we need, but we rent out a room and we saved about $300K vs. what we were going to spend before moving out of Orange County. We like to entertain a lot. For Thanksgiving we had 80 people over 🙂

Enjoy Beer Saturday. You got some work to do to work through all that beer left over from the wedding.

Cheers!

Cool way to track your money! I think it’s great because you treat it like a business or a company’s performance.

Thanks Money Spot!

I think that is the only way you get ahead is by treating it like a business. You can’t optimize what you don’t measure.

Thanks for stopping by.

Cheers!

The S&P was up by about 5.5% in February. Are your pre-tax investments in very risk-averse vehicles (~2.5% return)?

And why so much liquid cash?

Hey Paul,

Good observation on the pre-tax accounts. It is really a function of two things:

1) I am sitting on almost 50% cash waiting for better prices.

2) I also have some short deltas to hedge what long positions I still have on.

So that is causing a bit of under performance.

Regarding the large cash stash again driven by a few things:

1) We are looking to add a 2nd investment property sometime in the next 6-12 months that will require a decent down payment.

2) We have about $6K tied up in short term CD’s paying 3% that expire at the end of the year. Again holding out for better prices in the market. I don’t like buying all time highs.

3) We also like to have a few months of expenses in the bank.

I know its not ideal to be sitting in so much cash. But to me the risk/reward favors the downside. But I could very well be wrong and that will cause significant under performance for the year. But I like to sell into strength and buy into weakness.

If you were in my shoes, what what you be doing with all that cash?

Thanks for stopping by.

Cheers!

Wow, that is a detailed report. I really appreciate the level of transparency that you demonstrate here.

Most of the finance blogs that reveal income/spending are on the frugal to very frugal end of the spectrum. I am more in the middle (high income, but still some high expenses). I think you might be a little more past me with the wine and cheese memberships though!

Thanks Vawt! Transparency is very important to me in order to earn the trust of my readers. Plus it shows people that I am human.

I am for sure not a Mr. Money Mustache.

We did cut back a bit on the cheese and wine memberships.

Hope to see you around.

Cheers!

Looks like you are doing a great job! Keep it up. Does your Bride work outside of the home? I always include my wife and I in our Financial Statements. Also I do not see that you have a valuation for your business or your website that I am sure you generate revenue from? Do you think you have any asset value with your businesses?

Hey Noah,

My wife does work and is included in the financial update.

Great observation about the business valuation. I have not yet incorporated this into my net worth report. I recently shut down a consulting business so that I can focus my time here on the blog and have a better ability to scale my efforts. The blog is making money, but not enough to make it worth carving out separately. For now the income will just go into the Side Biz bucket and I will not include the business valuation in the net worth calculation just yet.

But this is something I plan to incorporate in the future. Especially since it is a part of my goal of a $10M net worth:

Wow this post must have taken you a long time to write. It’s fun to analyze progress though isn’t it? Nice job overall in Feb. It doesn’t feel like March is already half over. Where does the time go?

Yes, these reports take a few hours to put together. However, I have a pretty nice template built in Excel that save me a lot of time in February since I built it in January.

And personal capital is certainly helping to see all the numbers in one place.

Analyzing progress is both fun and enlightening. I always say that you can’t optimize what you don’t measure.

I also can’t believe that April is less than two weeks away.