I remember a time when I rushed to get my taxes done and submitted so that I could get my refund. Oh, how time, education, and increased earnings has changed that. Can you relate?

First of all, I no longer overpay on my taxes. I accomplish this by managing my withholding’s on my W-2 income (use the W-4 form to change these). I see absolutely no reason why the government should get to hold my money, interest free. And if the shoe was on the other foot, the IRS would charge me interest and penalties at the first chance they got. Plus, I am a Finance Guy and the concept of opportunity cost is ingrained and rooted so deeply, I can’t help myself.

I will admit that this sometimes causes a bit of tension between my wife and I when she walks into the office and sees the estimated taxes we owe on my screen at almost $10,000 (see below). But fear not, I assure her, I don’t have everything in the system just yet. I also remind her that we will likely still owe taxes at the end of the day because we had a really good and record-setting year. She gets it, but the sticker shock is just a little nauseating.

So this morning, I logged into Tax Slayer, the tax software that I have been using to prepare and file my own taxes for years. In my opinion, it is a very easy and intuitive piece of software that anyone can use to prepare their own taxes. Over the last few weeks I have been entering tax information as I have received it. And as I mentioned above, the last time I logged in, my wife walked in on an estimated tax bill of around $10,000 (see above).

Today I was ready to do a little more work as more tax documents have trickled in since this last session. After spending another 45 minutes working the numbers in Tax Slayer, the new estimated taxes came in around $4,000 (see below):

I still have one 1099 that I am waiting to receive, as well as some deductions to enter, but not enough to make what I owe above go to zero. So as you could imagine I am in no rush to get my taxes filed before the April 15th deadline. After everything is said and done, I think we will owe somewhere between $3,000 and $4,000 to the IRS.

Why I love Tax Season

Yes, there is a sick part of me that loves tax season. I think it really boils down to two reasons:

- It forces me to reflect on the past year and how we did financially. I am happy to declare that2014 was a great year! We increased our income by $40,000 vs. 2013 and saw our net worth increase by $78,000. On my Financial Stats page, I make all of this public if you would like to see it with your own eyes. And don’t forget about all the juicy details I just started releasing in my monthly financial report, starting with January 2015.

- It is kind of a game to me. I love opening up Tax Slayer for the first time in the New Year to start working on the prior year’s taxes. I typically start with all my income and watch the tax bill grow to wicked-high numbers. But then, I start layering in our deductions and adjustments and experience pure joy as the estimated taxes tick ever lower-almost as if I have outsmarted the system. The closer it gets to zero, the more euphoric the feeling.

It is really important to take some time to reflect on the past and acknowledge the milestones you hit. It is so easy to keep your head down and always looking to the next thing…

So here are some of the wins for us in 2014:

- We paid off the remaining $8,000 I had in student loans. The 2.25% interest rate was low and tax-deductible, but it was a nagging debt that we were tired of seeing. We had more than enough money to kill it, so we did.

- We bought a huge house that was less than we could afford. The timing could not had been better since we bought at the beginning of the year, which allowed us a pretty nice deduction on the interest and property taxes for the year. These deductions certainly helped reduce the tax bill. We had previously been renting and paying $3,000/month. The new mortgage is $2,200 with property taxes and HOA.

- We moved to a lower cost-of-living area. This allowed us to buy a house 4-times bigger than anything we were looking for in Orange County (where prices are ridiculous), and spend half the money. Besides the savings related to having a mortgage that was $800/month less than the rent we paid and the tax savings related to the interest and property tax deduction, this move also saved us money on things like gas, tolls, doggy daycare, etc. We did the math and estimated our total savings from the move to be around $1,750/month. You can read about the details here.

- We paid off my wife’s remaining car loan of $7,500. Again the interest rate was a low 1.7%, but we would much rather earn interest then pay it. Outside of our mortgage this was the last piece of consumer debt we had left to kill.

- I changed jobs and increased my income. My wife was already working about 8 miles from where we bought our new house. Shortly after we closed escrow on the new house and before we moved in (about a month after we got the keys), I was able to secure a new job that was only 4 miles from the new pad. The next move will be working for myself, and the commute will be from my bedroom to my home office, but for now 4 miles isn’t bad. The best part of it all is that I was actually able to increase my income by $10,000, even though we were moving to a lower cost-of-living area. And now, after being there for less than a year, my income is $18,000/year higher. That is not bad considering I was preparing myself for a lateral move at best and possibly a pay cut as a trade-off for no commute.

- We maxed out my 401K with $17,500 again. The plan is to do this every year without thinking about it (I’ve been doing it for years now). The limits changed this year, so I increased my contribution to make sure I max out the $18,000 new limit.

- We maxed out an IRA with $5,500 for my wife. Her employer doesn’t provide a retirement plan, so this was really our only option. But it’s a good start and something we plan to do every year from here on out.

- We got a $20,000 windfall from my wife’s grandparents. They have a family tradition to give $20,000 to each of their kids and grandkids when they buy a house. This allowed us to put in an awesome outdoor kitchen and artificial grass. We won’t be expecting this in our income next year.

- I made about $18,000 from a side-hustle consulting practice. I started a digital marketing and analytics consulting business in 2014 that brought in some nice cheddar. Although this was a nice additional income and a very successful project, I chose to shut it down as of January of this year. The reason being is that I want to be able to spend time building this blog and the community with awesome content and now I have the skills and the time to do that. And secondly, I felt it was just another exchange of time for money when. I am looking for something more scalable. I want to leverage my time many times over (the amount of people I can reach with this blog is limitless)and the earning potential online is massive and scalable. It was hard to give up the extra income, but an easy decision when I took into account my end goal.

And the one loss for the year:

{kind=link}

- We pulled out $20,000 from our retirement accounts to put towards the house. As you may or may not know, the IRS lets you pull out $10,000 penalty free to put towards the purchase of your first home. This is a one-time benefit that both my wife and I qualified to do. I would have rather kept this money in the accounts, but we did not like where our savings account would had ended when we first bought the house.

Overall there were way more wins than losses. And as you can see, we had a really awesome year.

Why I hate Tax Season

Well, the obvious reason is I never really enjoy writing a check to the IRS. Does anybody? But there are other things that just bother me about how messed up the tax system is, in my opinion. Let me preface this with a couple things – I understand we live in an amazing country and it takes money to run it. And, I am more than willing to pay my share in taxes for the privileges of living in the USA. But there is a list of things that annoy me so much that I hate tax season. I want to see rules that make sense and are more thoughtful rather than just having them shoved down our throats.

- I hate the fact that the contribution limit for a traditional IRA is $5,500 when you can contribute $18,000 to a 401K (in 2015 that is). My wife happens to work for a small business that can’t afford to offer a retirement plan. Why should she be penalized for that? I think we should have the ability to contribute just as much to her IRA as we do to my 401K. Who is with me?

- I hate some of the phase outs for deductions. When we first bought our house last year we got a FHA loan, with plans to refinance within a year. We were actually able to do this within 8 months (saving us $400/month by getting rid of PMI). However, although the tax deduction for PMI was extended to 2014, I found out that the almost $3,000 we paid in PMI would not bring any tax benefit because our adjusted gross income was too high. I am over it now, but a few weeks ago, I was pretty pissed off.

- I hate the rules about carry-over losses. When I first started investing in 2007,I was still in college and very green. I made some investing mistakes that cost me about $18,000 in an after-tax account (all of our money currently in the market is in a pre-tax account). It was a huge learning lesson, and is what caused me to learn and master the markets. However, the IRS has a ridiculous rule that you can only deduct up to $3,000/year for prior losses. But on the flip side of the coin, you have to always pay taxes on all of your gains. This rule is a bit ass-backwards if you ask me.

I am sure I could find more reasons why I hate tax season, but these are the 3 that come to mind relatively easily.

Now its your turn

How was 2014 for you? What were your wins? What were your losses? Do you love or hate tax season? Why? Please continue the conversation in the comments below, I look forward to hearing from you.

– Gen Y Finance Guy

20 Responses

Looks like y’all had a hell of a year! I HATE tax season and actually go as far as to pay a professional (~$200) to deal with it for me. I have a LLC for my side hustle, which ends up being more paperwork and taxes – kind of a pain.

We have an investment account that produces some nice dividends and we are constantly getting hit with that tax…as well as the tax from self-employment income. Seems wife’s company neglected to withold taxes from her last bonus check too…so ouch.

All in, we are looking at owing about 1500 to Uncle Sam, but hopefully this kid popping out will help lower the tax burden. The nice thing about Texas is that we don’t have to contribute to our State’s spending problem (state income tax) like we did in CA.

It was a smart move getting out of OC, we were happy to do the same and could never have afforded a house there. As much as we love Dana Point, it just wasn’t going to happen.

BTW, nice job with the backyard – I love that outdoor grill/kitchen area.

Hey Brian,

Yes we had our best year ever. We actually expect to take about a $35,000 hit in income this year vs. last year. Unless I can really ramp of my monetization strategy 🙂

$1,500 doesn’t sound like to bad of a hit. I always say that taxes are a good problem to have, because at the end of the day it means you made money. But it doesn’t make writing the check any easier.

The backyard was the most important area for us to spend money on.

We will have to have you and the wife over if you guys ever come back to SoCal to visit.

Cheers!

Wow congrats on all of those wins! Your home improvements look amazing. It feels so good to see transformations on your own property doesn’t it?

Taxes are a pita, but I agree with you that they do help us look closer at our finances and find ways to save and improve.

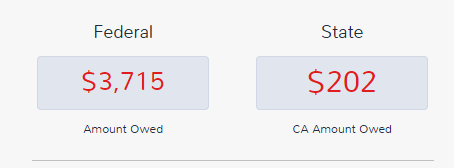

I’m gonna owe a big tax bill this year both for CA and Fed, so I’m not looking forward to that, but at least I’ve been anticipating and saving for it.

Hi Untemplater,

Thanks for the comment. It sure does feel good to see the transformation of our house into a home.

Sounds like you had a good year and have been preparing for the tax-equences 🙂

Cheers!

I have a bit of a different take on tax season, given I used to prepare them professionally. The best way to see what the wealthy do with their money? File their taxes or become their financial planner. Both offer a window into what works and what doesn’t. I was always fascinated to see who had a good year or who had a bad one.

For myself, I actually enjoy filing our personal taxes. Something about filling out those forms and evaluating our individual tax situation. Planning for the next year to see what we can or can’t adjust to maximize our income while limiting our taxes paid. All in all, a fun exercise for me.

I agree W2R, that optimizing your financial situation to reduce your tax bill as much as possible is the fun part.

I am sure you have seen a lot since you use to prepare taxes for people. Sounds like I might be able to learn a thing or two from you 😉

Cheers!

Man love the backyard, particularly that bbq set up. Congrats on the job and location.

Not taking advantage of that incredible climate to put in a mini-orchard of citris?

Thanks Adam!

The BBQ/Kitchen area is for sure a man station. We spend a lot of time out there using the BBQ and the fire pit. Especially when we have people over.

We do have a lemon tree and a dwarf orange tree. We are thinking about putting in either a lime tree or an apple tree next.

Any recommendations? You seem to have the green thumb.

Sweet looking backyard! Definitely looks likes a relaxing place to hang out enjoy the weather. I love preparing taxes (mine and clients) and also tax planning. I have a pro-forma spreadsheet going throughout the year and update based on any new numbers so it’s not a shocker at tax time. Like you said, it’s like a game and I guess I’m just a tax nerd because even though the tax code is complete nonsense (I think it should be way simpler for everybody), it’s like putting a puzzle together. Congrats on the side hustle business. That’s some nice extra income. Did you get to take advantage of the home office deduction? I would make my backyard my office if it looked like yours!

Thanks Lifestyle Accountant! The backyard is really where we spend almost all of our time, especially when we have people over.

I hope that I will be able to call it my home office one day. Figuring out the tax optization strategy is the fun game part. It’s just the writing the check I don’t look forward to, its as if I am leaving points on the table.

But in all honesty we actually do really well taxwise after all of our deductions and pre-tax contributions. So I can’t complain.

We for sure took advantage of the home office deduction. I think everyone should have a side business because of the tax benefits that come along with it.

What is your opinion on that?

100% agree. A side biz is a great way to build skills and wealth while still working a regular job. I recently took on some virtual tax prep work this season and am using a spare bedroom in my house that I converted to a home office. You can take up to $1,500 as a home office deduction using the IRS’s simplified method for qualified business use. Possibly more if you use the regular method. Either way, it’s a great way to take advantage of extra space in your home and save on taxes.

Love the BBQ area! Nice backyard. We haven’t done our taxes yet. Usually, I use an accountant, because having the rentals, flips and a few stock wins seems too complicated to me. But maybe I should just do Turbo Tax online or something (never heard of Tax Slayer, but maybe that’s better?). Would like to not pay like $200 for an accountant if I knew I can do it all myself.

Would love to hear more opinions from you and readers about options to file taxes yourself when you have rentals, flips and short-term stock wins.

Hey Felix,

Tax Slayer is like a Turbo Tax. I have been using them since like 2007 or 2008. It is very easy to use. I have a rental, side business, w-2 income, 1099 income, 1098’s, etc.

It walks you through step by step and even has a guided way of filling out your taxes. All for $30.

I’ve also lamented about the contribution maxes for IRAs versus a 401k….That’s a pretty substantial monetary difference! When I quit my job last year, I lost my ability to contribute to my 401k and get the match. That part really sucked as well.

Thanks for stopping by Robin.

Hopefully you have been able to at least open up an IRA that you can contribute to or maybe even a SEP IRA with higher contribution limits.

I work for a small company in a different state, so I have an S-corp. Meaning I feel your pain on quarterlies. I hate the stress of tax deadlines. I just turned in my business taxes. Once I those are done, I’ll do our personal return myself.

Taxes are complicated because sometimes I get some ad revenue on my blog or some freelance articles, plus I have a fair chunk of overtime opportunity at my job. So I have to estimate generously.

When my yearly bonus comes in, I just throw 20% at the quarterly payment to ensure I don’t underpay. That means we do usually overpay by $300-500, but I like to be cautious.

Once you get it the swing of things it’s not too bad.

So did your estimates cover you? Meaning did you owe anything additional or are you getting a refund?

Thanks for the comment.

I kind of have a similar relationship with tax season. I do kind of see it as a game, and I try to learn as much as possible about taxes to optimize my tax situation. I also agree with the phaseouts…it’s somewhat unfair for those in higher cost of living areas. The phaseout cut off is often not a “high income” when you’re in an expensive area.

Resonated with this piece. I see taxes as a bit of a video game. I swear I spent hours last weekend looking at all sorts of minutia just for curiosity’s sake. And while I enjoy my tax dollars going to firemen and foodstamps, I’m less inclined to write these checks since I know they mostly go to government waste and wars.

Yeah, it is so sad how much money gets wasted.

I am with you, I have spend 100’s of hours over the past few years learning how to optimize my tax situation.

Hopefully you did get to big of a hit.